Eurozone: Uncertainties Are Weighing On Growth

The eurozone economy is slowing down and with Brexit and the trade war tensions weighing on confidence, a further deceleration looks likely. If a hard Brexit were to materialize and Europe was targeted in the evolving trade war, it would be hard to avoid a technical recession and the ECB would have to act on its words.

Source: Shutterstock

From left: German Chancellor Angela Merkel, Christine Lagarde, European Commission President Jean-Claude Juncker, and European Central Bank Governor Mario Draghi

The hoped-for growth acceleration is not happening…

The hoped-for acceleration in economic activity is not happening. A number of risks could further weigh on eurozone GDP growth in the second half of the year and the first half of next year. With inflation still moribund, the European Central Bank is set to loosen monetary policy again. However, the marginal impact of further easing is getting smaller. At this juncture, fiscal policy would likely be more effective, but for the time being the countries with the most budgetary space are dragging their feet.

...with the risk that weakness could spread

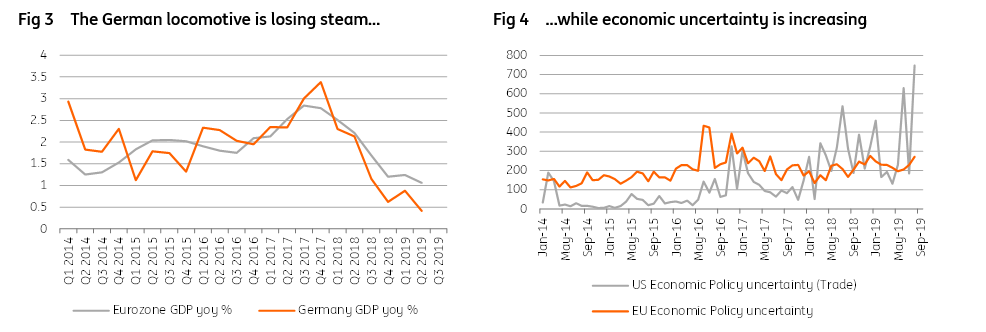

The eurozone economy grew by a non-annualised 0.2% in the second quarter after 0.4% growth in the first. But powerhouse Germany actually shrank 0.1% in the April-June period. This continues to reflect the dire situation in manufacturing, which has been hit by the trade war-induced softening of international trade (the manufacturing sector is relatively more important in Germany than in the other member states while the specific shock to the automotive sector also plays a role). Services are still holding up in the eurozone. And while the consumer still benefits from job growth and some increase in purchasing power, there is always the risk that a more uncertain economic environment leads to more savings instead of more consumption. The same story applies to business investment, which might suffer from uncertainty even if financing conditions remain extremely attractive. Also, bear in mind that capacity utilization in manufacturing is relatively high.

(Click on image to enlarge)

Source: Refinitiv Datastream

Italian political situation is stabilizing...

On a positive note, it seems that Italy is not heading for new elections after all, because an alternative majority between the 5 Star Movement and the PD is being put in place. This government would be led by current Prime Minister Giuseppe Conte and is unlikely to pick a fight with the European Union on the budget. The strong decline in Italian bond yields seems to corroborate this expectation.

... but Brexit might just push the eurozone into a technical recession

However, Brexit remains a major risk for the growth outlook in the eurozone. While numerous studies have tried to compute the long-term negative effect of a hard Brexit on the rest of the European Union (with figures ranging from 0.3% to 1.5% of GDP), it is obvious that trade distortions will have a negative impact in the short run. We could easily see a negative growth impact of 0.1% to 0.2% both in the last quarter of 2019 and the first quarter of 2020, which might push the eurozone into a technical recession.

The trade war is not over yet

At the same time, the trade war is still not resolved. While Donald Trump might decide to delay his decision on tariffs on European cars, he will still the possibility open to put pressure on European negotiators during the trade talks. Even though 2020 would therefore not see higher tariffs, the uncertainty will continue to weigh on sentiment of European producers. If alternatively, the trade war would escalate in 2020, we might easily lose another 0.2 percentage points in GDP growth.

GDP growth llikely to fall below 1% in 2020

For the time being, we are witnessing a growth slowdown, though the economy is certainly not falling off a cliff. August’s economic sentiment indicator saw an unexpected uptick, while monetary aggregates also point to some underlying growth momentum. That said, even though a hard Brexit is not our base case right now and we think that Trump will not drive the trade hostilities to a point where they could jeopardize his re-election, we think it’s wise to reflect some of these uncertainties in our growth forecasts. After all, the uncertainty itself could sap ‘animal spirits’. We have therefore revised our 2020 GDP growth forecasts downwards to 0.7%, after 1.1% in 2019.

ECB: Lower for longer

Meanwhile, inflation seems to be stuck at 1%. With growth decelerating, it is hard to see much of an increase, even if labor markets remain relatively tight. Together with slowing growth, this should push the ECB into more easing. While we doubt that more monetary easing will generate much of a growth effect, doing nothing is not an option anymore, as markets have already priced in additional easing.

We expect a 20 basis point deposit rate cut, a tiered interest rate system for excess liquidity, more generous TLTRO conditions and €30 billion per month of quantitative easing (though this last point is still being discussed and could be delayed to wait for the Brexit outcome). All of this means that bond yields are unlikely to rise much over the forecasting horizon. Some steepening of the yield curve is possible when the major uncertainties have finally lifted (and we might eventually also see some budgetary stimulus), but even then the 10yr bund yield is likely to remain firmly in negative territory.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more