Auto Markets Set For Major Disruption As Electric Vehicle Sales Reach Tipping Point

Major disruption is starting to occur in the world’s largest manufacturing industry. Hundreds of thousands of jobs will likely be lost in the next few years in auto manufacturing and its supply chains, as consumers move over to Electric Vehicles (EVs).

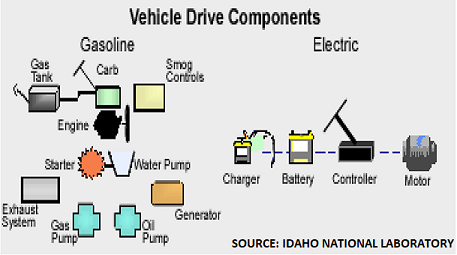

As the chart from Idaho National Laboratory confirms, EVs have relatively few parts – less than 20 in the drive-train, for example – versus 2000 for internal combustion engines (ICEs). There is much less to go wrong, so many servicing jobs will also disappear.

The auto industry itself was the product of such a paradigm shift in the early 19th century, when the horse-drawn industry mostly went out of business. Now it is seeing its own shift, as battery costs start to reach the critical $100/kWh levels at which EVs become cheaper to own and operate than ICEs.

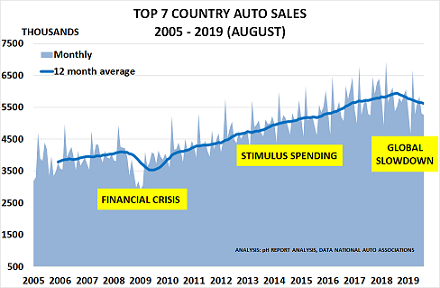

Unfortunately, this paradigm shift is coming at a time when global sales and profits are already falling. As the chart shows, sales were down 5.4% in January-August in the Top 7 markets versus 2018. And in the Top 6 markets, outside China, they were only 4% higher than in 2007, highlighting the industry’s current over-dependence on China:

- India is suffering the most, with sales down 15% this year

- But China’s woes matter most as it is the largest global market; its sales were down 13%

- Europe was down 3% YTD, but on a weakening trend with August down 8%

- All the major countries were negative in August, with Spain down 31%

- Russia was down 2%, despite the economic boost provided by today’s relatively high oil prices

- The USA and Japan were marginally positive, up 0.4% and 0.6% respectively

- Only Brazil was showing strong growth at 9%, but was still down 28% versus its 2011 peak

EV sales, like those of used cars, are heading in the opposite direction. China currently accounts for 2/3rds of global EV sales and sold nearly 1.3m EVs in 2018 (up 62% versus 2017). They may well take 50% of the Chinese market by 2025, as the government is now focused on accelerating the transition via the rollout of a national charging network.

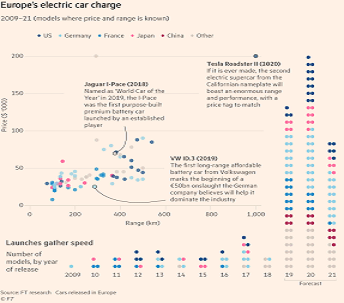

Interestingly, it seems that Europe is likely to emerge as the main challenger to China in the global EV market. The US has Tesla, which continues to attract vast investment from Wall Street, but it is only expected to produce a maximum of 400k cars this year. Europe, however, is ramping up EV output very fast as the Financial Times chart confirms:

- The left-hand scale shows EV prices v range (km) for EVs being released in Europe

- The right-hand scale shows the dramatic acceleration in EV launches in 2019-21

One key incentive is the manufacturers’ ability to use EV sales to gain “super-credits” in respect of the new mandatory CO2 emission levels. These are now very valuable given the loss of emission credits due to the collapse of diesel sales.

2020 is the key year for these “super-credits” as they are the equivalent of 2 cars, before scaling down to 1.67 cars in 2021 and 1.33 cars in 2022. Every gram of CO2 emissions above 95g/km will incur a fine of €95/car sold. And as Ford’s CEO has noted:

“There’s only going to be a few winners who create the platforms for the future.”

VW NOW HAVE BATTERY COSTS AT BELOW $100/kWh

VW is likely to be one of the Winners in the new market. It is planning an €80bn spend to produce 70 EV models based on standardised motors, batteries and other components. This will enable it to reduce costs and accelerate the roll-out:

- Its new new flagship ID.3 model will go on sale next year at a typical mid-market price of €30k ($34k)

- Having disrupted that market segment, it will then expand into cheaper models

- And it expects a quarter of its European sales to run on battery power by 2025.

The key issue, of course, is battery cost. $100/kWh is the tipping point at which it becomes cheaper to run an EV than an ICE. And now VW are claiming to have achieved this for the ID.3 model.

Once this becomes clearly established, EV sales will enter a virtuous circle, as buyers realise that the resale value of ICE models is likely to fall quite sharply. Diesel cars have already seen this process in action as a result of the “dieselgate” scandal – they were just 31% of European sales in Q2, versus 52% in 2015 .

One other factor is likely to prove critical. The media hype around Tesla has led to an assumption that individuals will lead the transition to battery power. But in reality, fleet owners are far more likely to transition first:

- They have a laser-like focus on costs and often operate on relatively regular routes in city centres

- They don’t have the “range anxiety” of private motorists and can easily recharge overnight in depots

The problem for auto companies, their investors and their supply chain, is that the disruption caused by the paradigm shift will create a few Winners – and many Losers – as Ford warned.

Those who delay making the investments required are almost certain to become Losers. The reason is simple – if today’s decline in auto sales accelerates, as seems likely, the investment needed for EVs will simply become unaffordable for many companies.

Disclosure: I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this ...

more