Hungary: The Hiking Cycle Continues

With an upside surprise to June inflation, we see the National Bank of Hungary delivering a 30bp effective rate hike. The forward guidance and tone should remain unchanged, pointing to more hawkish steps in the coming months.

Economic activity...

The incoming economic activity data in the past month was rather a mixed bag. But we still believe that services will provide a huge boost to GDP growth on the reopening of the economy. We see 7.4% GDP growth this year, which means clear upside potential to the NBH's forecast. This supports our call for a stronger effective rate hike in July (+30bp) compared to June (+15bp).

and inflation...

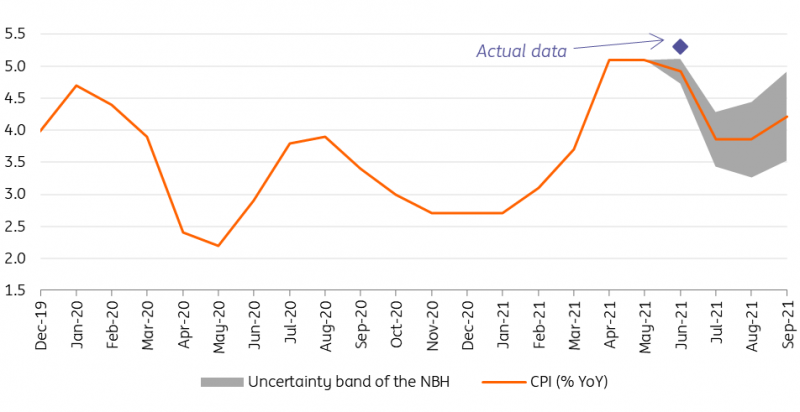

So yes, GDP growth will be strong, but the elephant in the room is the June CPI. It came in at 5.3% year-on-year, with core inflation moving to 3.8% YoY. This wasn’t simply above the market consensus and higher than the central bank’s forecast, it was even higher than the upper range of the NBH’s uncertainty band. With this in mind, we believe that the tightening cycle should continue at a strong pace.

The NBH’s short-term inflation forecast (%)

Source: NBH, ING

point towards a 30bp rate hike...

In our view, this means another 30bp increase in the base rate to 1.20%. To make it effective, the 1-week deposit rate should also move to this level. With such a high inflation print, the NBH could also send a symbolic message with an upward shift in the interest rate corridor. The overnight deposit rate has been in negative territory since early 2016, so the central bank could send a message with a hike into positive territory. We see the NBH resetting the +/–100bp corridor around the base rate, moving the O/N depo to 0.2% and the O/N repo to 2.2%.

and balance of risks suggest more hikes to come

With the rosy economic outlook and elevated inflation, we can say that the balance of risks regarding the CPI outlook has remained clearly to the upside. We can add the labor shortage, the surprisingly strong wage growth, the continued price pressures in agricultural and industrial producer prices, and the loose fiscal stance to the upside risks, too. In this respect, we see no change in the hawkish forward guidance, which will suggest further rate hikes until the balance of risks improves and CPI moves close to 3%.

Inflation forecast of ING (% YoY)

Source: HCSO, ING

But what does it mean for HUF?

The 30bp hike this week and the forward guidance to continue tightening should be positive for the forint and help EUR/HUF to stabilize below the 360 level. With the NBH tightening to be frontloaded (with another 30bp hike to follow next month) and some decline in CPI in July and August (back below 5%), HUF should get some breathing space and EUR/HUF could re-test the 355 level as the NBH tightening should provide an anchor to the forint. Indeed, we now see the NBH benchmark rate around 2% by the year end.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more