Don’t Ignore Currency Exposure When Investing Globally

Managing Exposures in 2021

In 2021, U.S. investors are likely to find improved return opportunities in overseas markets. This increased investment offshore creates currency exposure which is often an implicit bet rather than an intentional investment decision. In this text, we explore how currency exposures can be managed to lower risk or enhance return.

When U.S. investors make allocations to international assets, they are inevitably exposed to exchange rate fluctuations. For example, a US investor who buys an international developed-market ex US equity index implicitly has a long position in a basket of currencies consisting of roughly 30% euro, 23% Japanese yen, 13% pound sterling, 9% Canadian dollar, and other currencies.¹

That currency exposure can have a large impact on realized returns to the US investor. Between the start of 2017 and the end of March 2020 - a period of U.S. dollar strength - the currency-hedged MSCI ex USA index outperformed the un-hedged version by 11%. Since then, roles have reversed and the un-hedged index did better by 8.5%.²

Leaving foreign currency exposures un-hedged could be an implicit bet on continued U.S. dollar depreciation. However, for many investors the foreign currency exposure is not an investment decision they expect to earn returns from, but instead a mere by-product of the equity position. In that case, the unintended risk could be reduced or molded into rewarded risk.

Currency Hedging for Risk Management

Currency hedging using forward exchange contracts is a good way of reducing the unrewarded risk from currency. By selling an appropriate amount of foreign currencies forward, hedging creates positions that move in the opposite direction to the currency exposures in the underlying portfolio. In a static currency hedging program, a constant percentage of the foreign currency exposure is hedged, for example, 50% or 100%.

In our view, static currency hedging (on average) reduces risk without giving up expected return when looking at an appropriately long period. For that reason, some academics have called currency hedging a "free lunch."³

This effect is very pronounced for international bonds, but is also visible for international equities. Between 1997 and today, full currency hedging would have reduced the volatility of global bonds ex-US by roughly two thirds and that of developed-market equities ex-US by about 14% compared to the un-hedged investment.⁴

Another way of quantifying the risk reduction benefit from currency hedging is to look at drawdowns. Again, the figures for the global bond ex-US portfolio look compelling. Full currency-hedging would have reduced the maximum drawdown by $15 million on a $100 million portfolio compared to no currency hedging. For the developed-market equity ex-US portfolio, the decrease in maximum drawdown is about $7 million on a $100 million portfolio.

While these historical outcomes are specific to the sample period studied, we believe that the risk reduction conclusion will directionally hold in the future. This is because the U.S. dollar is a so-called safe-haven currency which goes up when risky assets, such as equities, slump. Currency hedging is risk-reducing for the U.S. investor because it increases exposure to a safe-haven asset.

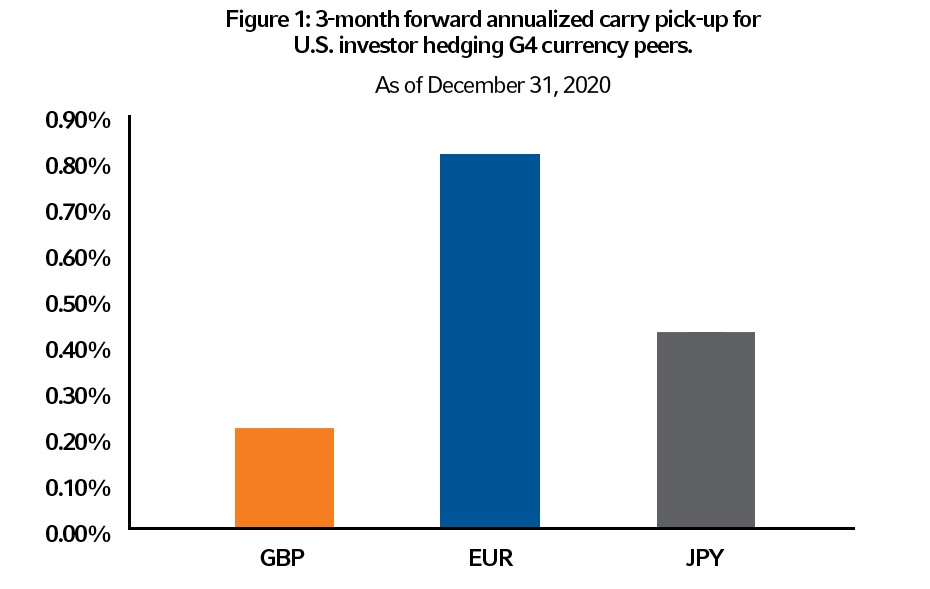

Lastly, U.S. investors can continue to pick up a small positive yield from hedging many other developed currencies given the relative level of interest rates (see Figure 1).

