Eurozone: A Labour Market In Surprisingly Good Shape Ahead Of The Second Wave

Too good to be true or merely another weird feature of the extraordinary downturn that the coronavirus causes? Thanks to government support, significant unemployment increases have been avoided up to now. However, with the second lockdown wave in full play and a looming wave of insolvencies, unemployment looks set to increase in 2021.

Short-time work schemes do what’s on the ticket

According to the latest data for October, unemployment in the eurozone has been declining since July. What is quite remarkable for a shock this unprecedented is that the unemployment rate was just 8.4%, up just 1.2 percentage points from February 2020. For a labour market that is known to experience peaks in unemployment in excess of 10%, this is extraordinary and provides a strong buffer for the impact from the second wave.

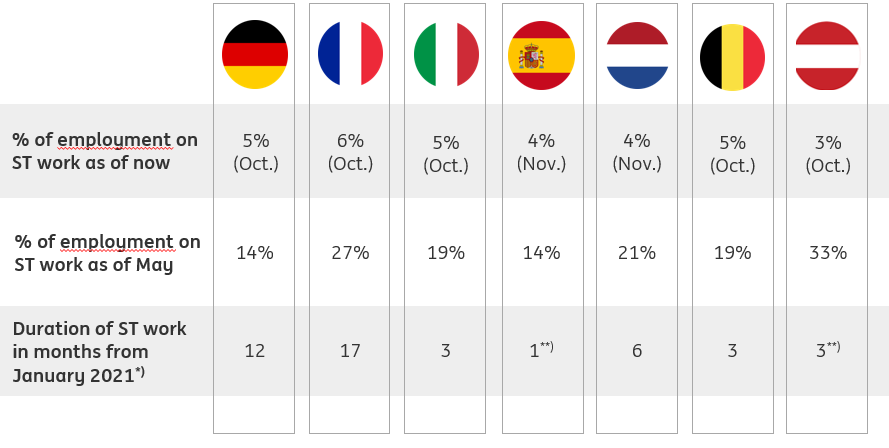

To explain the modest impact on unemployment so far, it is important to take a closer look at short-time work developments. Short-time work schemes across the eurozone have caused large labour market distortions as they have subsidized a very sizable amount of employment. See table 1 below for the current state of short-time work schemes, which indicates that around 5% of total employment is still covered by short-time work. The share of total employment covered by the schemes has fallen dramatically since May though as economies have been recovering. As unemployment has not increased much since then, the schemes have been quite successful in mitigating job losses in times of economic shock.

With still relatively many jobs supported by the schemes, the question is how long the schemes will continue now that the second wave is hitting, and new lockdowns cause a similar situation compared to the difficult first wave. According to latest data out of Germany, the number of people in short-time work increased again in November and December.

Most short-term work schemes have been extended until the end of 1Q21

For many countries this is not an imminent issue as most short-time work schemes had already been extended until the end of 1Q21. Only Spain stands out as a worrisome case, where the short-time work scheme is due to expire at the end of the month, but it has been already announced that talks about an extension of the scheme will take place on 8 January. A lengthening seems necessary to avoid a further sizable increase in unemployment. However, the longer the lockdowns last, the higher the risk of companies going bust. In such a scenario, unemployment would increase independent of government support schemes.

Short-time work schemes, where are we?

ING estimates on national data, Eurostat

Note: latest available data differs per country, Netherlands data is until 26 November; *)Short-time work schemes may be extended and adjusted according to the economic situation at the time of expiration; **)negotiations about extension already planned

Those extensions of the scheme do often include somewhat less favorable conditions than at the start of the crisis though. France, at 6%, is still high on the list of large eurozone economies leaning on short-time work, and is expected to make conditions less attractive at the end of the month though – increasing the employer contribution from 15% to 40% of the benefit. All in all, short-time work is likely to continue to support the labor market through the difficult second wave in most large economies but take-up could become smaller under less favorable conditions.

