Brexit And The Bank Of England: What To Expect This Week

UK-EU trade talk optimism is rising, although there's widespread skepticism that a deal will come before the Bank of England announces its decision this Thursday. We don't expect fresh monetary stimulus, but we could see signals from the Bank that they are prepared to ramp up various schemes to smooth over any Brexit-induced market volatility.

Bank of England, in the City of London

Brexit optimism is tentatively rising once more

Despite a deafening amount of Brexit-related noise over the weekend, we start the week with a feeling that things may finally be moving in the right direction.

Of course, the cynic might argue that we've been in this position several times over the past month or so, only for optimistic headlines to be subsequently displaced by warnings of ’significant differences’.

The recent deadlock has centered around what happens if either side wants to tighten up things like environmental rules, labor standards, and state aid controls in the future. Prime Minister Boris Johnson last week publicly pushed back on the idea that a) the EU could unilaterally decide to tighten its standards in these areas in the future and b) automatically impose tariffs if the UK failed to follow suit.

According to The Sun, however, both aspects have been watered down. On the former, negotiators are looking to define what level of divergence can be labeled as ‘unfair’, and how it could be tested. On the latter, there is talk of an independent arbitration system to resolve disputes, removing the unilateral right of either side to impose sanctions automatically.

There will inevitably be some debate on who’s blinked - whether this shows flexibility from the EU, or whether it reflects a big shift in principle from the UK. Perhaps the reality is a bit of both - and undoubtedly there may be an element of choreography embedded in all of this to help PM Johnson sell a final deal domestically.

A deal remains more likely than not, but the timing is unclear

Whichever way you cut it, there is clearly a ‘landing zone’ in sight for a deal to be done.

Nothing's guaranteed though, and we’d reiterate that this is ultimately a ‘big picture’ decision for PM Johnson. It's not just about the shape of the final compromise but encompasses a range of contextual political factors - polling, the Scottish Independence factor, the relationship with President-elect Biden. It will also come down to how the deal fits into the government’s view of sovereignty - a key pillar of the Brexit debate.

But while a deal still feels (narrowly) more likely than not, the timing remains up in the air. Politically speaking, there’s not much to stop talks running very close to the New Year’s deadline.

That would make ratification trickier, but not impossible. In London, the deal could be pushed through Parliament at speed, perhaps only requiring one day. Across the Channel, the European Parliament (EP) needs time to scrutinize and vote on the agreement - although there is a less-favored scenario whereby the European Council agrees to provisionally apply the deal on 1 January, and seek approval from the EP a few days later.

Expect signals rather than action from the Bank of England this week

This makes life all-the-more difficult for the Bank of England, which meets this week for the final time in 2020. The combination of likely disruption at the start of 2021 (even with a trade deal in place), combined with the growing prospect of tight Covid-19 restrictions running well into the first quarter, mean the pressure on the Bank to keep offering stimulus is unlikely to dissipate imminently.

That said, we doubt we’ll get any fresh action this Thursday - and instead we’re likely to get a series of signals of what the Bank could do if conditions deteriorate around New Year.

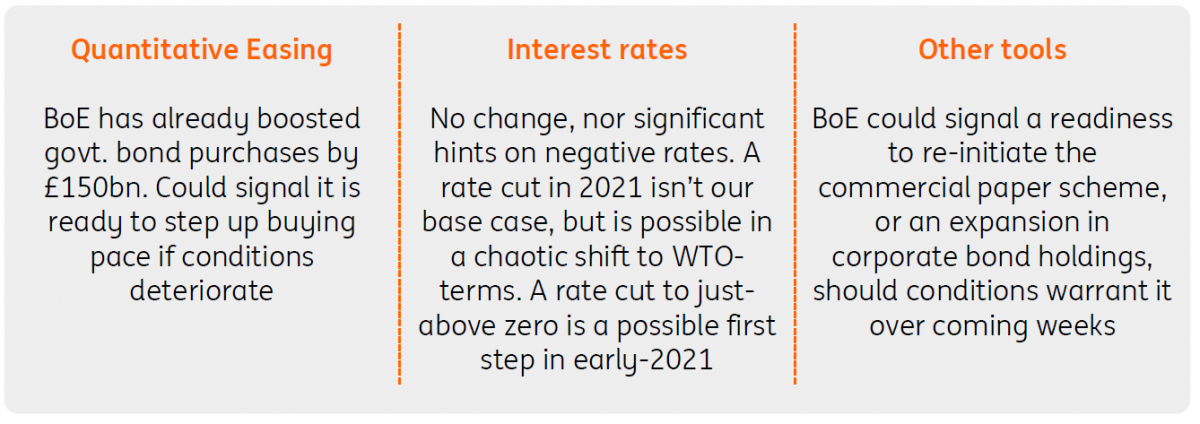

The Bank of England has already expanded the scope of its government bond purchase program by £150bn in November, enabling it to continue purchases through 2021. The BoE may well indicate that it could increase the pace of purchases again if financial conditions warrant it, although, for the time being, sterling markets remain relatively calm.

10-year yields are relatively stable, while the degree of risk premium in EUR/GBP is now roughly 1% according to our FX team’s calculations, which is noticeably less than in previous moments of Brexit drama. It's a similar story for corporate financing conditions - previously a key worry among central bankers back in March.

However again, it's not impossible that the Bank signals openness to re-deploy its commercial paper scheme, or to top-up the corporate bond-buying program, should conditions warrant it over coming weeks.

Our expectations for this week's Bank of England meeting

(Click on image to enlarge)

Source: ING

Negative rates not our base case in 2021

As always though, markets will be most interested in further commentary on negative rates - although they might be disappointed. Governor Andrew Bailey recently noted the Bank's impact analysis is ongoing, following a survey of commercial banks. More importantly, there still appears to be a lack of consensus on the monetary policy committee on whether the policy would be effective. The likes of Silvana Tenreyro and Michael Saunders, both external committee members, have signaled their support for negative rates, but others, including Chief Economist Andy Haldane, appear less convinced.

In our view, we think the Bank of England will most likely steer away from negative rates in 2021, although a chaotic switch to WTO trade terms in January would increase the chances. As a first step, the Bank might be inclined to lower rates even closer to zero from their present 0.1%.

If the Bank does ultimately make a foray into sub-zero rates next year, we suspect policymakers would not move into negative territory as deeply as other global central banks have done. We also think it would be considered an emergency move - one that may well be fairly swiftly reversed as the recovery builds momentum.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more