Saturday, July 2, 2022 11:50 AM EDT

Image Source: Pixabay

US jobs figures are released next Friday. For us to seriously consider changing our July Fed call we would need to see payrolls growth fall with the unemployment rate moving a couple of tenths higher and wage growth showing signs of stagnating.

The expectation of a 75bp rate hike from the Fed is unlikely to change

Between now and the 27 July Federal Open Market Committee (FOMC) meeting there are only two US data releases that could potentially prompt us to switch our forecast from a 75bp rate hike to a more cautious 50bp hike. After all, the Fed has made it clear that it is resolutely focused on getting inflation under control so we will either need to see a very weak jobs report, published on 8 July or, but quite possibly together with, a surprise drop in inflation, out 13 July, that reflects declines in a broad range of categories. Currently, we are expecting inflation to dip only very modestly from its 8.6% rate in May, but given that is two weeks away, the market will be focused on next Friday’s jobs figures.

We know that there were around 11 million job vacancies at the last count, equivalent to nearly two vacancies for every unemployed American. This itself should point to a very strong figure for job creation, but the issue is the lack of suitable workers available to fill these positions, hence why wages have been rising so rapidly as firms compete for labor. However, we sense that the plunge in equity markets and the increasing recession talk as the Fed ramps up interest rates may lead some employers to slow down the rate of hiring. Consequently, we think payrolls may grow somewhere in the 250-300,000 range, down from 390,000 in May, which should still be enough to keep the unemployment rate at 3.6% and wages continuing to tick higher. For us to seriously consider changing our July Fed call we would need to see payrolls growth fall with the unemployment rate moving a couple of tenths higher and wage growth showing signs of stagnating. Even then we would still probably need to see a surprisingly large decline in inflation the following week.

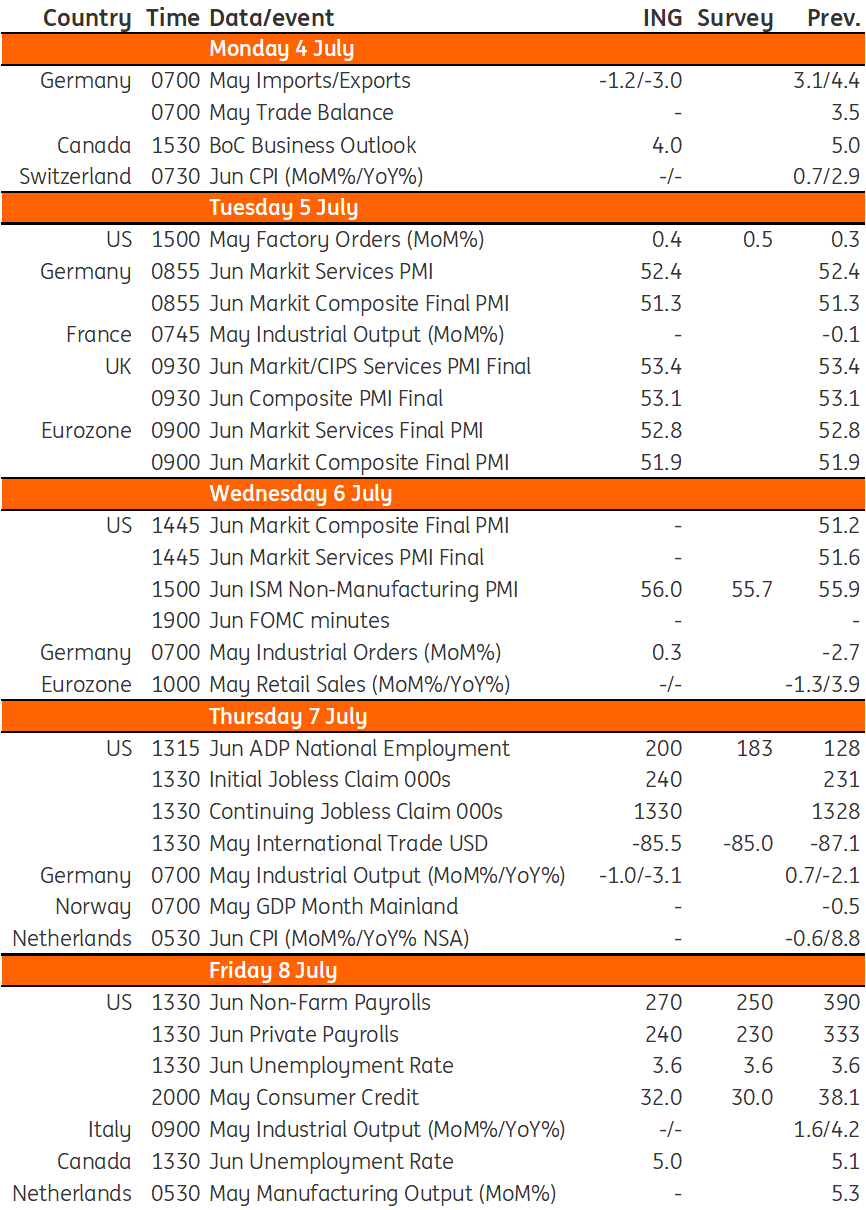

Developed Markets Economic Calendar

Image Source: Refinitiv, ING

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.