Germany, Rates And FX Markets: Preparing For The Elections

With less than five months to go before Germany's elections, the country's political landscape is preparing for both an exciting campaign and final vote. Fiscal spending and further European integration are key topics for markets. They could bring the end of negative yields and greater inflow into the euro.

The most open election in decades

In September, the German elections will be the first in decades in which the incumbent chancellor will not be running for re-election - an essential element to understand the current dynamics.

Angela Merkel is still one of the most popular politicians, and her party, the CDU/CSU, has long benefitted from the so-called “Amtsbonus”, the advantage of incumbency. With Merkel not running for re-election and growing frustration about the government’s mismanagement of the current phase of the pandemic, the CDU/CSU has dropped significantly in the polls. The latest controversy about who will lead the party into the elections seems to have contributed to fading electorate support.

Since Tuesday, it has become clear that the CDU/CSU will be led into the elections by Armin Laschet - the CDU party chairman and minister-president of North-Rhine Westphalia.

For the Greens, it will be Annalena Baerbock (if formally approved by the party assembly). Simultaneously, the SPD had already nominated the current finance minister Olaf Scholz as the party’s candidate for Chancellor. While the CDU/CSU was clearly ahead of the other parties last year when the pandemic was considered highly supportive for the executive’s popularity, recent polls have seen a dramatic decline in the party’s electorate support.

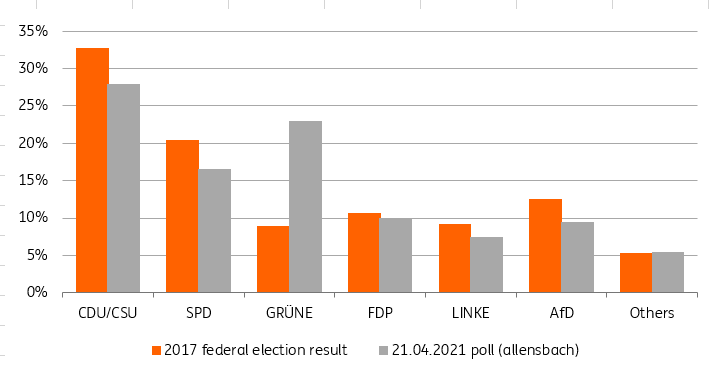

The open controversies and struggle between Laschet and Bavarian minister-president Markus Söder on the political leadership clearly contributed to the drop in the polls. According to the latest polls this week, the Greens have caught up the CDU, with the CDU dropping to a record low of 21% in a national poll, while others still put it ahead by a small margin.

Remember that in the 2017 elections, the CDU still had 32.8% of the popular vote.

Recent polls highlight the weakness of the incumbent CDU/CSU/SPD coalition

Sources: Allensbach, ING

In our view, these polls have to be taken with a large pinch of salt as the latest developments highly influence them.

Some political commentators have already warned that the combination of a weak party with a strong and popular lead candidate can work, but that the combination of a weak party with an unpopular lead candidate is risky. But don’t underestimate the support for the CDU, no matter how popular the lead candidate might be.

Even if other commentators have argued that Söder might have been the better campaigner for the CDU, but Laschet could be the better chancellor, with potentially more skills in managing a coalition. With the “Amtsbonus” of Merkel gone, the CDU/CSU and Greens are likely to be closer than ever in the final election results in September.

Even a Green chancellor should not be ruled out. Annalena Baerbock has never won an election, except various Green party leadership contests, but at least in other European countries, such a personal background has not stopped politicians from rising from obscurity to one of the highest political positions in a country.

In Germany, that would be a first.

Still a lot to play for before September

Fast-forward to September, a lot can still happen. To some extent, the outcome of the elections will depend on the success or failure of the vaccination campaign and whether Germans find themselves in a post-pandemic period or still in the thick of it. Economic topics like climate change, education, investments, etc., will definitely matter too - as they always have.

From an international point of view, the most important question will be what to expect from the next government in terms of fiscal and economic policy.

At the time of writing, all parties haven't published their election manifestos but gauging the available information, we would expect to see a similar trend like the Netherlands: a broad consensus for more public investment with nuances in size, purpose and financing.

Also, while the AfD has officially included a German exit from the EU into its manifesto, expect all other parties to be pro-European. Pro-European, however, does not automatically mean that a party is in favor of deeper integration. Therefore, when listening to German politicians, don’t judge them on being pro or anti-European but rather on being in favor or against deeper integration of the monetary union.

The discussion and position any next German government will take on fiscal policies will also have an impact on the eurozone debate, in which yet another revision of the fiscal rules will be discussed. However, don’t forget that any decision at the European level will in our view not be taken before the French presidential elections. As stated previously, further eurozone integration or reforms will remain paused until the summer of 2022.

A CDU/CSU/Green coalition as our base case

Our base case scenario for the German elections is a coalition of the CDU/CSU and the Greens after the elections. Such a coalition would favor more fiscal stimulus, continuing the line of the current government, with them stepping up investments.

