Eurozone Labor Shortages Unlikely To Become A Structural Problem Quickly

Labor shortage isn't such a big issue in the Eurozone, as is the case in the US, but as the economy re-opens in full force, this theme is likely to surface evermore. But over the medium term, we think a scenario of a slowly recovering jobs market is more likely to emerge than one with structural shortages.

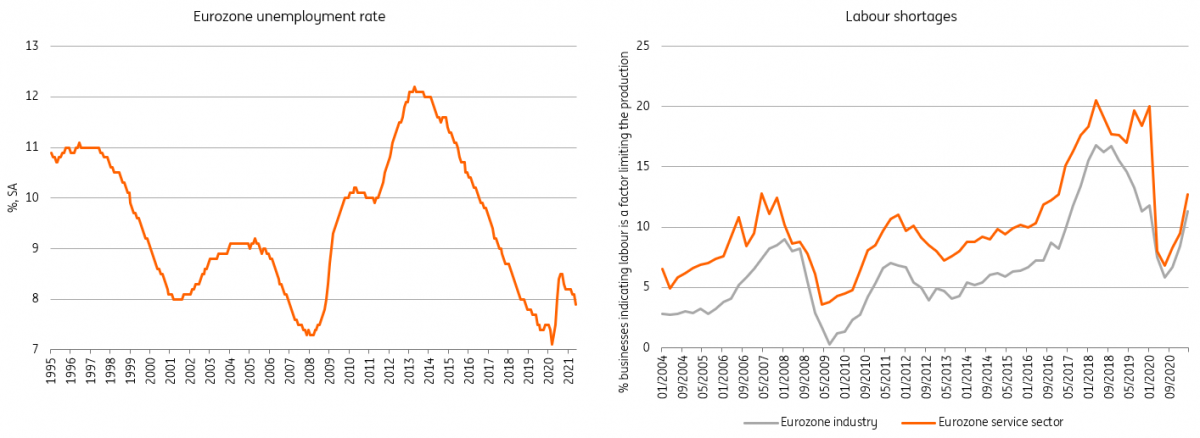

Unemployment is less than 8% but labour shortages are creeping higher

We’ve said it before, and we’ll say it again - this crisis is not like others.

Despite the historic shock to GDP, unemployment in the Eurozone is now only 0.8 percentage points higher than the pre-pandemic low of 7.1%.

Over the course of the second wave of the pandemic, unemployment didn't increase and instead continued to fall from the highs seen in August 2020 when it was at 8.7%. At face value, this gives the impression that a tight labour market and strong wage growth could return sooner than expected, especially as businesses are reporting concerns about finding right workers. The number of businesses indicating labour availability is limiting production has increased up to about 12%, which is still below 2019 levels but historically quite high.

More labour shortage reported as unemployment begins to fall again

(Click on image to enlarge)

Source: Macrobond, ING Research

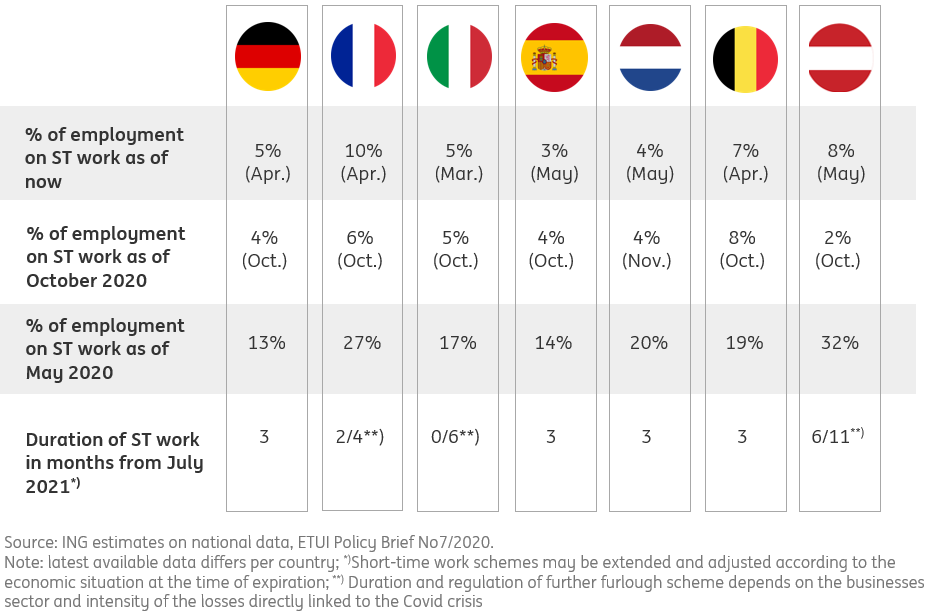

Eurozone furlough schemes still cover substantial part of employment

But this can be deceiving when forming a view on the labour market though.

Hours worked were still 6.5% below pre-pandemic levels in the first quarter, which is a much larger gap than what was seen during the financial crisis. The unemployment rate has remained as low as it is mainly because of furlough schemes, and its widespread use has radically changed the labour market impact of the GDP shock.

