Thursday, August 26, 2021 7:30 AM EST

Today's Bank of Korea (BoK) decision to hike rates by 25bp came against the backdrop of a market completely split (actually fractionally leaning towards no change) as rapidly growing household debt was weighed against a worrying increase in COVID-19 infections. The BoK chose to focus on debt rather than disease in the end.

Pexels

Rates rise, can they do more before year-end? Probably...

The Bank of Korea decided after all to hike rates by 0.25% to 0.75%, making them the first mover in Asia of the countries we cover, and clearly not daunted by the earlier decision by the RBNZ to leave rates on hold due to rising COVID cases.

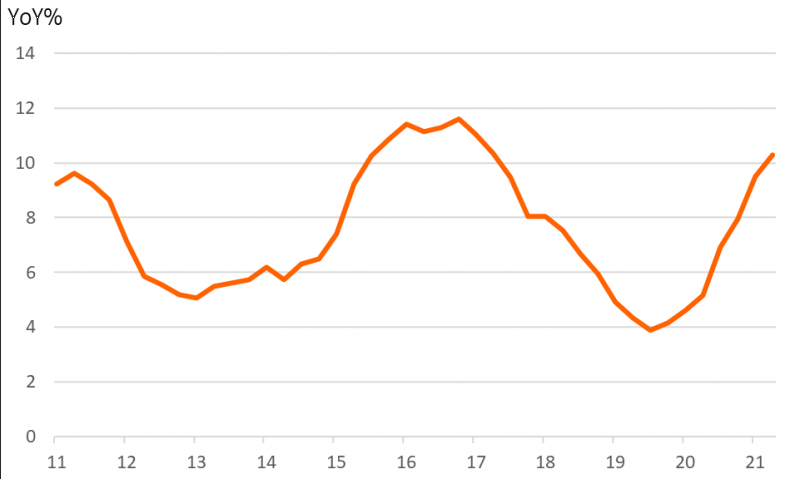

One thing that may have tipped the balance in this decision was the release of more household debt data earlier in the week. The rise in household debt has been a source of government and BoK concern for a considerable time now, but COVID has prevented any countermeasures to offset this. Clearly, and despite the increase in daily COVID cases in Korea, which is hovering around 2000 again, the BoK felt that the time had come to act.

Household debt growth YoY%

Source: CEIC

Debt is the flip side of a red-hot housing market

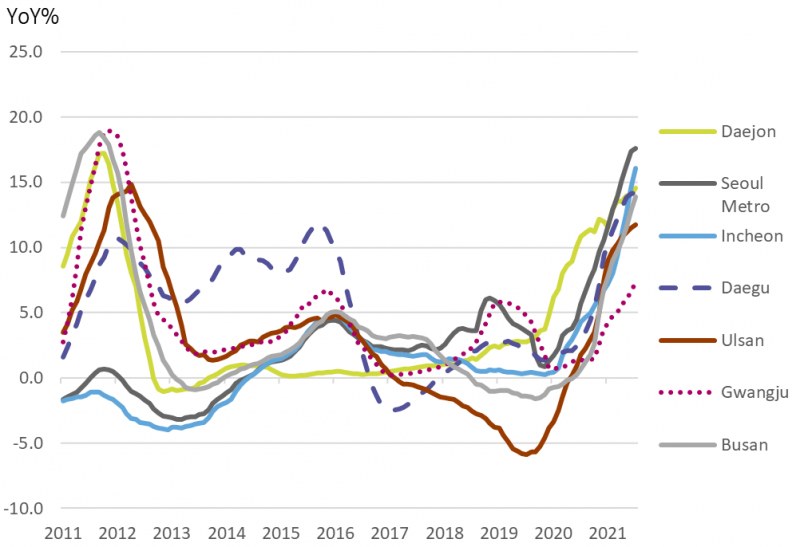

The flip-side of the rise in household debt is the housing market, where low rates have not been any barrier to rapidly rising prices across the country, with the national rate not far off 20%YoY. If there is ever a time when you can say that an asset is growing "too fast", this would be a good contender. The BoK will be attempting to soften house price growth, without kicking the legs from under the market. That's never an easy balancing act to pull off.

Residential property price increases

Source: CEIC

Where's the peak?

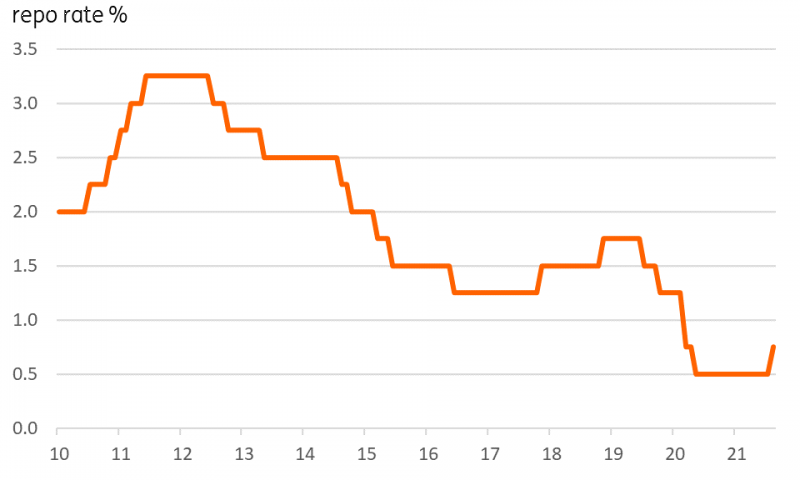

That takes us on neatly to the next question which is, "where do rates peak?". This is trickier, but the first thing to say is "lower than the last cycle", and that is a direct read across from the debt figures. With a higher household debt-to-income ratio, each rate hike will exact a greater squeeze on discretionary spending than in the cycle before, slowing credit growth to a more manageable rate earlier than in previous cycles.

The previous peak in policy rates was a mini-cycle in 2019, when rates got as high as 1.75%. I'd suggest that puts the peak in this cycle at no more than 1.5%, though it could reach it by the end of 2022 at this rate.

7-day repo rate

Source: CEIC

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on the Financial Conduct Authority’s website.. ING Bank N.V., London branch is registered in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.

less

How did you like this article? Let us know so we can better customize your reading experience.