Source: Bloomberg

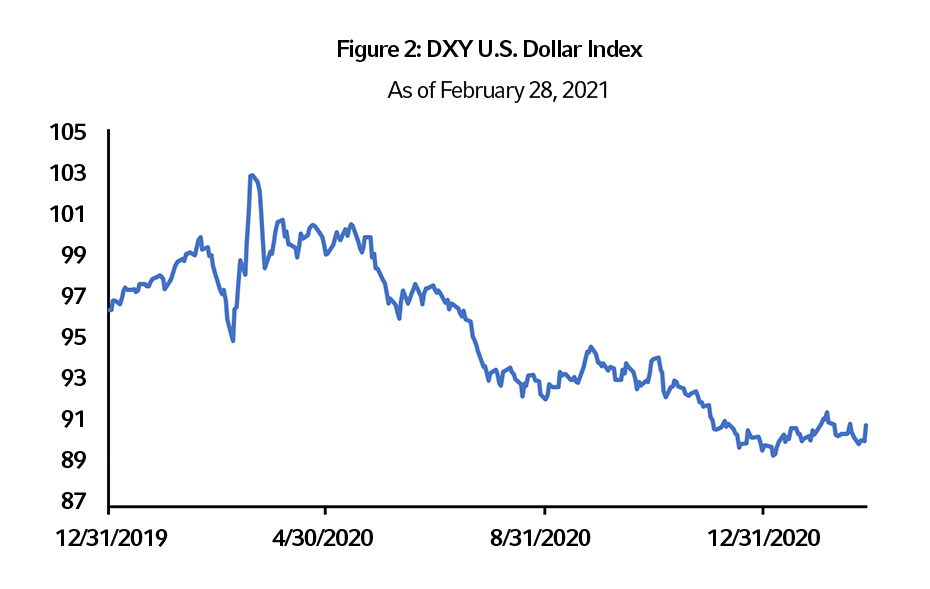

Is now the right time? Over recent months, broad market consensus has been congregating around a secular U.S. dollar bear market view for the coming years. This is supported by the decline in the U.S. dollar of about 11% (as measured by the DXY dollar index) since its peak at the time when the COVID-19 pandemic erupted (see Figure 2).

Source: Bloomberg

The consensus view on dollar weakness is predicated on a continued re-opening and reflation in the world economy, a view we share. But we know from experience that the consensus view can be wrong. A notable concern with timing is that, during the current recession episode, we have not experienced the insolvency phase synonymous with the end of economic cycles and recessions.

This phase has been kicked down the road thanks to the powerful combination of monetary and fiscal policy, not to mention legislative forbearance measures. If there is a wave of insolvencies and other hidden structural damage coming to the fore, it could lift the U.S. dollar as a typical safe-haven currency.

Whether the dollar bear market continues or not, investors can lessen the timing risk by phasing in their currency hedging program either through a calendar-based approach, and/or valuation triggers that raise the currency hedge ratio as the U.S. dollar falls to more attractive levels. Doing it this way may allow investors to capture some additional return if and when the dollar trend turns around.

Dynamic Hedging and Absolute Return Currency

Finding the 'optimal' hedge ratio and the right time to initiate that static hedge is difficult. A different approach is to allow the currency hedge ratio to always be flexible over time with the aim of generating excess returns over a passive hedge. Hedge ratios can be adjusted for currency valuations, interest rates, and other factors that drive currency returns.

This dynamic currency hedging approach can turn the incidental currency risk from international assets into a return source. Investors could improve the risk-return outcomes of their portfolios, relative to implementing a static hedging policy or not hedging at all.

Alternatively, some investors also employ absolute return currency strategies where long-short foreign exchange positions are agnostic of the currency exposures in their underlying portfolios. We believe that commonly used factors such as Carry, Value, and Trend can capture returns in foreign exchange markets.

Such strategies are more attractive in the current environment where policy interest rates are likely stuck around zero and macroeconomic divergences can’t easily be reflected in bond markets. We find that Japanese investors, who are used to very low interest rates, have shown an interest in absolute return currency for some years. Amid a similar monetary policy environment, U.S. investors could also turn their attention there.

Bottom Line

When investors start thinking about post-pandemic asset allocations, consideration should be given to the management of currency exposures. As the U.S. dollar has declined in recent months and a further fall is the consensus view, leaving foreign currency exposure from international stock and bond investments un-hedged may be a psychologically comfortable stance.

However, the weak dollar forecast may be challenged if risk aversion takes hold again or if U.S. interest rates unexpectedly rise. We believe now is a good time for investors to assess their options in currency management, be that phasing in a static hedge program, dynamic currency hedging, or absolute return currency. The only course of action we do not believe is appropriate is to ignore currency exposure.

¹ These are the currency weights in the MSCI ex USA index. Source: MSCI, as of 29 January 2021.

² Source: MSCI, Refinitiv Datastream, as of January 29, 2021.

³ ...

more