ASIA-PACIFIC RECAP: STOCKS, SOUTH KOREAN WON NURSES LOSSES

Global equity markets appear to be mounting what could be the early stages of a recovery after experiencing two days of intense selling pressure. S&P 500 (SPY) futures spiked approximately one percent in Tuesday’s trading session with the South Korean Won gaining despite a growing number of cases both domestically and internationally. The source of renewed risk appetite may have originated from news of Japan confirming the test of an anti-flu drug on coronavirus patients.

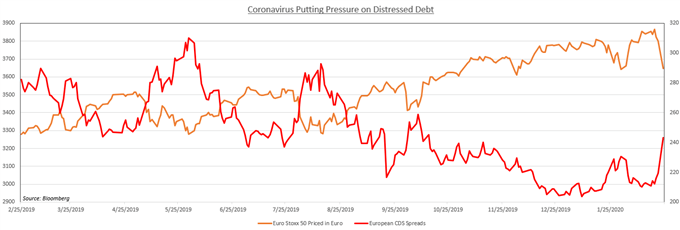

EURO AT RISK FROM FRAGILE EUROZONE CORPORATE DEBT

On Monday, the Euro Stoxx 50 index plunged 3.5 percent, while the cost of insuring sub-investment grade corporate entities surged to its highest level since October. The spread on credit default swaps for Mediterranean sovereign debt also rose, particularly in Italy (EWI) where the government has shut down 10 towns in an effort to stop the spread of COVID-19.

Policymakers are growing increasingly concerned about the durability of corporate debt in a downturn and whether it could spark a cross-continental contagion effect. In the Eurozone (EZU), the appeal of so-called leveraged loans and their high-yielding features made them particularly attractive in a low interest rate environment. Consequently, investors have begun to gain exposure to increasingly higher yielding and riskier assets.

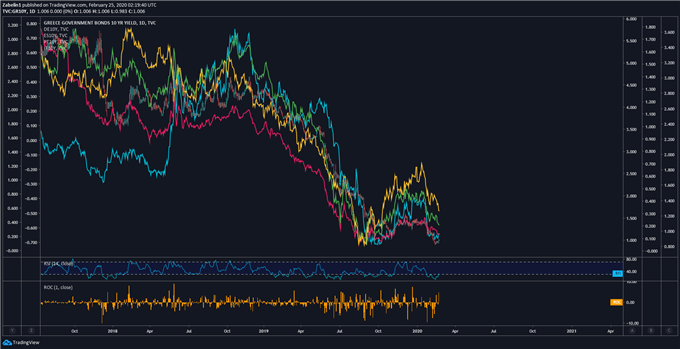

This came amid a regional convergence of interest rates on sovereign debt in Greece (GREK), Germany (EWG), Italy Portugal (PGAL) and Spain (EWP). What this means is the risk premium between owning Mediterranean debt – with a history economic precarity – and German bunds – with a reputation of financial soundness – has collapsed and is approaching equivalency. But why is that important?

10-Year Yields on German, Spanish, Greek, Portuguese and Italian Sovereign Debt

This implicit message behind this convergence is investors are assuming that “all other things equal”, these states will be almost equally able to meet their debt obligations. History says otherwise, and the current fundamental context only supports the notion that the Southern member states are still comparatively more vulnerable than their northern counterparts.

However, buoyant market optimism – buttressed by expectations of central bank easing – has alleviated the anxiety of a region-wide default. Consequently, investors have grown more comfortable with investing in riskier assets (both sovereign and corporate) while underwriting standards for the latter deteriorate. The coronavirus has revealed that these debt markets are more susceptible to economic shocks than imagined.

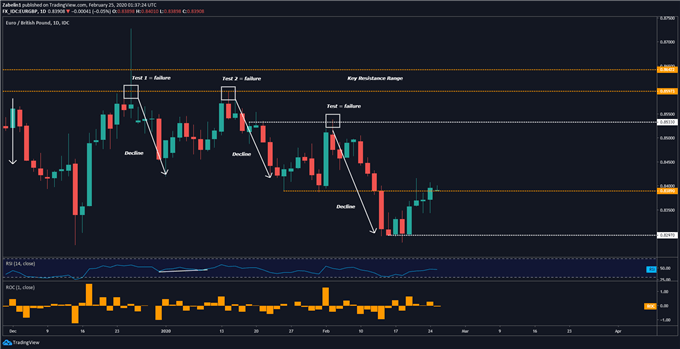

EUR/GBP FORECAST

EUR/GBP has bounced back from the swing-low at 0.8297 and is now testing its strength as it wrestles with resistance at 0.8389. If the pair is able to surmount the ceiling, it opens the door to retesting resistance at 0.8533 where the EUR/GBP failed to clear it back in early February. However, if the pair is unable to clear the near-term barrier, it may leave discouraged traders in the dust and cause a retreat to 0.8297.

EUR/GBP – Daily Chart

EUR/GBP chart created using TradingView

Comments

Log in or sign up to join the conversation.