Mexico: Monetary Contraction Is Getting Harder To Justify

Low growth, low inflation, and the moderately strong Peso should help consolidate a dovish outcome in this week’s monetary policy meeting. Risk of a more aggressive 50bp cut is limited, however, as authorities should prefer not to deliver a dovish surprise, to avoid market volatility, especially on the FX front.

Still following the Fed, perhaps for the last time

Mexico’s upcoming monetary policy meeting, this Thursday, should conclude with an extension of the ongoing monetary easing, with another 25bp rate cut to 7.5%.

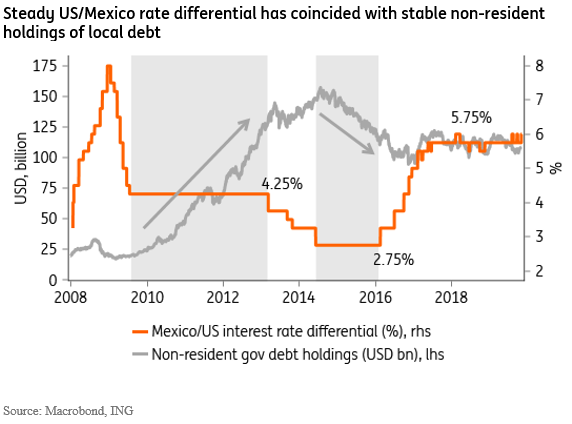

This decision would follow the latest cut by the US Fed, and therefore, it would keep intact the large US/Mexico rate differential. As the chart below shows, that differential has been steady at 5.75% for 2 ½ years now, a period that coincided with fairly stable non-resident holdings in the local Treasury market.

(Click on image to enlarge)

As a result, a 25bp cut this week would be consistent with the policy practice prevailing for more than two years now. Among other things, this strategy has been successful at establishing an effective FX anchor.

Banxico could choose to depart from this practice by cutting the policy rate by 50bp, as two out of the five board members advocated at the last policy meeting. In our view, however, even though the risk of a more extended easing cycle has increased in Mexico, we suspect a majority of the board members should maintain a strong preference not to surprise the market on the dovish side (as it would be the case with a 50bp rate cut).

Avoiding a dovish surprise would be consistent with Banxico’s long-lasting policy focus on avoiding market volatility, especially on the FX front.

Decoupling from the Fed in December

A departure from the US Fed’s cycle is more likely at the 19 December meeting. In our view, Banxico should opt to extend the easing cycle, with another 25bp rate cut in December, even if the Fed opts for a pause in its December meeting.

A December cut by Banxico would be broadly in line with investor expectations and this should help limit any risk of market instability following the decision. Moreover, a deeper easing would be fully justified by recent developments on the inflation and economic activity fronts.

Since policymakers last met, at the end of September, inflation data surprised slightly to the downside while activity data displayed generalized weakening, albeit still shy of qualifying as a technical recession. The sharp drop in investment indicators continue to stand out, as evidenced by the collapse of capital goods imports, the slowdown in corporate bank lending, and the deep contraction in the aggregated investment series.

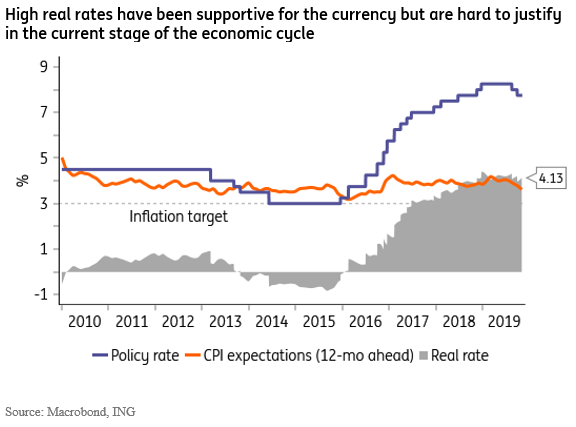

Moreover, as the chart below shows, real rates remain quite high in Mexico. At near 4%, monetary policy remains deep inside restrictive territory, which is especially notable when compared to the level of real rates prevailing among Mexico’s peers in LATAM, with Brazil’s 1.4% (and falling) standing out as the distant second highest.

