ECB Draghi's 'Whatever It Takes' Is Not Enough

It has been five years since ECB President Draghi defiantly stated that the “ECB is ready to do whatever it takes” to combat the then looming debt crisis in the eurozone. The crisis has long past, but the eurozone remains mired in slow growth; and, serious divisions regarding budget fights weaken leadership in Germany and France and the whole mess called Brexit.

It seems that “whatever it takes” has turned out to be not enough. Last week, the ECB lowered its 2019 forecast for gross domestic product growth in the eurozone by 0.1 percentage point to 1.9% and shaved its 2020 forecast by a similar amount to 1.7%. The announcement by the ECB to cut its economic forecast is the culmination of a whole set of risks now confronting the major European economics. In a rather stark admission, ECB President Mario Draghi stated that “It’s a climate of great uncertainty,” that is holding back better economic performance. He cited trade tensions, vulnerabilities in emerging markets and volatility in financial markets as major contributing factors to adjusting growth lower. What triggered the re-assessment of growth was the unexpected weak performance for the third quarter of 2018. Accordingly, the ECB confirmed it would keep its key interest rate unchanged through to the summer of 2019, at minus 0.4 per cent.

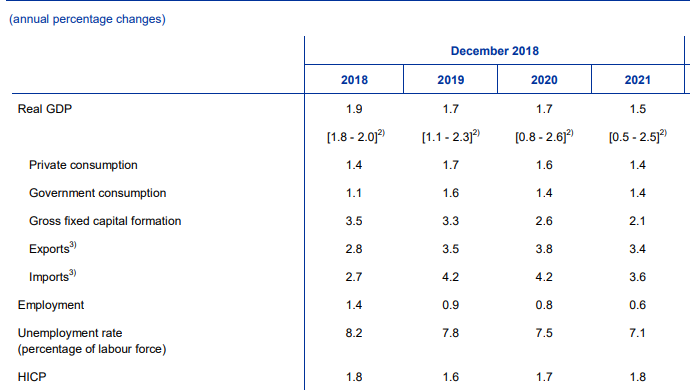

Figure 1 Eurozone GDP and Components

Source: December 2018 Eurosystem staff macroeconomic projections for the euro area

Overall, there are unmistakable signs that the area is facing slower growth and no inflationary pressures.An ECB staff forecast anticipates that growth will slow from 1.9 per cent in 2018 to 1.7 per cent in 2019 and eventually to 1.5 per cent in 2012. Business fixed investment will drop from 3.5 per cent in 2018 to 2.1 per cent by 2012. Finally, the rate of inflation (HICP) is expected to remain below the 2 per cent target used by the ECB. The ECB explains that decline in growth rates is tied to “labour supply shortages in some countries and somewhat less supportive financial conditions over the projection horizon”.

It is questionable why the ECB elected to end its bond-buying program (QE), given this rather sobering outlook. Begun in 2015, its QE program was aimed at reducing long-term borrowing costs, stimulating spending and investment and ultimately reversing the deflationary forces in effect in previous years. The decision to end the program was made this year and comes some years after the Federal Reserve and Bank of England wound downsize their own bond purchases. More to the point, ECB President Mario Draghi has gone on record saying that “in some parts of this period of time, QE has been the only driver of this recovery.” It seems as if the ECB is winding down the program , albeit with considerable reluctance.

Should growth weaken further, the ECB has very little, if any, room to stimulate growth. The bank rate rests at minus 0.4 per cent and going further into negative territory will be interpreted as an act of desperation, especially in comparison to the Fed’s stated objective of raising rates. Also, the EU rules regarding budget deficits prevent any country from adopting greater fiscal stimulation. Budget deficits are at their maximum of 3 per cent of GDP. Italy is challenging the EU authorities regarding its wish to expand its national deficit beyond the community rules.

Within the individual countries, there are developments that could send the Eurozone onto an even lower growth path. The recent political upheaval in France has already hit the retail sector at a crucial holiday period and threatens to weaken economic growth throughout the country. Italy continues to square off with the EU over budget issues and has generally been a laggard holding back growth in the region. Finally, for the first time since early 2015, German GDP growth turned negative at -0.2 per cent in the third quarter. In sum, Europe will not be a source of growth for the global economy, at a time when China and Japan are also slowing down, leaving only the United States to do the heavy lifting.