Broad measures of unemployment show strong recovery after lockdown 1

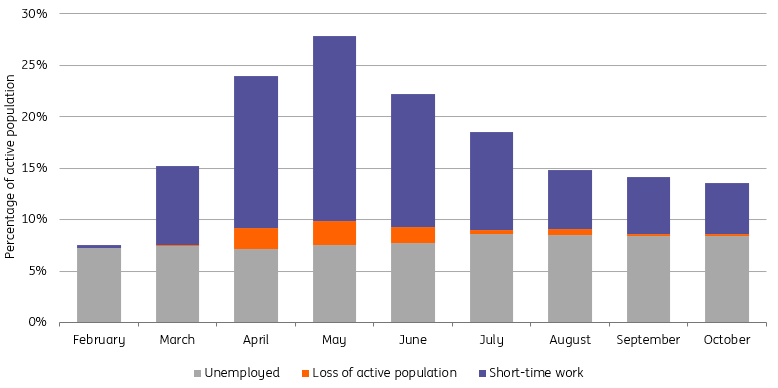

To get a better sense of actual labor market workings during the corona crisis, we use a broader measure of unemployment to look at how the labor market has developed. We add our estimate of the number of people on short-time work schemes to the number of unemployed and take an estimate of the monthly change in the active population to account for labor market dropouts (people not looking for work anymore and therefore not counting as unemployed). The latter is a very rough measure, but the best we can do using monthly eurozone data.

What we find is that the peak in combined inactive people was between 25% and 30% of the labor force in May, after which a rapid decline occurred to about 15% in October. The curve has flattened over recent months. This still leaves a sizable amount of the labour force on short-time work, but at the same time unemployment has also been declining significantly and the increased number of inactive people has vanished as the labor force is almost back to February levels. This is a remarkable recovery given the historic economic shock we experienced in the first lockdown last spring.

Broad labor market measures show a quick recovery from the first wave

ING Research, Eurostat, national sources on short-time work

Is this first wave impact too good to be true?

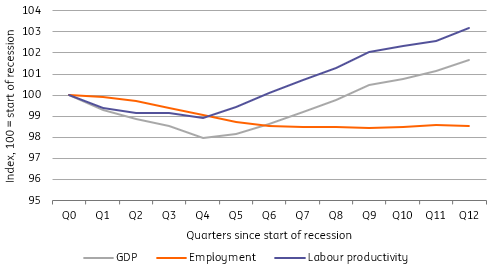

While many comparisons with prior recessions fall flat, it is interesting to keep in mind how employment developed in the aftermath of past eurozone recessions. Chart 3 shows the development of GDP, employment and productivity per worker over the course of the past five recessions in the eurozone. This shows continued employment declines until after labor productivity has recovered to the pre-crisis level.

We were still far from that level in the third quarter – partly the flipside of the short-time work schemes – with productivity some 2% below its pre-crisis peak. Consequently, additional employment drops are still on the cards. Even if this is no ordinary recession and without the impact from the second lockdown as well as the structural impact from insolvencies, historical comparisons suggest that we are set for a sluggish job growth performance in 2021, at best.

Eurozone employment usually doesn’t recover until labor productivity has reached pre-crisis levels

ING Research calculations, CEPR Euro Area wide model, Eurostat Note: average of the 1974, 1980, 1992, 2008 and 2011 recessions

Unprecedented crisis – also for the labor market

Unfortunately, this is no crisis like any other crisis. There are two important factors complicating any forecast for the eurozone labor market: the second lockdown and the uncertain lasting impact of the first. The massive amount of stimulus that governments have provided has in part avoided economic misery. However, some argue that parts of misery have only been delayed. When businesses come off short-time work schemes, some workers will still be laid off as businesses restructure, but perhaps more importantly: bankruptcies have also been massively suppressed by many support measures like deferred taxes or loan moratoria. That has pushed many financial obligations out to 2021, causing bankruptcies in 2020 to be far lower than even in good economic years. That makes it more than reasonable to assume a catch-up in bankruptcies once support measures are withdrawn, leading to higher unemployment.

All in all, the impact of the second wave on the labor market is hard to quantify as countries are still in the process of extending or deepening restrictive measures to contain the virus as we speak. Even if the performance of the eurozone labor market in 2020 was encouraging, successes of the past are unfortunately no guarantee for future success.

Although a recovery is set to take firm hold from 2Q onwards, mild increases in unemployment are still expected

While the recovery is set to take a firm hold of the economy from the second quarter onwards, mild increases in unemployment are still to be expected due to the delayed labor market impact of several economic shocks. In particular, a rise in insolvencies is probably the biggest threat to the labor market in 2021. Judging from previous experiences, we would be surprised if unemployment would ultimately run up nearly as high as during the euro crisis. However, it only needs up to 33% of all people currently working under short-time work schemes eventually losing their jobs to push eurozone unemployment above the 10% mark. Needless to say, governments will try everything they can to prevent such a scenario.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more