Key CPI and PPI readings in the US should reflect continued labor

US: Supply constraints and rising costs to give higher inflation readings

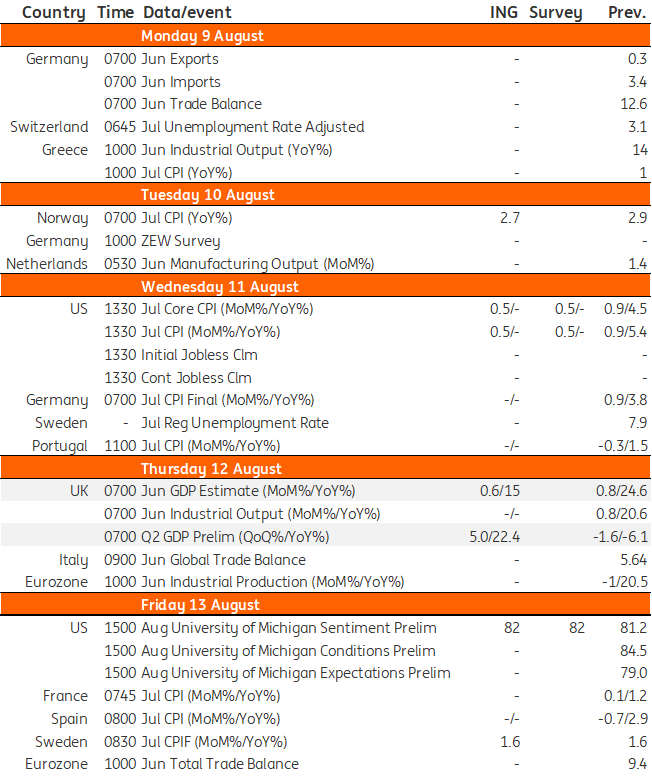

The main economic data points of interest in the US over the coming week will be the various inflation readings.

Federal Reserve doves suggest that inflation shouldn't get as much focus as it has been doing, given that price pressures have been focused in relatively few sectors such as used car prices and areas that have been feeling particular reopening frictions. We are less sanguine and expect to see price pressures broaden out across more areas of the US economy given ongoing supply constraints, including a lack of suitable workers, and robust, stimulus-fuelled demand.

Numerous surveys, including the ISM and NFIB reports, suggest companies are experiencing rising pricing power and are prepared to use it to pass higher costs on to customers and preserve profit margins. Given the lags between these inflation components and actual house price growth, we also expect to see housing costs increasingly be a major source of inflation pressures.

With CPI and PPI set to hit new highs and import price inflation running in double digits, next week's data is likely to give more ammunition to the relative hawks within the Federal Reserve's FOMC membership and support the case for an earlier tapering of asset purchases and interest rate hikes starting in 2022. Also, watch for rising inflation expectations amongst consumers as measured by the University of Michigan consumer sentiment report.

UK: Buoyant second quarter growth to give way to lacklustre summer of activity

Next week’s UK GDP will likely show a huge 5% growth rate for the second quarter.

Of course, that’s largely a function of the reopenings, but it also represents the rapid rebound in confidence and appetite to socialise again among consumers. Ultimately this is a bit out of date now, and the reality is that the growth rate is likely to slow markedly over the summer. We’re pencilling in 1.5% third-quarter growth due to the disruption from higher Covid-19 cases and perhaps some renewed reluctance to visit hospitality and other venues given the risk of getting ‘pinged’. That said, this is likely to pause rather than stamp out the recovery, and we still think the size of the UK economy will be at, or close to, pre-virus levels around the end of this year.

Developed Markets Economic Calendar

Refinitiv, ING, *GMT

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.