Lockdowns have created problems for banks in China as they have become more risk-averse. China's central bank has promised to help but it lacks a solution. We believe that asset management companies play a role in boosting overall credit. But there is no perfect solution when the uncertainty of long lockdowns is high.

During lockdowns, banks become more risk averse

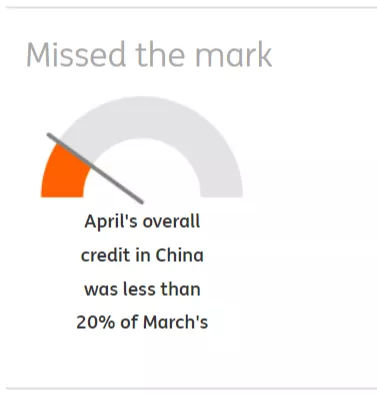

Very weak loan growth

New yuan loans grew only CNY645.4bn in April after a CNY3130bn increase in March. The market consensus was CNY2200bn. April is typically a month of lower loan growth than March, but this April's loan growth is just too weak. This matches the very soft growth in aggregate finance, which grew only CNY910.2bn in April compared to CNY4650bn in March.

Banks can blame lockdowns

The main reason for such small credit growth is because of Covid lockdowns that have created difficulties for getting new loans. During lockdowns, there are many individuals and companies who suffer from loss of wages and loss of business, so, therefore, there should be an increase in demand for loans. If the supply of loans was steady, we should have seen a jump in new loans in April.

But that was not the case because banks in mainland China are more credit-sensitive nowadays. During lockdowns, banks tend to be more risk-averse. They have been told to keep past-due loans on their books. Under these circumstances, banks have become unwilling to create new loans, as that would mean taking on more risk by getting new loans and then waiting for them to become past due if lockdowns continue.

This is bad for the government as it would like to see banks giving a helping hand to the economy. But from a risk management perspective, banks are protecting their capital ratios, which isn't a bad idea for the whole financial system in China.

PBoC is undecided: to cut or not to cut

The People's Bank of China (PBoC) is struggling to decide on whether to lower interest rates by cutting the policy rate (Medium Lending Facility) and/or the required reserve ratio (RRR). There are mixed messages from the government and the central bank. It is difficult to decide because cutting interest rates is not a direct way to help an economy that has been damaged by lockdowns. Fiscal measures would be more effective, and there are quite a few of them for small and medium-sized enterprises and individuals.

There may be new tools from the PBoC, as it has promised, which will hopefully arrive soon.

We believe a way out is for banks to divest some loans to asset management companies, allowing banks more room to increase lending. But the asset management companies have to take the weak credit from banks. Then there is the issue of how much weak credit the asset management companies can hold without raising too much capital. There is no easy solution for easing monetary policy when the uncertainties of long lockdowns remain high.

Comments

Log in or sign up to join the conversation.