China's Rapidly Expanding Credit Affects Global Markets

We are seeing again how rapidly expanding credit in China is spilling over into the global market. In reaction to its economy being slammed by COVID-19, China, like many countries, has unleashed several massive stimulus programs to start things moving.

Unfortunately for the Chinese citizens, they have also been dealing with other issues putting their system under stress. Not only is the trade war and a high level of political stress putting China to the test, but it is in the midst of the worst flooding in decades - and this is also adding to the pressure.

Since the outbreak of the pandemic, Chinese authorities have issued 4.75 trillion yuan ($683 billion) in local and national debt, with most of that earmarked for infrastructure projects to boost construction. China is not exactly transparent and this is making it difficult to know exactly what is happening. This is also true when it comes to imports, which are sometimes stored away rather than used.

Speculation and projections of future use all play into this. Whether we are talking about grain prices, oil, or metal, China is a bigger user of commodities and the demand flowing from China affects prices. Factor this as well as the notion that China has a history of projecting a positive narrative of economic growth, and the spillover becomes clear.

An example of this can be seen as iron ore prices hit a six and a half year high on Thursday, September 3, as the Chinese construction and manufacturing sector claims to be experiencing levels of activity not seen for almost a decade. Fastmarkets MB reported that benchmark 62% Fe fines imported into Northern China were changing hands for $129.92 a ton on Tuesday, up 2.1% on the day.

That would be the highest level for the steel-making raw material since mid-January 2014, and put gains for 2020 to over 40%. China is responsible for more than half the world’s steel output and 70% of seaborne iron ore imports. This makes such numbers a key gauge of economic activity in the country.

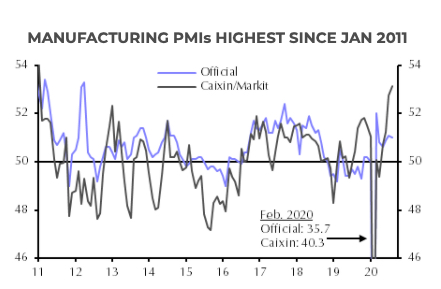

Source: Capital Economics (click to enlarge)

If accurate, the numbers released this week indicate a rapid expansion of China's manufacturing and construction sector in August. The question remains as to whether this is a dead cat bounce from the diabolical COVID-19 pandemic, or a recovery with real legs.

The chart above shows the Caixin manufacturing PMI index rose from 52.8 in July to 53.1 in August, well above analysts’ expectations. The official PMIs released by the Chinese government showed a slight drop in activity, but the Caixin index is often seen as a more reliable gauge of activity.

The export orders component of the manufacturing PMI rose above 50 for the first time this year on the back of recovering foreign demand. This could indicate that foreign demand is now beginning to increase again.

It could be argued that China’s factories are humming once again and spending on infrastructure is soaring, however, as a skeptic, I view much of this as temporary. It could be that many stores across the world simply need to refill their shelves after months of economies being locked-down. If this is true, prices and demand may soon begin to fade.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in ...

more