(Click on image to enlarge)

Front-end pricing talk but it’s a red herring

Much has been said and written about the next two ECB meetings’ rate hikes. The upshot is, as our colleagues highlight, the ECB still has a licence to hike, and a 50bp increase is pretty much set in stone this week. In all likelihood, guidance for a 50bp March hike will be repeated too but the March meeting will also feature a new set of forecasts that should heavily influence the ECB’s decision. As a result, markets will be tempted to rely more on their anticipation of how the ECB staff forecast will evolve at that meeting, rather than on president Christine Lagarde’s guidance.

As our economics team noted in their preview, "If everything else remains the same as it was in December, the ECB’s headline [March] inflation projections could easily be lowered by 0.3 to 0.5 percentage points for 2024 and 2025". Cut-off for the FX, rates, and energy market prices is a little under one month away but, as things stand, this would imply 2025 inflation at 1.8%, under the ECB’s 2% target. Worse, this would be premised on a curve that implies 80bp of cuts between the mid-2023 rate peak and end-2024.

To cut a long story short, we wouldn’t overstate the importance of the next two meetings for interest rates markets.

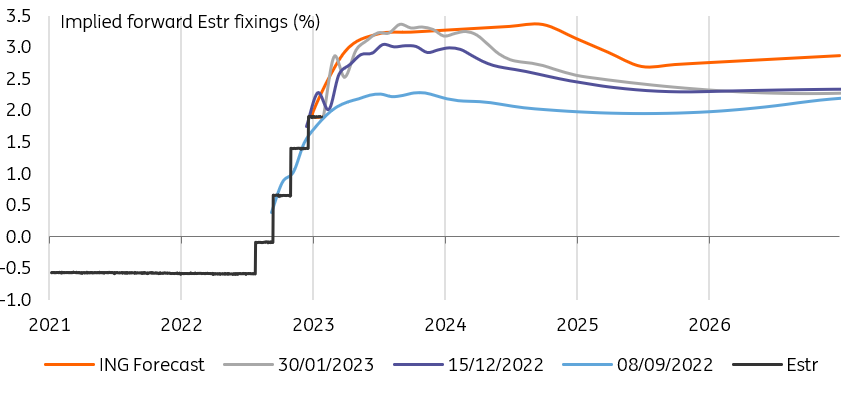

We now have more hawkish ECB expectations than the market

Source: Refinitiv, ING

Eyes on the prize, the belly’s where the battle really is

The curve is pricing a rapid decline in rates after they reach their peak in 2023. For a central bank expected to hike at least three more times, this is problematic. Lagarde is sure to be asked about this anomaly. If recent history is any guide, she’ll likely take that opportunity to guide market rates higher. We doubt she’ll manage to completely dis-invert the curve, however. The shape of the euro term structure cannot be seen entirely in isolation and some remnant of easing is likely to persist as long as the Fed is expected to cut more than 200bp by end-2024. But, at least, she should manage to delay cut expectations.

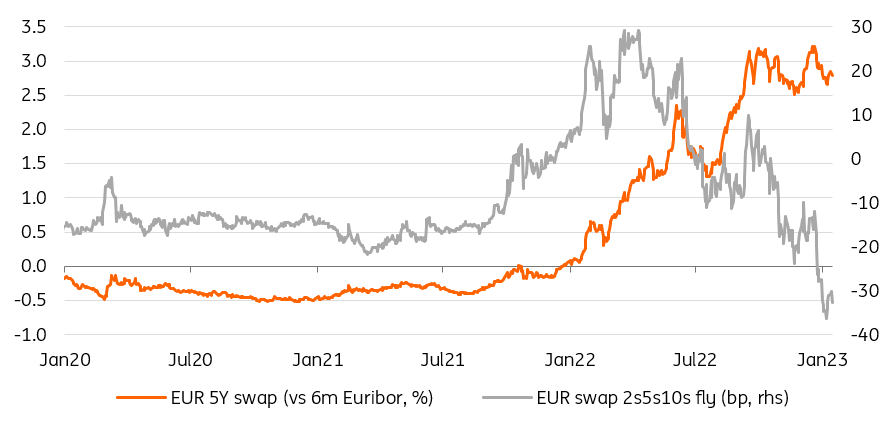

The part of the curve most likely to be affected is the 5Y point. We think hike expectations are correctly set for the next few meetings which imply that short-dated bonds and swaps, say up to 2Y, are also correctly priced. Longer tenors, on the other hand, depend on more structural factors such as where investors think the long-term interest rate equilibrium lies. This is not something the ECB will change at this meeting. This leaves the maturity in between, aptly called the belly of the curve, as the sector most at risk of a pushback against cut expectations.

What happens to the slope of the curve, for instance 2s10s, depends in greater parts on the tone of the ECB from one meeting to the next. We have a view (it will be hawkish) but given its recent unpredictability, we have a greater conviction on our outright (higher rates) and curvature (5Y rates to rise faster than other maturities) calls.

5Y rates are most at risk if the ECB pushes back against rate cut expectations

Source: Refinitiv, ING

'Detailed parameters' on quantitative tightening to come, but the market-moving information is already out

The ECB has promised “detailed parameters” for the reduction of its asset purchase programme portfolio. With laying out the headline volumes already at the last meeting, the most market-moving aspects are already known. What we could expect is details about whether the reduction will be proportionate across the different asset classes. Within the public sector specifically, how the ECB will maintain alignment with the capital key distribution across countries. We do not anticipate the ECB to diverge from previous targets here, though we might get information on how special situations will be dealt with. For instance when overall redemptions in a month are below the targeted reduction volumes.

Keeping in mind the focus the ECB and Isabel Schnabel in her recent speeches have put on “greening” the central bank’s portfolios, there is a chance that this also translates into more concrete action in the public sector portfolio. A rebalancing towards supranational debt with their larger share of green bonds would make sense, and it would not impact the capital key alignment. It would also address the rising prominence of the European Union as an issuer. We doubt though that such tweaks by themselves will impact the market's currently benign take on sovereign spreads. This time they are more likely to take their cues from the overall tilt of the ECB’s communication.

This isn’t a litmus test for the euro rally

While it’s undeniable that the ECB doubling down on its hawkish rhetoric has contributed to the strengthening of the euro since December, we don’t see this week’s policy meeting as a litmus test for the sustainability of the euro rally.

The reasons are two-fold. First, EUR/USD may well return to being predominantly a dollar story this week. A Fed approaching peak rate and facing a worsening economic outlook has more room to surprise on the hawkish side, and we think it could offer a breather to the dollar. In contrast, as discussed above, we would not overstate the importance of the next two ECB meetings for rates.

This leads us to the second reason: the ECB’s communication hiccups have likely eroded the market's trust in Lagarde’s guidance. Only a few hours after the December meeting, the news that many members had preferred 75bp was leaked. And if ECB members aligned behind the 50bp guidance in recent weeks, a probably more debated 50bp move in March may well cause sparse communication again after the February meeting. This – in our view – may lead markets to be more forward-looking than what Lagarde will wish them to be.

Ultimately, data may remain a larger driver than Lagarde’s guidance for the euro. If gas prices stay capped and economic surveys keep pointing up, a correction in EUR/USD after a hawkish Fed should not last long. We expect EUR/USD to trade around 1.07-1.10 for most of February. Another big break higher may need to wait for an official pivot by the Fed: we see this materialising in the second quarter, where we forecast a move to 1.15.

More By This Author:

Eurozone Sentiment Continues To Improve

Drastic Shift In Natural Gas Outlook

FX Daily: Stress Testing The Consensus View

Comments

Log in or sign up to join the conversation.