This coalition would not let go of the constitutional debt brake but would rather find a workaround, e.g. in the form of a special-purpose vehicle, an investment vehicle to finance investments in digitalization and to tackle climate change. In this scenario, Germany (and the eurozone) would see more fiscal stimulus, probably similar to the currently discussed investment plans in the US.

The second most likely coalition would be the Greens leading a Green, CDU/CSU coalition. Policies here would hardly differ from the base case scenario.

Other coalitions with currently equally very low probabilities would be:

- CDU/CSU, Greens and FDP. This Jamaica coalition was the first option after the 2017 elections, but the coalition talks failed. In terms of fiscal policy, we would also see more investments but a quicker return to austerity, on the back of public expenditure cuts and not so much higher taxes

- Greens, SPD and Left Party. This would be an unprecedented coalition at the left side of the political landscape. This coalition could bring an end to the constitutional debt brake, would also see more fiscal stimulus with a focus on redistribution and eventually a return to austerity financed by higher taxes.

- Another revival of the current grand coalition CDU/CSU and SPD. This coalition will only be an option if all other options have failed or if no other option is possible. It would be another continuation of the status quo.

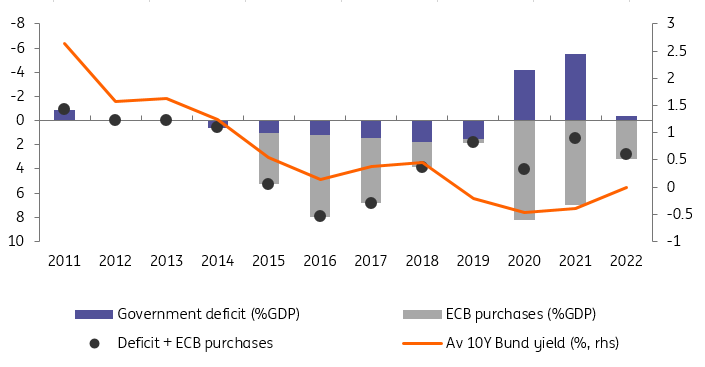

German Bund: Goodbye negative yields

With the two most probable coalition configurations likely to favor public investment and European integration than in the past decade, it is legitimate to question the paradigm that has sustained exceptionally low German yields over that period.

On the first point, the fiscal response to the Covid-19 emergency has already somewhat remedied the insufficient amount of safe assets issued by the German government. The problem is, the European Central Bank has absorbed more than the new debt issued since 2020 in its purchase program, resulting in negative German yields. It would take a sustained commitment to run deficits in the coming years to alleviate that chronic shortage, something even a Green-led coalition might not be ready to contemplate. However, at the margin, a return to a healthier level of public investment and accompanying growth would help unwind some of the scarcity premium behind extremely low Bund yields.

Falling German yields have come with fiscal surpluses and ECB purchases

The second point, pertaining to European integration, is an extension of the first. A new coalition looking more favorably towards further European integration, especially if it enshrines the functioning of the EU recovery fund in a more permanent form of EU budget, would contribute to greater fiscal spending at the European level. What is more, any further debt financing would also go some way towards alleviating the scarcity of safe bonds in the Eurozone, and push yields up.

However, European integration is more than a way of circumventing German aversion to budget deficits. Its redistributive nature, and the common liabilities it entails, would stand a chance of reducing economic disparities among EU member states, and thus the differential in credit risk between debt issuers. The result would be that investors feel more comfortable divesting German Bund and investing in the hitherto riskier sovereigns. An added benefit would be to ease pressure on the ECB to maintain an exceptional degree of monetary accommodation, and thus allowing them to run higher base interest rates over time.

On either front, the changes brought by a new coalition will likely prove incremental. Inasmuch as it would strike at the heart of both Bund scarcity, and of the lack of European integration until recently, this election could prove decisive for Bund valuation. Watch both topics during the campaign. If they gain traction with both main parties, negative yields could become a thing of the past.

FX markets: A better policy mix for the EUR

As above, while any policy changes may prove incremental, the direction of travel towards looser fiscal and tighter monetary policy would be a more positive policy mix for the EUR.

Looser fiscal policy would presumably help towards a re-rating of the German and European growth story and encourage equity flows into the region. Buy-side surveys show that investors have increased overweight positions in European equities over the last year – but nowhere near the conviction levels seen in 2017 and early 2018. Steeper yield curves led by the Bund sell-off would also support flows into financials and European equity benchmarks in general, where financials have higher weightings than their US counterparts.

For reference, the renewed sense of optimism in Europe after the French Presidential election in Spring 2017 did certainly garner fresh international interest in Eurozone equities as witnessed by flow into the iShares MSCI Eurozone ETF. As noted above, however, and in a recent note, a stronger re-assessment of the European project may have to wait until after French presidential elections next Spring.

The narrowing in the US Treasury/Bund differential would also slow the recent pick-up in Reverse Yankee corporate issuance as US borrowers have sought to take advantage of cheap EUR borrowing rates to swap funds back to the dollar. Heavy issuance here has tended to weigh on EUR/USD.

To conclude, any further progress of the Greens in the polls would probably be taken well by the EUR and would add to our cautiously positive forecast of EUR/USD moving above 1.25 later this year (FXB,UDN).

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

{kind=link}