High Turkish Inflation Likely To Keep Central Bank Stance Tighter For Longer

Turkish inflation continued to rise reflecting cost-push factors, sticky services inflation, and deteriorating inflation expectations but we think it will peak in April.

Source: Shutterstock

Therefore, the central bank is likely to remain cautious, given the concerns about reserves, high dollarisation and the need to maintain capital flows.

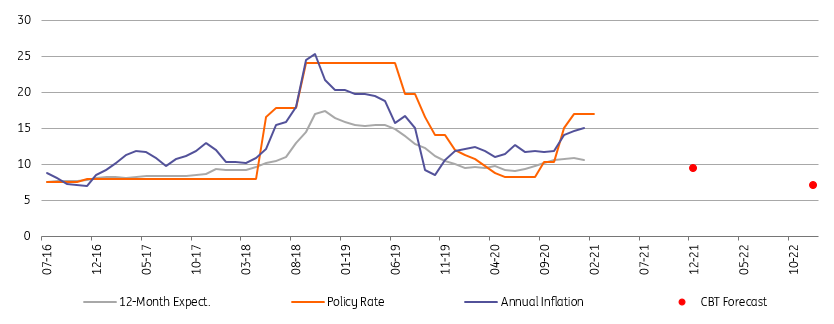

Inflation outlook (%)

(Click on image to enlarge)

TurkStat, CBT, ING

Annual Turkish inflation rose up to 15.0% in January from 14.6% a month ago, on the back of a monthly reading of 1.67% (slightly higher than market expectations of 1.4%, while our forecast was 1.6%). Core inflation also increased to 15.5% with the highest ever January reading in the current inflation series.

The data shows challenging inflation dynamics with high pricing pressures, sticky services inflation and lagged effect of exchange rate developments

The breakdown shows goods inflation at 16.5% - the highest since mid-2019, up from 15.9% a month ago attributable to food, energy, and some core goods despite benign alcoholic beverages & tobacco prices thanks to a tax reduction on tobacco products and elevated services inflation driven by rent and transportation services, though we saw a marginal decline in the annual figure to 11.5%.

The domestic producer price index (D-PPI) has also maintained a sharp upwards trend continuing since last May reaching 26.2%. This is attributable to not only the impact of exchange rate volatility last year but also recent pressure on commodity prices. The outlook indicates significant producer-price-driven cost pressures on the inflation outlook.

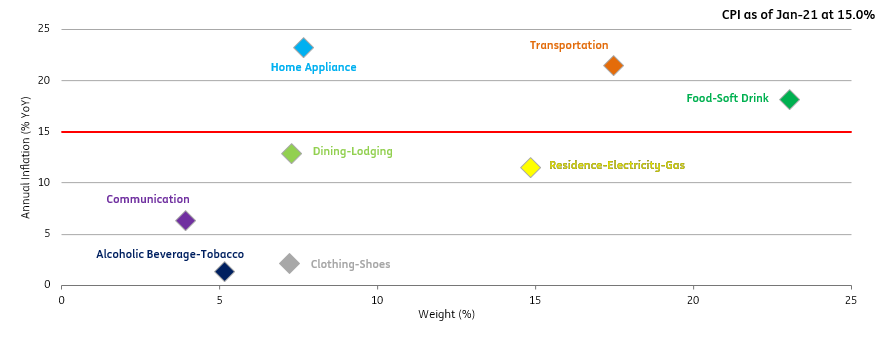

Annual inflation in expenditure groups

(Click on image to enlarge)

TurkStat, ING

Main expenditure groups

- Food has remained the biggest contributor to the headline number with 64bp, attributable to the processed foods given the monthly reading in this group turned out to be the highest January figure in the current inflation series. Unprocessed foods on the other hand took some of the steam with a decline in fresh fruits and vegetables vs seasonal jump averaging to around 12% in the first months of previous years. Accordingly, we saw a decline in the annual inflation in this group to 18.1% (vs the CBT’s 11.5% call for end-2021).

- The second highest contributor was housing with 46bp on the back of adjustments in water, electricity and natural gas prices.

- Among others, the monthly contribution from household equipment by 25bp due to price adjustments on furniture and durables was another driver of January inflation, followed by transportation with 17bp contribution attributable to weight changes and quality improvements for automobiles as well as adjustments on transportation fees.

- On the flip side, clothing reflecting seasonality dragged the headline by 26bp, while the annual rate of price change in this group has remained in low single digits.

Finally, TurkStat, the statistical agency made usual revisions to the CPI basket by cutting the weights of alcoholic beverages & tobacco, clothing, transportation, catering, recreation & culture and education groups and adding to food, housing, household equipment, health, and communication.

Accordingly, the weight of the food group still remains the highest at 25.94%, followed by transport at 15.5% and housing at 15.4%.

Overall, another higher than expected change in January with across the board pricing pressures reflecting continuing cost-push factors, sticky services inflation, and deteriorating inflation expectations. Inflation will likely peak in April while exchange rate outlook, tax adjustments and expectations will remain key drivers for the inflation.

Given this backdrop, there is a shift in the central bank’s focus to medium-term and therefore, it turns more decisive on keeping a tighter stance for longer, also leaving the door open for more rate hikes. So, the Bank will remain cautious in the near-term given not only inflationary pressures, but also concerns about level and composition of reserves, high dollarisation and the need to maintain capital flows.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more