Global Central Banks Outlook

The Federal Reserve's position of no rate hike until 2024 will be increasingly difficult to reconcile with the data, the European Central Bank will likely look through rising inflation and the Bank of England is likely to slow the pace of purchases this year.

Source: Shutterstock

The outlook for central banks

(Click on image to enlarge)

Source: ING

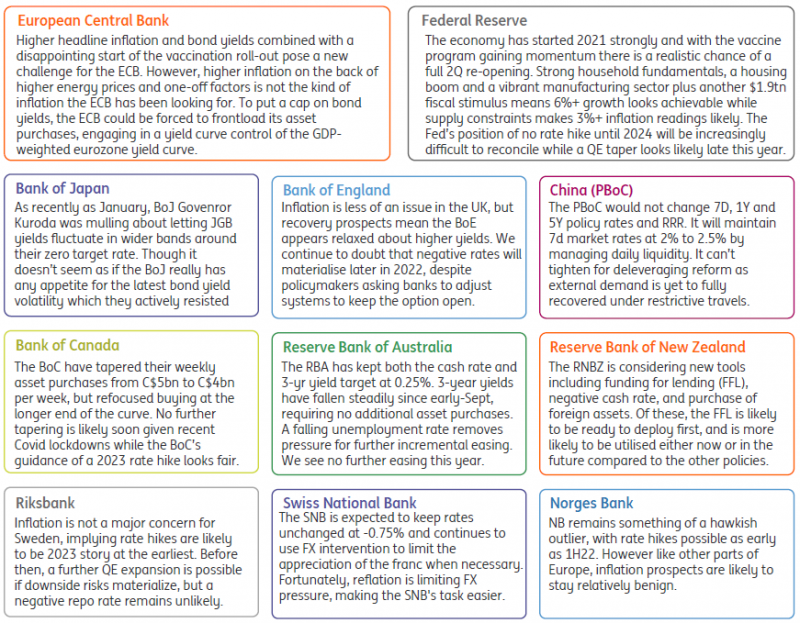

Federal Reserve

The economy has started 2021 strongly with the $600 stimulus payments boosting consumer spending while manufacturing and the construction sector are firing on all cylinders. With the vaccine program gaining momentum there is a realistic chance of a full 2Q reopening.

Household balance sheets are strong with high levels of savings and low levels of credit card debt meaning consumers have cash to spend. Significantly, this isn’t just for high earners, with extended and uprated unemployment benefits and stimulus cheques clearly benefiting lower income households. With another $1400 stimulus payment heading their way as part of President Biden’s $1.9tn fiscal package, 6%+ GDP growth looks achievable this year.

However, we anticipate some supply side capacity constraints in the service sector, which when faced with vigorous demand means 3%+ inflation readings are probable. Improved corporate pricing power and a roaring housing market could also make inflation somewhat sticky.

We suspect that the Fed’s position of no rate hike until 2024 will be increasingly difficult to reconcile with the data flow while expectations of quantitative easing being tapered this year are likely to grow. We would imagine the Fed would incorporate a “twist” whereby they would lower the $120bn of monthly purchases but focus them more towards the longer end of the Treasury curve.

Bank of England

The Bank of England appears to be taking a leaf out of the Fed’s book when it comes to the 50bp rise in yields we saw last month. Policymakers seem fairly relaxed so far, and in fact, we think it’s more likely that the pace of purchases is slowly lowered through the remainder of 2021 before the BoE stops actively expanding its balance sheet at the end of this year. A further QE extension can’t be ruled out if conditions warrant it, but it’s not our base case. As for negative rates, we think this is a path the Bank is unlikely to cross, despite the operational planning steps being taken to enable the policy’s usage from the autumn if needed. Several committee members remain unconvinced of the merits of negative rates, and in any case the economic outlook is unlikely to warrant a move given the improving economic outlook.

European Central Bank

Higher headline inflation and bond yields combined with a disappointing start of the vaccination rollout pose a new challenge for the ECB. The ECB’s current rather benign approach to inflation will be put to the test in the coming months as inflation looks set to reach 2% in the summer months, in our view. However, higher inflation on the back of higher energy prices and one-off factors is not the kind of inflation the ECB has been looking for. Consequently, we expect the ECB to look through higher inflation, but only as long as higher bond yields do not undermine what the ECB calls “favorable financing conditions”. To put a cap on bond yields, the ECB could be forced to frontload its asset purchases, engaging in a yield curve control of the GDP-weighted eurozone yield curve.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does ...

more