The 1.3% QoQ GDP fall wasn't much worse than had been expected (ING f -1.2%), but it highlights the negative impacts of restrictions on movement during states of emergency, and with more of these being unfurled in 2Q21, the prospects for growth in the rest of the year are looking much weaker.

2Q won't be much better

While 1Q21 GDP was not much worse than we had imagined, at -1.3%QoQ (INGf -1.2%), we still probably have quite a bit of downward revision to full-year 2021 GDP to do.

What the 1Q figures do is show the negative consequences of states of emergency linked to daily Covid cases, and with more prefectures being placed under such states of emergency this month (nine in total currently) and growing calls for a national state of emergency as hospital beds fill up across the country, the outlook for 2QGDP is for another decline, and that will make reaching 3.5% for the full year as we are currently forecasting all but impossible to achieve without an improbably large second-half bounceback.

Nothing in the detail to get excited about

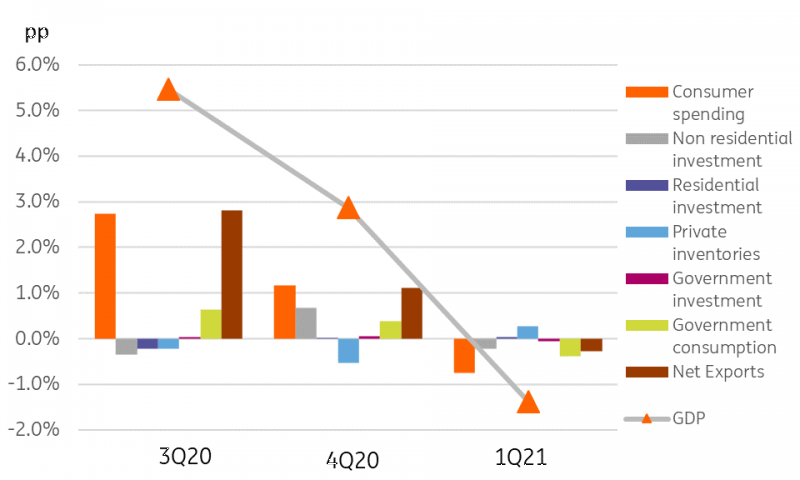

Delving into the sub-components of the release, there was nothing too exciting to note. Consumer spending held up a little better than had been expected, but business investment was worse. Inventories added 0.3pp to the total, as weak demand led to involuntary stock accumulation, but net exports offset most of that subtracting 0.2pp from total GDP growth. A similarly, though perhaps slightly less weak 2Q figure seems probable.

Contributions to QoQ GDP

Source: CEIC, ING

Quick revision points to only 1.6% in 2021

A quick reworking of our forecasts, which are subject to considerable further finessing, suggests a further decline in 2Q21 followed by a relatively slow recovery in 2H21, would result in only 1.2% GDP growth for 2021 as a whole, less than half what we were forecasting previously. But with Japan still lagging behind even many developing Asian economies when it comes to vaccination rates, we believe a more rapid second-half improvement is unlikely.

There will undoubtedly be fiscal money poured on this problem to soften the blow, though after so much already, it is difficult to see this having more than a fairly marginal effect. And the Bank of Japan seems to be out of fresh policy stimulus ideas currently, so we don't anticipate anything new from them apart from extending existing measures.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.