ECB: Rates Spark

Tapering fear is not affecting all financial markets alike, reflecting the nature of purchases, but also the drama surrounding each ECB meeting. Record low real rates suggest very accommodative conditions; any display of optimism in today’s minutes will be reflected in higher bond yields, and cheaper asset swap spreads.

Euro government bonds are the epicentre of tapering fears

No-one said the road to a world where central banks need normalising monetary policy would be a smooth one, but the process is delivering some interesting contradictions in financial markets.

Tapering of ECB asset purchases seems to be more of a concern than the same prospect from the Fed

There is of course the fact that, comparing USD and EUR rates movements, a tapering of ECB asset purchases seems to be more of a concern than the same prospect from the Fed. Granted, ECB communication has put increased emphasis on meeting-to-meeting decisions, but the policy space for monetary tightening in the Eurozone is reduced by dim medium-term growth and inflation outlook. Given the strength of the US recovery, fiscal stimulus, and inflationary pressure, we think there is more to fear for US markets.

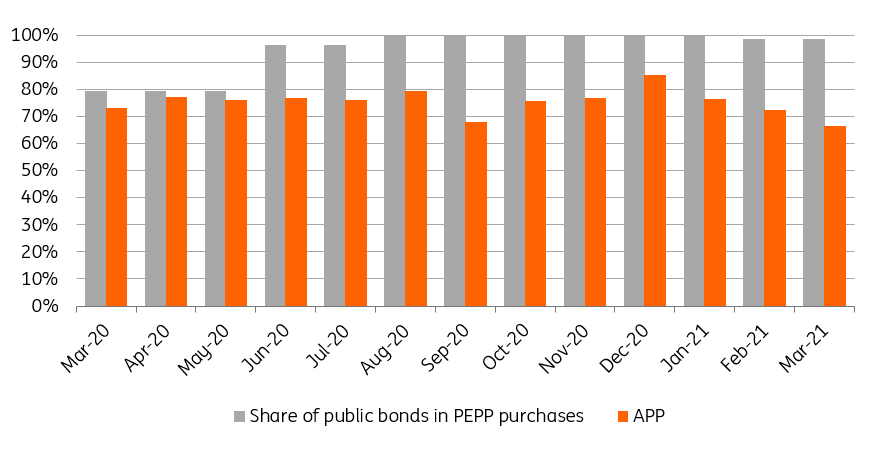

PEPP will be tapered first; this is mostly a problem for government bonds

Refinitiv, ING

Even if the path towards normalisation at the ECB is far from straightforward, the extent of its approximately €100bn purchases per month means slowing them down will have clear distorting effects on the markets it targets. In the case of PEPP, the programme most likely to see a reduction in the purchase run-rate as soon as next month, this means mostly government bonds. This provides a justification for the sharp underperformance of European government bonds relative to swaps, and for wider sovereign spreads. Corporate bond performance on the other hand has been resilient.

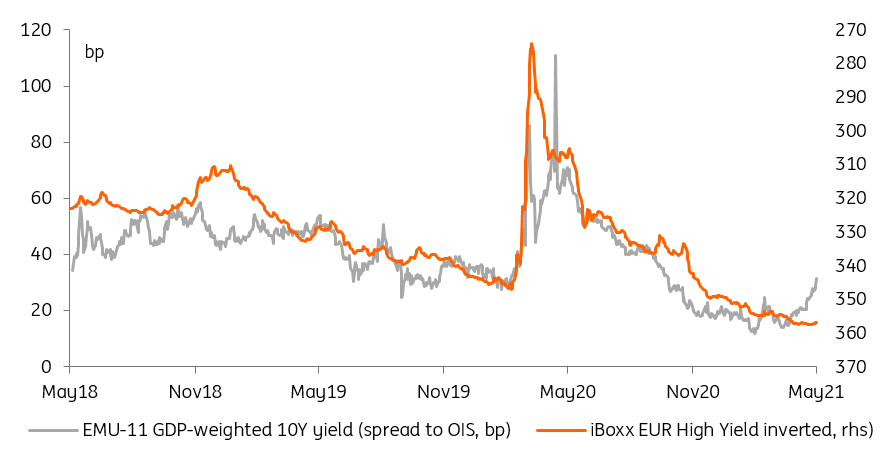

Corporate bonds have been immune to the tapering fear gripping govies

Refinitiv, ING

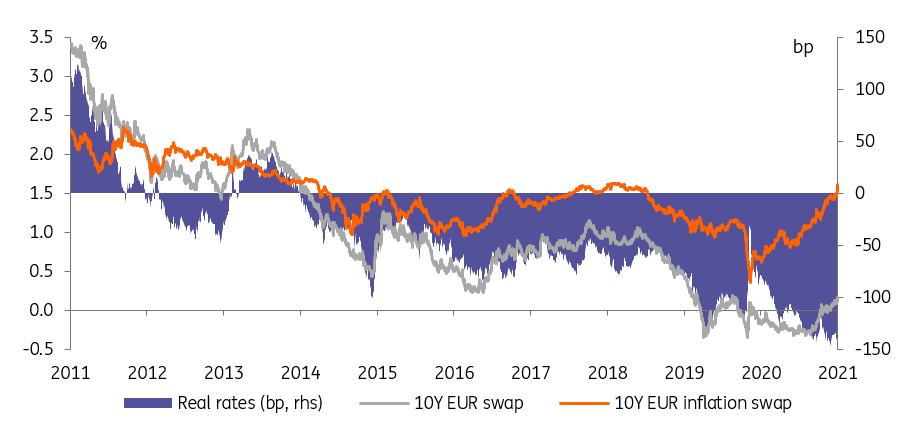

Fears justified, at least according to real rates

The question the ECB will have to answer next month is whether the current state of play: higher financing cost for sovereigns but not necessarily for corporations, is enough to continue purchases at an accelerated pace. One way to answer this question is to look at real rates, financing costs adjusted for inflation expectations. By that metric, financing conditions remain exceptionally easy. In other words: it seems like higher government bonds yields and swap rates actually failed to keep up with better economic prospects.

Higher government bonds yields and swap rates actually failed to keep up with better economic prospects

In theory, the minutes of the April ECB meeting could provide a useful yardstick as to how it assessed rate levels compared to the economics of the recovery at the time. In practice, we suspect the governing council avoided the subject like the plague. How else could President Christine Lagarde boast of a ‘peaceful’ meeting with no objection to faster purchases being voiced? To us, the battle lines were drawn when the decision was taken in March, and economic developments into the June 10th meeting should reinforce the hawk’s hand.

Real rates suggest ECB policy is at its most accomodative relative to inflaiton prospects

Refinitiv, ING

Today’s events and market view

There is no let-up in US economic releases today with retail sales, industrial production and consumer confidence. Each could face potential headwinds (eg, fall after the stimulus-induced jump in March for retail sales, chip shortages for industrial production) but together, they should confirm the US economy is in rude health. Even after this week’s inflation surprises, we would venture that economic data has taken a bit of a backseat in setting USD rates. One reason is that the recovery makes indicators extremely noisy. The other is that the Fed has been successful in communicating its patient mantra. This has provided cover for near-term investors to pocket the carry offered by bonds.

The ECB publishes the minutes (called accounts) of the April meeting today. We would be surprised if it gives much information about how it regarded financial conditions at the time and thus allowed the market to draw conclusions about the future pace of purchases. This being said, fewer direct references to the recovery and how it justifies higher rates could be taken by bonds as a confirmation of their tapering fear, and push EUR rates higher.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more