Bank Of England: Four Things To Watch At The August Meeting

The recent rise in Covid-19 uncertainty means we're unlikely to see a hawkish turn from the Bank of England on Thursday. We expect policymakers to avoid offering any new hints on when the first rate hike may come, and we also doubt we'll get the early end to QE that some BoE hawks have recently proposed.

Bank Of England, London

In short: Don't expect a hawkish shift at the August meeting

We expect the Bank of England to strike a cautiously optimistic note on Thursday (5 August) – though crucially we’re unlikely to get any fresh hints on the possible timing of future hikes. Nor are we likely to see an early end to the Bank’s QE program – something BoE hawk Michael Saunders has recently advocated.

There is however an outside chance that we hear more about the Bank's future balance sheet reduction plans - which is likely to happen at a much earlier point in the future tightening cycle than policymakers had previously signaled. We expect the first rate hike in early 2023.

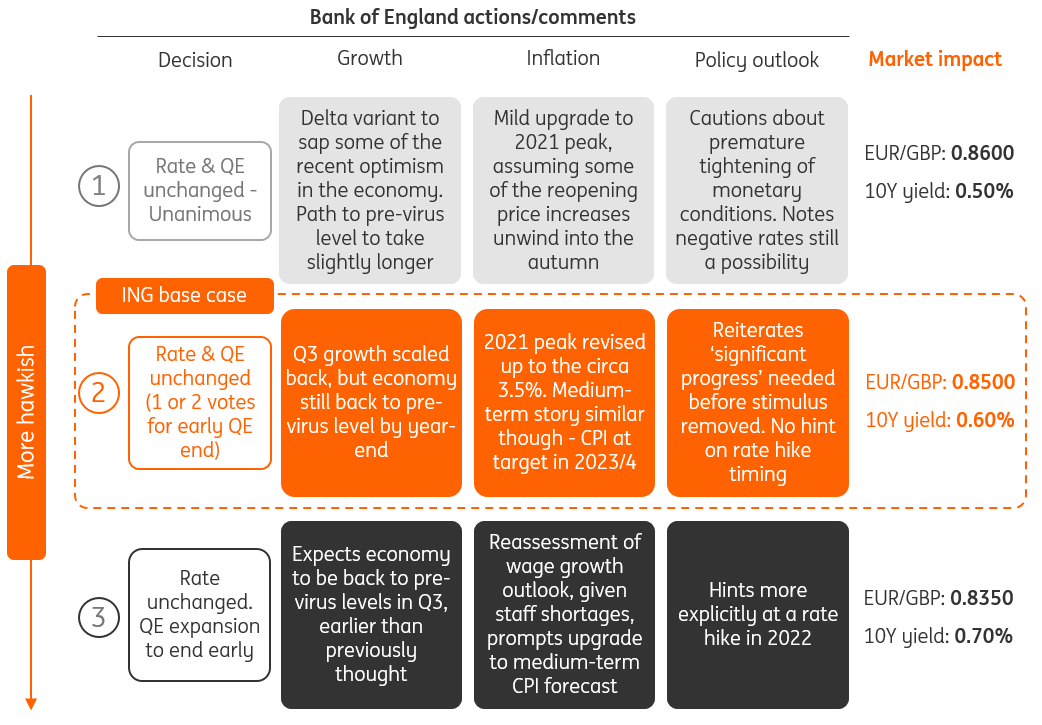

Three scenarios for the August meeting

(Click on image to enlarge)

Source: ING Forecasts courtesy of ING's Rates and FX Strategy teams

1. Expect some fairly upbeat forecasts

The Bank of England will unveil its new quarterly forecasts on Thursday - and on paper the story is still likely to be fairly upbeat.

Policymakers are likely to raise the inflation forecast quite noticeably for later this year. Reopening-related price spikes in various consumer services are combining with lingering supply chain disruption and energy base effects to drive a faster inflation rate than the Bank had penciled in back in May. We now expect CPI to peak around 3.5% later this year, compared to 2.5% as the Bank was forecasting back in May.

Unemployment has also been a bit better than feared, and it’s possible that the Bank once again lowers its estimate for the peak in the jobless rate later this year (linked of course to the phasing out of wage support). The BoE had previously penciled in a peak of 5.8% - around a one percentage point spike. The recent run of jobs data has certainly been fairly solid, though we’d caution that the number of people on the furlough scheme has not fallen as quickly as the wider recovery might have implied. That suggests a spike in redundancies is still likely in the autumn.

We also don’t expect any wholesale changes to the medium-term outlook for growth – and we’d expect the Bank to reiterate its forecast that the size of the economy will reach pre-virus levels in the fourth quarter.

