Photo by Michelle Spollen on Unsplash

The Bank of Canada is widely expected to cut the overnight rate for a third consecutive meeting as slowing inflation and rising unemployment incentivize the central bank to get policy to a more neutral level quickly. We look for rates to fall to 3% by the end of second quarter 2025.

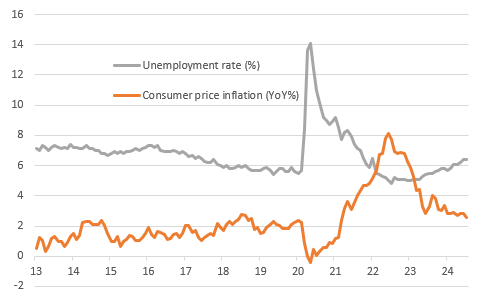

Lower inflation and rising unemployment justify interest rate cuts

The BoC initiated the current easing cycle at the 5 June meeting on the basis that "recent data has increased our confidence that inflation will continue to move towards the 2% target". This was followed up by a second cut on 24 July, justified by data showing “broad price pressures continuing to ease” with “ongoing excess supply lowering inflationary pressures”.

Since that meeting business survey responses have cooled further, employment has fallen for the second month in a row and inflation has slowed to 2.5% at the headline level, comfortably within the BoC’s 1-3% target range. Since unemployment has risen 1.6 percentage points since the July 2022 low, this underscores the BoC’s point that the economy is now experiencing excess supply.

This excess supply will continue to depress inflation while the effect of previous interest rate increases will continue to impact demand. Remember that in Canada, mortgages are fixed for a much shorter period of time than in the US and this means households face higher borrowing costs when their mortgage rate resets higher. In fact, debt service costs as a proportion of household income are at 30+ year highs, which will contribute to sluggish consumer spending with the economy as a whole expected to grow only 0.9% this year.

We are forecasting inflation to average 2% next year, so given these economic conditions we see scope for meaningful interest rate cuts. We agree with the market pricing of another 25bp cut on 4 September and target a 3% overnight rate for second quarter 2025.

Canada inflation and unemployment

Source: Macrobond, ING

USD/CAD can find some support

The Canadian dollar has appreciated in line with the broader G10 FX moves and the very soft month for USD. However, the loonie cannot count on a strong domestic story, both on the macro side and – crucially – on the central bank side.

As we see the BoC cut three more times by the end of the year, there is no real reason for CAD to outperform other pro-cyclical G10 currencies. Incidentally, some gradual unwinding of the Trump trade in the background makes the likes of AUD and NZD more attractive than CAD. The new round of opinion polls after Labour Day can have some impact on FX, and CAD would outpace other commodity currencies only if Trump starts to regain momentum over Harris.

With 100bp fully priced into the USD OIS curve, the external environment may not get much better for CAD either. All in all, we think it is more likely that USD/CAD finds some support and settles above 1.35 as opposed to experiencing another major leg lower.

More By This Author:

Italian inflation Falls slightly

Polish CPI Up In August But Core Inflation Is Stable

Japan: Hotter Than Expected Inflation, Output Rebound Should Support The BoJ’s Policy Normalization

Comments

Log in or sign up to join the conversation.