Euroflation: The EUR Reflation Trade And Its Market Implications

EUR interest rates and, more noticeably, inflation swaps have been rising in tandem with their USD counterparts. The move rests on the shaky fundamental ground but could run ahead with US markets poised to drag the rest of the world out of its gloom. We look at the curve and consider broader market implications.

The Eurozone reflation trade: hard to justify with fundamentals

The ‘made in the Eurozone’ reflation trend shares many of the characteristics seen in other developed markets, chiefly in the US. If a correlation between global markets is not a new phenomenon, the rationale in the Eurozone is harder to make sense of. We wrote in our 2021 outlook that the divergence between USD and EUR rates markets would be one of the key themes of the year. This has largely proved true for nominal rates…but inflation expectations have been rising apace on both side of the Atlantic.

inflation expectations have been rising apace on both side of the Atlantic

The Eurozone economy remains dogged by harsher lockdown policies than in the US, a slower vaccine rollout, and, most importantly, more limited hopes of fiscal stimulus. As such, the Eurozone reaching ‘escape velocity’, the point where growth is sufficient for stimulus to be withdrawn, is but a distant prospect.

To be sure, some global developments could prove this analysis wrong. For instance, goods inflation, a more global phenomenon than service inflation, could pick-up as the global economy recovers. Rising commodity prices are also finding their way in prices. It is likely that these effects would prove transient, however. Longer-lasting inflation would have to rely on higher wages. By and large, the rise in Eurozone inflation that our economics team expects this year should not last, and medium-term price pressure remains weak.

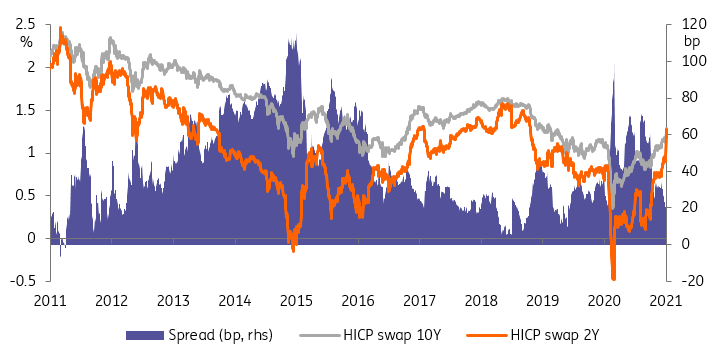

EUR inflation swaps have risen much faster at the short-end

Source: Refinitiv, ING

Reflation and the curve: steeper nominals ahead

If there is a place where a temporary rise in inflation is justified, it is to be found at the short-end of inflation swaps. And indeed, the rise in 2Y inflation swaps has outpaced 10Y. This has only occurred twice in the past ten years. Once in 2011, and once in 2018. In both instances, market concerns about the risk of premature ECB tightening grew quickly.

This time could be different. Inflation swaps anticipating inflation of 1.32% over the next two years hardly cause for concern at the ECB. Neither is 1.27% average inflation, also implied by swaps, over the next 10 years. Nevertheless, inflation expectations are an important input in interest rates, and interest rates are input in all other markets.

Inflation of 1.32% over the next two years is hardly cause for concern

One important fact about long-term (10years) inflation expectations as implied by swaps is that they have been on a clear downtrend since the great financial crisis. It is all well and good to aim for expectations rising back to the levels prevailing in the previous cycle, around 1.5% in 2018, but when it comes to breaking higher, the burden of proof lies with those calling for a change in long-term inflation dynamics.

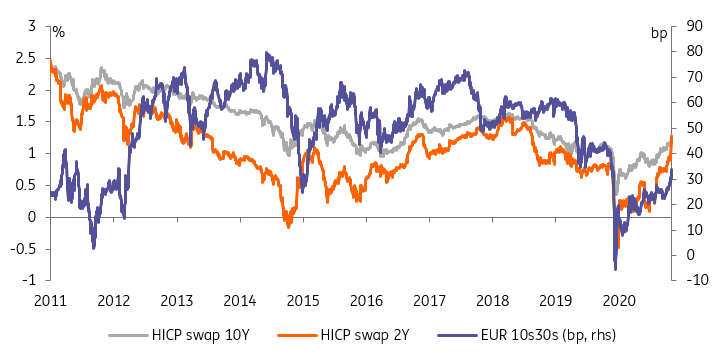

Interestingly, past relationships between long-term inflation and the slope of the EUR nominal interest rate curve suggests EUR 10s30s (to take that example) should lie somewhere around 45bp, from 35bp currently. 10-year inflation swaps at 1.5% would be consistent with 10s30s at 60bp. In short, even as the inflation swap slope is inverting the 2s10s, the nominal rates slope steepening appears to have only begun.

Rising inflation expectations imply a steeper curve is necessary

Source: Refinitiv, ING

Real rates at record lows: a few more weeks of goldilocks

As we hinted above, the implications of higher inflation, higher nominal rates, and of a steeper curve do not stop at interest rates markets. We let individual strategy teams detail the implications for their respective markets but one general point is that there is a solid theoretical basis to believe that real rates, the difference between nominal rates and inflation expectations, matter for risk appetite in financial markets.

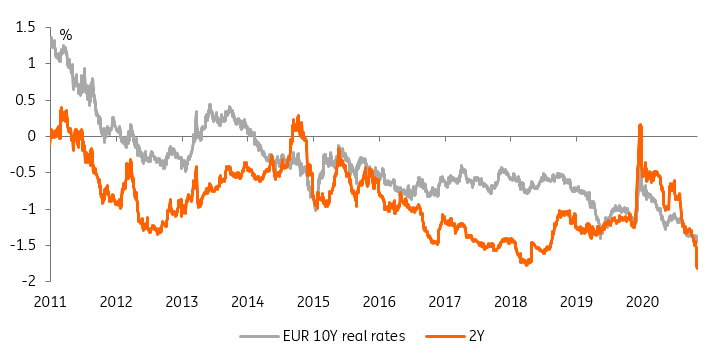

Real rates are at record lows at both ends of the curve

Source: Refinitiv, ING

By that measure, with both 2Y and 10Y real rates at record lows, one could conclude that financial conditions are exceptionally accommodative. Interestingly, the ECB is in the midst of a debate on what the definition of favorable financing conditions should be. ECB president Christine Lagarde has hinted that the answer when it eventually arrives, will rely on a broader set of indicators than just interest rates. It is clear to us, however, that low-interest rates, tight credit spreads, and buoyant stock markets put in the context of rising inflation expectations indicate a degree of disconnect.

Higher rates now, sowing the seeds of lower rates by year-end

Barring a hawkish ECB communication accident (or one from the Fed) we see this state of play extending for a few more weeks to a few more months. It should turn when one of two things happens. Either economic hopes are proved correct by data later this year, or they aren’t. In the former case, the debate about withdrawing monetary accommodation will heat up, and nominal rates will catch up higher to inflation swaps. In the second scenario, inflation swaps will converge lower towards nominal rates in pricing dim economic prospects.

We continue to doubt 10Y nominal EUR swaps will end the year above 0%

Either way, higher real rates will usher a more challenging period for risk appetite, one that would see nominal rates drop or remain low, by virtue of safe asset demand for government bonds. In that respect, the higher the spike in real rates in the first half of 2021, the lower nominal rates will be pulled by the end of the year. We continue to doubt 10Y nominal EUR swaps will end the year above 0%, but they may well test that level in the coming months.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more