2. We don't expect any further hints about future rate hikes

Despite that upbeat view, there are three reasons why we don’t expect any real hawkish shift on Thursday.

- Firstly – and most obviously – the Delta variant has clouded the near-term outlook. We’d expect the Bank to pare back its forecast for third-quarter growth from 3.8% to something more like 1.5-2%. Ultimately this is (hopefully) going to be a temporary story, but the short-term disruption has effectively pressed pause on the recovery and may have tempered some of the consumer optimism that had emerged through the spring. If nothing else, it’s a reminder that the recovery is unlikely to be smooth.

- Secondly, while markets have scaled back rate hike expectations in the longer term, the bit that’s most relevant for the Bank of England is what’s priced in two-three years' time. And on that score, investors are still pricing in a modest amount of tightening.

We suspect policymakers are fairly comfortable with that for now. We, therefore, expect the Bank to simply reiterate its recent line that it requires ‘significant progress’ before looking at stimulus removal, and avoid saying anything more concrete than that.

- Finally, the medium-term inflation story looks much the same as it did before. Despite recent staff shortages, we aren't convinced we're about to enter a period of above-target wage growth. And that suggests the BoE's inflation forecast for two to three years' time is likely to be roughly at target - and it's this that is ultimately relevant for policymaking today, rather than what will happen over the next six to twelve months.

Markets are pricing some modest tightening over the next three years

Source: Refinitiv, ING

3. No early QE end - but how about some hints on balance sheet reduction?

For those reasons, we think it’s also pretty unlikely that the Bank will scale back its QE program early. The BoE is on track to finish expanding its balance sheet at the end of the year, though outgoing Chief Economist Andy Haldane and external MPC member Michael Saunders have recently proposed wrapping things up early. In reality it won’t make much difference to the economy either way, though an early end does risk setting a precedent for future QE packages. The announcement of a new bond-buying package in the future may be less potent if investors were to factor in the possibility of the scheme being wound up early.

The more interesting question perhaps is whether we hear anything new on the topic of balance sheet reduction – or reverse QE/quantitative tightening as it’s otherwise known. This is uncharted territory for the Bank, which, unlike the Fed, did not shrink its pool of government bond holdings in the post-financial crisis years.

That’s mainly because Bank rate never came close to 1.5%, which was the threshold the BoE has long signaled to be when balance sheet reduction could occur. But under Governor Andrew Bailey, a future tightening cycle is likely to be accompanied by some reduction in the amount of gilts the BoE holds. The motivation is to provide more space to be ‘bold’ in a future round of QE.

One ‘passive’ approach to this could see the Bank of England allow maturing bonds to roll off the balance sheet without reinvesting – perhaps by setting an annual target. We discussed this in more detail back in May.

The jury’s out on whether we’ll hear anything more at this meeting, though policymakers have said they are in the process of reviewing their balance sheet guidance. At this stage we’re unlikely to get much more than a signal that the previous 1.5% Bank rate threshold will be lowered. Further details are likely to be unveiled very slowly over the next year or so, given this is new ground for the Bank.

4. Rates: Highly skeptical

Sterling interest rate markets are going into this BoE meeting fearing a repeat of the Federal Reserve's hawkish shift in June. Back then, the FOMC signaled an earlier start to its tightening cycle than previously anticipated, at a time of growing doubts about the strength of the recovery. We think these fears are misplaced, yet this is the scenario that the GBP swap curve is pricing with the greatest degree of probability.

Following the June Fed meeting, yield curves globally went on to price in a dismal outlook for the economy, an outcome supposedly precipitated by the Fed’s newfound hawkishness. We think this narrative has its limitations but the mindset prevailing in rates market is undeniably gloomy. This means sterling rates will not take kindly to another barrage of hawk-talk from the BoE next week.

The chorus of hawkish comments has prevented sterling rates from participating in the subsequent stabilization seen in other markets. This is visible in the continued flattening of the GBP 5s30s slope over the past weeks at a time the EUR and USD curves regained their composure. As it stands, we think the slope is already in policy error territory. As we think the BoE collectively will adopt a more cautious tone, the bar for some re-steepening is low.

A confirmation of the tentative decline in Covid-19 cases in the UK would cement Gilts’ underperformance relative to Bunds and Treasuries. It would also light a fire under the long-end. Remember that as BoE tightening looms, Bailey has flagged that balance sheet reduction could occur in parallel to rate hikes. This means a decompression of GBP rates is a real possibility over the coming months.

The continued flattening of the GBP curve reflects hawkish fears

Source: Refinitiv, ING

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more