(Click on image to enlarge)

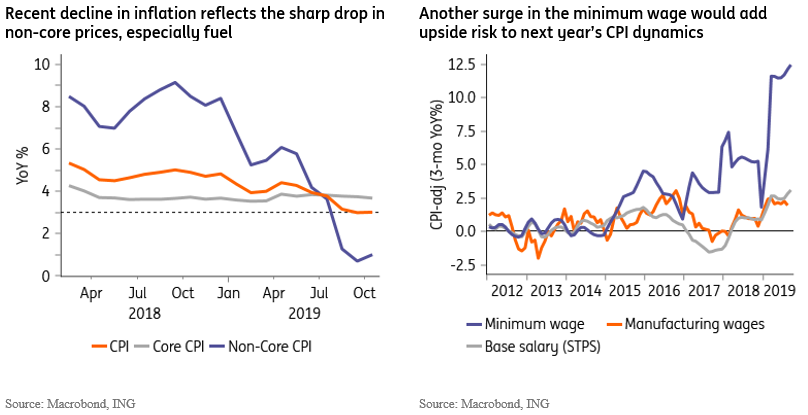

Policymakers remain concerned about certain aspects of the inflation dynamics. Even though headline inflation has reached the 3.0% target at a faster-than-expected pace, the correction was driven by volatile non-core components (1.0% year-on-year, see chart below), while core inflation (3.7% YoY) has remained relatively high, compared to the 3% target.

(Click on image to enlarge)

Inflation expectations are beginning to improve however, and the more favorable inertia, intensified by the government’s pledge to keep fuel prices stable in real terms, together with the strong slowdown in domestic demand should exert downside pressure on core components of the inflation series in the coming quarters. As a result, we believe the inflation outlook has become much more constructive, and now expect headline inflation to trend close to the target in the foreseeable future.

Low inflation complicates justification for tight monetary policy

The benign inflation outlook should make it increasingly harder for policymakers to justify the current monetary policy stance.

At a minimum, we suspect bank officials should be able to deliver a steady pace of 25bp cuts, until the policy rate drops to 6.5% at least (i.e. five consecutive cuts until May 2020). But our base case is that a more extensive cycle is more likely, with the policy rate ending 2020 at 6.0%.

Judging by the caution expressed by the current policy guidance, the risk of a more frontloaded cycle should remain limited. Among other factors, policymakers should remain concerned about:

- the risk of credit rating downgrades, which remains high in light of lingering recession risks,

- the risk of another sharp increase in the minimum wage in 2020, and

- the risk of policy-triggered market instability following policy announcements by the Mexican administration, or the US, as we enter the US campaign season.

Alternatively, the risk of a more frontloaded easing cycle, or a terminal rate that brings monetary policy more firmly into neutral territory (possibly in the 5.5-6.0% range) would increase if the Mexican Peso appreciated, consolidating in the 18.5-19.0 range.

Heightened uncertainties should prevail in 2020

The Lopez Obrador administration remains severely restricted in its ability to conduct counter-cyclical policies. The interest rate trajectory described above suggests that monetary policy is likely to remain restrictive in the foreseeable future (despite upcoming rate cuts).

AMLO’s fiscal policy guidance is, meanwhile, marked by a staunch commitment to a fiscal target, which has resulted in binding spending restrictions amid enormous frustration with economic activity (and, presumably, tax collection).

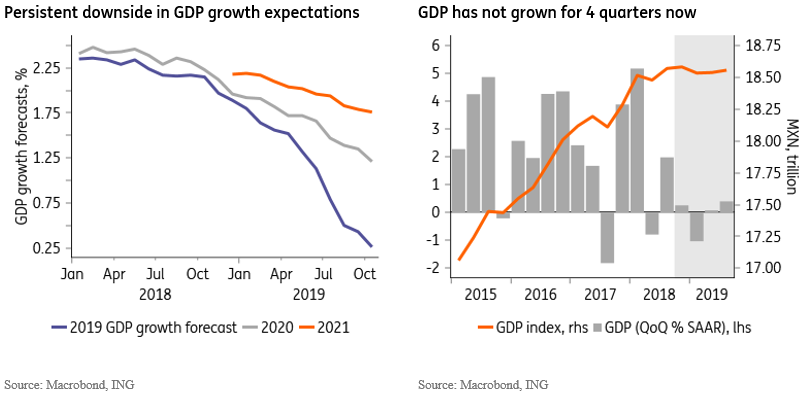

This suggests that heightened uncertainties vis-à-vis 2020 GDP growth dynamics should prevail in the near future. As seen in the chart below, 2019 GDP growth expectations have collapsed during the year and are now close to 0%. Our 2020 forecast is in line with the consensus at 1.2% but downside persists for that as well.