In the second wave, as unemployment continued to fall, we estimated that the percentage of employment covered by furlough schemes did not fall. So also in the very mild second wave labour market shock, furlough schemes mitigated unemployment impact. Data on furlough scheme take-up is lagged though and therefore latest developments are hard to monitor, but both in October 2020 and February 2021, we forecasted 6% of the number of employed in the eurozone were still subsidised by governments.

It’s hard to estimate what percentage of those will find themselves without a job when the scheme ends, the situation will have a lot to do with the state of the labour market when the programmes end. As we expect synchronised upturns across the eurozone in the coming quarters, it is quite probable that the ultimate impact on unemployment at the end of the schemes could be relatively small.

However, when businesses start to restructure, especially in countries like Italy where layoffs are prohibited while making use of the scheme, job losses may become sizeable. That means that outflows from the workforce will result in higher unemployment, leading to a longer period of labour market recovery than the current unemployment figures suggest.

Short-time work schemes across Europe: where are we?

(Click on image to enlarge)

Source: ING Research

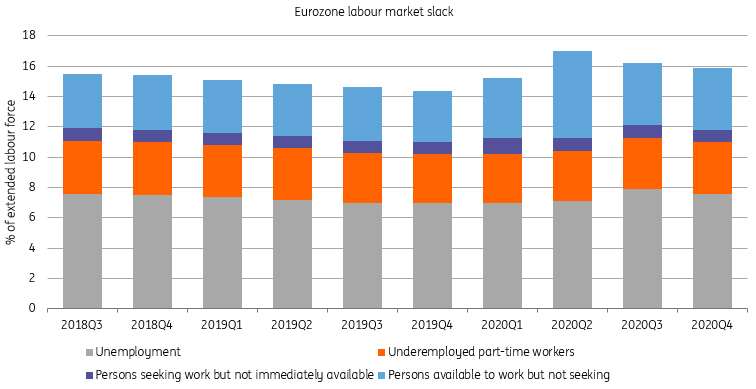

Broad labour market slack is still 2.4 million people more than what it before the pandemic

Besides furlough schemes, there is significant hidden slack in the labour market.

The number of people that would like to work but are not looking – and therefore do not appear in the unemployment figures – is still higher than during the financial and the euro crisis in 4Q. This means that plenty of people are still on the sidelines and who will only come back to the job market when they are comfortable with the associated health risks. Think of migrant workers who moved back home to avoid travel difficulties or students who moved back in with parents, or when the economy looks hot enough for people to feel confident enough to start applying again. This amounts to 1.3 million people more than before the pandemic.

Other factors usually considered are part-time workers that would like to work more hours, but that has not increased significantly, so additional slack is mainly found in people that have stopped looking for work during the pandemic. In total, labour market slack is now 2.4 million people more than before the crisis.

Labour market slack is still elevated, mainly thanks to dropouts

(Click on image to enlarge)

Source: Eurostat, ING Research

Increased vacancy rate imply late-pandemic mismatches, not structural issues

The reopening phase comes with labour market hiccups, as we are witnessing in the US right now, but we expect these issues to be mostly temporary given the furlough schemes covers substantial amounts of employment.

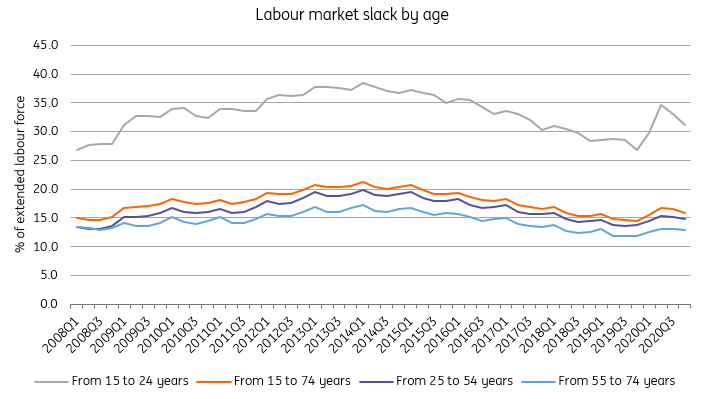

Another issue is the sheer number of people sitting on the sidelines of the labour market for now, as evidenced by the shortages experienced in low-wage hospitality and retail sectors.However, we think this issue is also temporary as a large pool of the people sitting on the sidelines consists of 15-24 year-olds who would most likely be doing these jobs.

Besides being usually higher, labour market slack has grown disproportionally among the young

Source: Eurostat, ING Research

Labour shortage isn't such a big issue in the Eurozone, as is the case in the US, but as the economy opens in full force, this theme is likely to surface more.

We expect most pressing shortages to alleviate as more people are vaccinated, travel becomes easier, in-person teaching restarts etc. We expect more churn in the labour market, especially when the furlough scheme ends.

Over the medium term, a scenario of a slowly recovering job market is more likely than one in which structural shortages emerge quickly.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more