Copper Demand: China Has Been Doing The Heavy Lifting

Copper prices: bullish arguments

Copper has been stuck in a range-bound market over the past two weeks as there are multiple counterbalancing forces. On the bullish side, the supportive factors in the macro backdrop are still in place, including the Fed’s supportive stance and the dollar index continuing to be under pressure.

Meanwhile, governments’ stimulus packages are expected to kick-start their economies. Recent economic indicators are still validating the strength of China's economic recovery – rather than contradicting it. On the micro-level, the London Metal Exchange on warrant inventories continues to grind lower, and now both the LME and Shanghai Futures Exchange markets are in backwardation with tightened spreads in the front of the curve to fence off nearby bears.

Copper price: bearish arguments

On the bearish side, elevated political tensions see no signs of easing, but only escalating, along with headwinds for riskier assets. Mining disruptions (both virus-related and strikes) risks are starting to recede ahead as long as there is no major reversal in virus cases, and, in fact, some have managed to return to work.

China demand, which has been doing all of the heavy-lifting so far this year, is expected to have entered its seasonal lull and pent-up demand is set to dry up. Support from cathode displacement to scrap has mostly faded. Meanwhile, a resurgence of COVID-19 cases has been seen at multiple locations around the world, which casts a shadow over the economic recovery path.

What does this mean for short-term prices? After an astonishing rally seen in 2Q20, momentum seems to have been lost in the near term, absent a strong dominant theme. Unless a factor comes to the forefront, copper is likely to continue trading in a range-bound pattern.

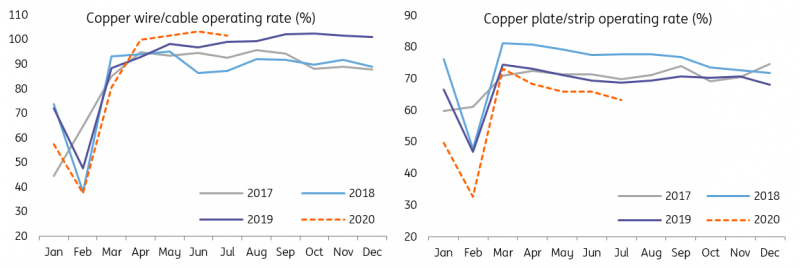

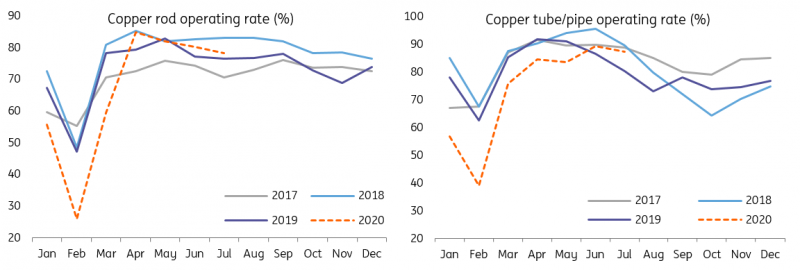

Average operating rates at semi-fabricated products manufacturers are declining

SMM, ING

SMM, ING

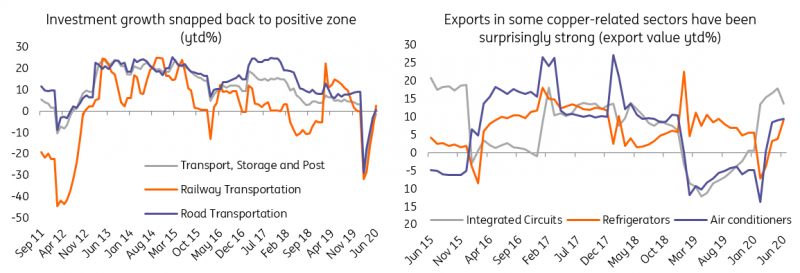

How’s the demand from China?

Starting from 2Q20, a strong investment-led demand coupled with surprisingly strong exports at some copper-intensive sectors (machinery, home appliances, etc) saw demand growth snap back sharply. Meanwhile, the domestic end-use sectors had seen a substantial recovery (car sales, retail sales such as air conditioners etc), although they have not yet come back to the level from the same period of the prior year.

These had sparked to a round of restocking by consumers and stockpiling was also heard among other players in the market, including the State Reserve Bureau as reports suggested. Although exports strength ahead remains uncertain, we expect infrastructure construction to continue to provide support to demand for the remainder of this year. Hence, China is expected to continue doing the heavy lifting for global copper demand.

End-use indicators validates a strong demand growth from China

China Customs, NBS, ING

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more