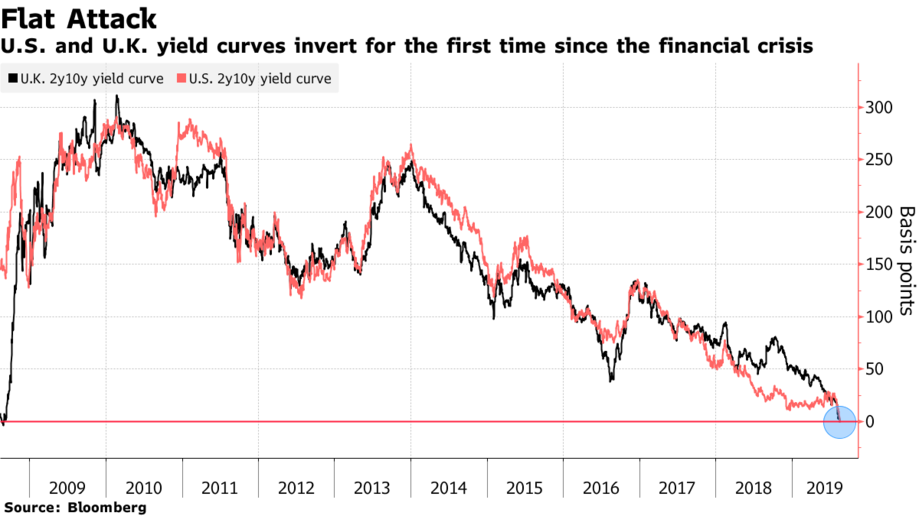

Implications Of Yield Curve Flattening For The UK

In today’s Bloomberg:

(Click on image to enlarge)

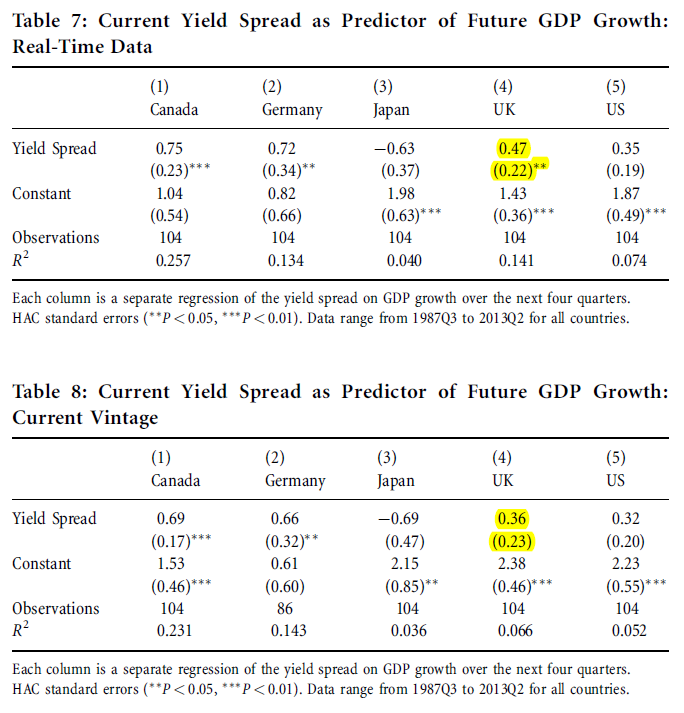

In Chinn and Kucko (2015), we find that the 10yr-3mo spread is not particularly informative regarding recessions (as defined by ECRI) or industrial production growth in the UK. It is informative regarding real-time GDP, however (which is what we’ll see in the coming months regarding 2019-2020). We didn’t report the 10yr-2yr spread results.

(Click on image to enlarge)

Source: Chinn and Kucko (2015).

Disclosure: None.

How did you like this article? Let us know so we can better customize your reading experience.

Comments

Leave a comment to automatically be entered into

our contest to win a free Echo Show.