(Click on image to enlarge)

Growth stagnation reflects, to a large extent, the collapse in investment that has taken place in the past year, since approximately the announcement of the cancelation of the Mexico City airport construction.

Prospects for future investment remains dim as private sector perception of elevated risk in regulated sectors, together with lingering uncertainties in the future of the US/Mexico trade relations, especially in the run-up to the US Presidential election, suggest that a turnaround in investment dynamics is unlikely to take place in the near future.

Positive surprises are possible, however, when considering that one-off factors may have played a role depressing domestic demand this year, especially early in the year (strikes, stoppages). Logistical difficulties to implement regulations and launch government-led projects typical of first-year governments may have curbed public and private investment indicators this year

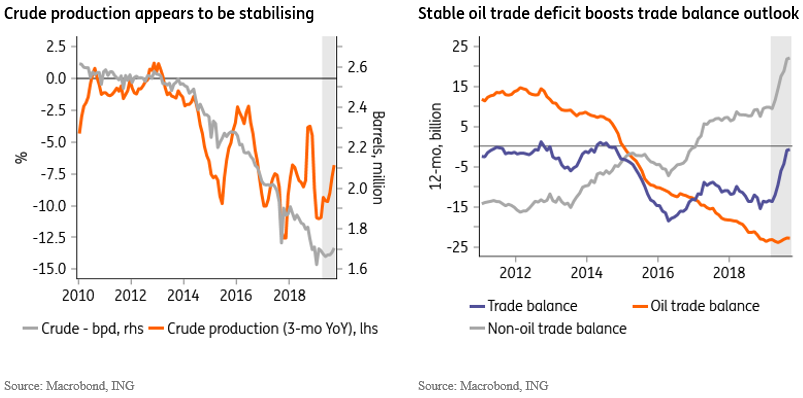

An additional positive we would highlight is the fact that, despite broad-based skepticism, PEMEX appears to have been able to stabilize oil production in recent months, after years of non-stop declines (see shaded area in the charts below).

(Click on image to enlarge)

The administration’s predictions of sharp production increases (i.e. 7% growth in 2H19, relative to 1H19, and a 13% YoY surge next year) still seem too optimistic. But the latest results helped boost confidence on the administration’s pledge to deliver the first (small) increase in crude production in years.

We expect the Peso to underperform next year

The sharp retrenchment in imports, notably investment-related capital goods imports, resulted in an impressive reduction in the external trade deficit in recent months (see chart above), and the stability in oil production would help support that correction in trade accounts.

External accounts also continue to benefit from the steady increase in external remittances. Together, these factors should help lower the current account deficit from about 1.8% of GDP last year to close to 0.5% by the end of this year.

The lower current account deficit should, in principle, be supportive of the Mexican peso. But Mexico’s challenging GDP growth outlook, lingering risk of credit rating downgrades, among other factors, suggest that the scope for MXN outperformance is more limited in 2020 than it was the case for most of 2019. In fact, our expectation is that the USD/MXN gradually depreciates towards 20.0 throughout 2020

The ongoing rate-cutting cycle also suggests that high rates should become less effective as an FX anchor than it has been the case in recent quarters. Having said that, we still see no sign that Banxico would surprise the market on the dovish side, by delivering more rate cuts than are currently priced in the local yield curve. Instead, we expect Banxico to continue to sanction the rate cuts priced in the short-end of the yield curve, but maintain an underlying cautious bias.

But poor activity data could increase pressure on the bank, while a change in the board’s composition at the end of 2020 could set the stage for a more substantial change in policy bias. Javier Guzmán, often seen as the most hawkish board-member, concludes his term at the end of 2020, providing Lopez Obrador with the opportunity to appoint a majority at the monetary policy board. This could weigh on the Peso later in 2020.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more