EUR & ECB Cribsheet - Tuesday, October 27

The ECB is moving closer towards more action, but it is too early to do so this month. While we look for a dovish bias and hints at more asset purchases (to come in December) this should not catch markets off guard. The impact on EUR/USD, which has been relatively resilient during the latest de-rating of the eurozone growth outlook, should not be overly negative.

Source: ING

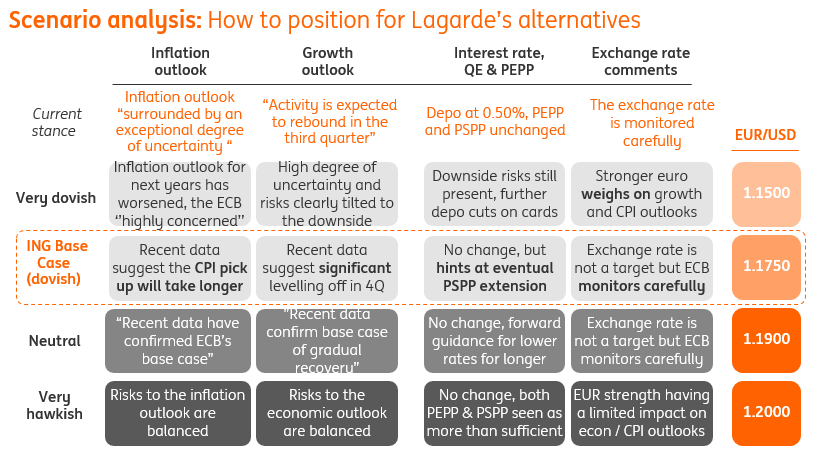

Shifting focus from comments on the exchange rate to hints at more bond-buying

With the eurozone inflation outlook already deteriorating for some time and the new wave of Covid cases across Europe now translating into the additional de-rating of the EZ growth outlook for the winter months, the ECB is moving closer towards another round of easing.

Compared to the September meeting, the focus will not be so much on the ECB comments on the exchange rate. Since the September meeting, the euro stabilized due in part to the deteriorating EZ economic outlook, hence no need for urgent verbal intervention. Instead, all eyes will be on hints at further easing, likely via the additional bond purchases. As per the ECB Preview, we think it is too early for specific measures to be announced at this meeting, but the guidance is likely to hint at more asset purchases (likely via the Public Sector Purchase Programme) to eventually come.

EUR downside limited as the market expects the ECB to act later this year

While not a positive for the euro, the scale of the euro downside should be limited in response to the ECB meeting. This is because the market has already assigned a high probability to additional easing measures being rolled out in the December ECB meeting. The latest Covid wave in Europe, the rise in restrictions, and the resulting downgrades to the EZ growth outlook further cemented such expectations.

With the recent ECB working paper pointing at the effectiveness of asset purchases in influencing the exchange rate (its strength has been a clear headache for the ECB this summer) and a very high bar for moving rates into further negative territory (given its effect on the banking sector) more asset purchases seem to be the widely anticipated way forward at this point. Hence, hints at such measures should not catch the market off guard and thus have a limited negative impact on the euro (particularly if the size of the asset purchase extension will not be announced).

For the amount of bad news, EUR/USD has been very resilient

Despite the second wave in Europe, the material downgrades to the near-term EZ growth outlook and the market expecting more easing from the ECB at the end of the year, EUR/USD has been fairly resilient for the amount of EUR specific negative news. The fact that the pair is not far from the 1.20 level (its high during the peak of the positive re-rating of the EZ growth outlook in the summer) provides the case in point.

In our view, this is partly because markets (and ourselves included) continue to stick to the glass-half-full view and consider the rise in Covid cases and the associated EZ slowdown as temporary. With the outlook for the next year remaing constructive (eventual EZ recovery after a tough winter; the Fed being intentionally behind the curve and this translating into weaker USD dynamics), it is difficult to argue for a materially and persistently lower EUR/USD. Hence the relative EUR/USD resilience so far and thus the not overly detrimental expected effect on EUR from the eventual additional ECB easing.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more