Growth In Turkey Moderates

Turkish GDP data showed a continuation of the rebound from the pandemic induced recession despite the mobility restrictions.

In the pandemic year, GDP expansion turned out to be strong at 1.8%, recording one of the best performances among the major emerging market countries vs 0.9% in 2019 and well above the government’s 0.3% projection.

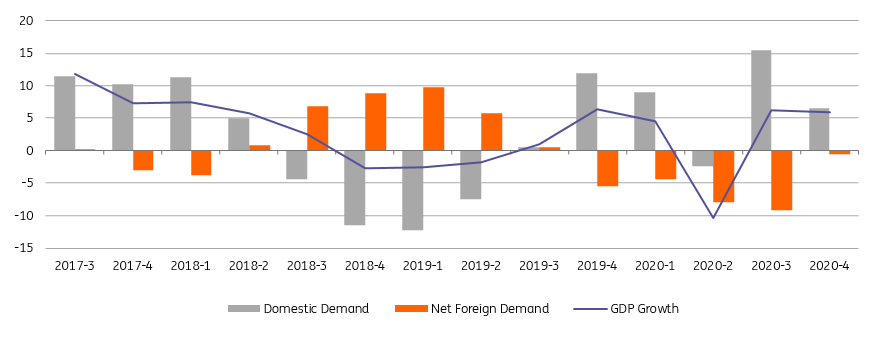

On a quarterly basis, 4Q GDP growth at 5.9% was lower than the market consensus at 7.1% (and our call of 6.5%). While losing some momentum in comparison to 3Q, the growth still remained buoyant as evidenced earlier by high-frequency economic activity indicators. The statistical agency, TurkStat also revised both 2Q and 3Q figures down to -10.3% and 6.3% respectively from -9.9% and 6.7%.

In seasonal and calendar-adjusted terms (SA), economic activity continued its recovery with 1.7% QoQ at a still higher pace, after a surge in 3Q thanks to the various stimulus measures and an accommodative policy stance to mitigate the adverse effects of the pandemic. The quarterly performance is driven mainly by net exports.

Turkish GDP growth

(Click on image to enlarge)

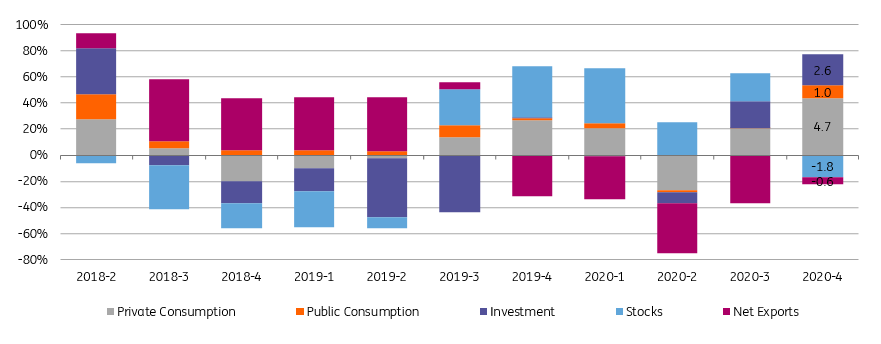

Looking at the spending breakdown, private consumption maintained its rebound with 8.2% YoY after another close to double-digit growth quarter in the previous quarter and turned out to be one of the major drivers with a +4.7ppt contribution to the growth in 4Q20.

There is still significant consumer credit momentum in private banks and the continuing impact of other domestic policy impulses despite intensifying efforts to unwind them should be the factor behind the private consumption growth. Investments maintained recovery with 10.3% YoY, translating into +2.6ppt contribution to the headline as companies, after a long delay after the August 2018 financial shock, has utilized pandemic related supportive measures to improve production capacity.

Accordingly, machinery & equipment investments recorded excessive growth rates in the second half of 2020, reaching 39% YoY in 4Q, while construction investments slipped into negative territory again weakening on the back of increasing mortgage rates. Public consumption that has lifted GDP almost every quarter since the second half of 2017 has remained supportive in 4Q, adding the headline +1.0ppt. After inventory buildup since 3Q19 markedly supporting the GDP performance, we saw the contribution of inventory drawdown with -1.8ppt.

These large impact of inventories in recent quarters likely reflect some measurement problems.

Breakdown of GDP

(Click on image to enlarge)

Finally, net exports remained a drag, reducing the headline growth by another 0.6ppt in the last quarter, though the adverse impact on the headline was moderated in comparison to previous quarters. This is attributable to a small rise in imports by 0.6% YoY given that exports were practically unchanged.

In the sectoral breakdown, all sectors except construction have lifted the headline growth showing a continuation of the broad-based recovery. Among positive drivers, industry was again the biggest contributor, pulling the fourth quarter performance up by 2.0ppt, followed by services with 1.1ppt which is a surprising performance given return of pandemic-control restrictions in early-November.

Overall, the data showed the continuation of the rebound from pandemic induced recession despite the revival of quarantine measures with the second wave in the Covid-19 pandemic. Despite some moderation over 3Q, 4Q GDP performance has remained strong driven by private consumption, gross fixed capital formation, and government expenditures while contributions of net exports and inventory were in negative territory.

The latest activity indicators hint at a strong start to this year and the carry-over effect from the last year should keep yearly growth high, though the pace of activity will likely lose momentum given significant policy tightening by BRSA and the central bank along with ongoing uncertainty.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does ...

more