Argentina: Back To The Debt Negotiating Table

The Fernandez administration has favored temporary fixes over long-term adjustments to address Argentina’s macro imbalances. Price and FX controls should become harder to sustain if the debt-restructuring process takes long to complete, with May's heavier debt maturities standing out as an important deadline if the goal is limiting FX outflows.

Temporary fixes, long-term problems

Since taking office in December, the new Alberto Fernandez administration has implemented a series of emergency measures covering different aspects of the country’s fiscal and monetary policy stances. These included initiatives that should result in about 1.5-2.0% of GDP in additional fiscal revenues, along with a series of temporary measures to help mitigate short-term pressures on the inflation and FX fronts, chiefly through stringent price and FX controls.

These are not permanent solutions for Argentina’s macroeconomic imbalances, as illustrated by the absence of monetary policy targets. But, on balance, these initiatives may provide an adequate short-term respite for the administration to address its main challenge, ie, the restructuring of the sovereign’s outstanding debt.

Negotiations with debtholders should intensify in the coming weeks, but the stated hope for a quick resolution, with March still held as the targeted deadline for the conclusion of the talks, looks unrealistic.

The insistence on a quick resolution probably reflects the fact that the government would like to resolve this uncertainty as quickly as possible, to minimize the drag it will continue to have on economic activity. Economic activity appears to be stabilizing after a deep 2-year recession (when GDP accumulated a 6% contraction), but the consensus still points to a slight recession in 2020. Inflation expectations are, meanwhile, down-trending, but remain far too high (still above 40%), down from the 54% 2019 print.

In any case, as indicated by the wide dispersion of analyst estimates for each of these variables, assessing the outlook for Argentina’s macro indicators remains clearly a low-conviction exercise, as much should depend on the timing and the end-result of the debt renegotiation process.

Risk of a protracted negotiating process is high

Given the limited information provided so far by Fernandez’s team, assessing Argentina’s likelihood of default and the final outcome of the debt renegotiation process also remains far from a trivial exercise.

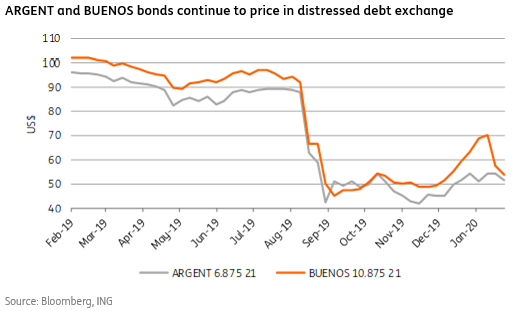

Investors have been bracing for challenging and protracted negotiations, with external sovereign bond prices continuing to linger in the US$40-50 range. This indicates expectations of a low recovery value, with negotiations likely entailing a combination of a long grace period, coupon reductions and an outright debt relief. Given the federal government’s high debt burden (with debt/GDP near 90%), high concentration of FX debt (at about 80%), and high-interest costs (about 20% of revenues), a more market-friendly debt exchange, like Uruguay in 2003 and Ukraine in 2015 (with recovery values of 66% and 80%, respectively, according to Moody’s) appear unlikely.

The complexity of this exercise also reflects the fact that it involves debt from different jurisdictions (local/foreign), denominated in different currencies, issued with different clauses – such as collective action clauses (CAC), cross-default and acceleration clauses – and held by groups with different incentives (private foreign/local, local government, IFIs, and Paris Club).

A taste of what’s to come is already taking place, with the attempt by the Buenos Aires province to postpone a principal payment that was due at the end of January. Given the nature and clauses of this bond, ie, an external debt issuance with collective action and acceleration clauses, the provincial administration would need the consent of a 75% majority of bondholders to change the bond’s terms.

The provincial administration has so far failed to attract enough bondholder interest and now it faces a fast-narrowing grace period to resolve the situation. The consequences of failing to make a payment this month could be severe, especially due to the acceleration clause. Even though the default would effectively be limited to the BA province, the noise generated could be detrimental to the federal government’s debt-negotiation process.

A sovereign default is unlikely to be imminent

Despite the ongoing BA province episode, we will assume that the federal government is unlikely to default “willingly”. This will help us assess the government’s “ability” to continue to service its debt this year, to have a clearer understanding of the evolution of the constraints faced by the negotiators, or the timing of eventual default.

We will also assume that the chief constraint faced by the federal government is the amount of hard currency freely available at the central bank to pay FX-denominated debt. These so-called net FX reserves currently stand at about US$15bn. There are both local-law and foreign-law FX-denominated debt, but a special focus on foreign-law bonds is warranted. This reflects several considerations:

- the fact that external-law bonds have CACs, acceleration and cross-default clauses,

- the fact that defaulting on these instruments would also trigger CDS payments, and

- our assumption that bondholders are considerably less likely to successfully litigate against the government in local courts.

In fact, the government has already unilaterally reprofiled all its local-law short-term debt, and further reprofiling should not be discarded. In particular, we assume that the scheduled US$9bn payment in LETES bills (short-term local debt settled in USD) due in August should be reprofiled or swapped for a long-term bond.

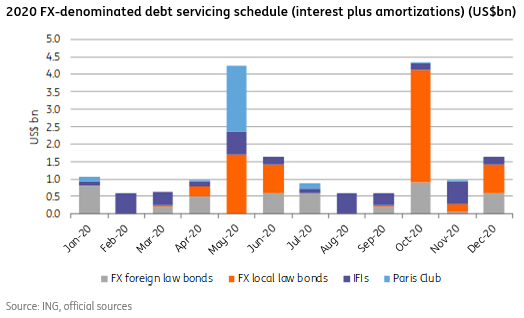

Our conclusion, when analyzing the Treasury’s 2020 foreign-law debt-servicing schedule, is that the Fernandez administration could, in principle, muddle through and avoid a default until year-end. However, that could be accomplished with increasing headline noise and market volatility after May.

As illustrated in the chart above, during 2020, the Treasury’s debt-servicing requirements includes: US$4.4bn due to private creditors, US$4.2bn due to IFIs and US$2.2bn due to the Paris Club. An additional US$7.2 in debt-servicing for local-law USD-denominated long-term debt would also affect FX reserves but, there’s a considerable risk that, like the LETES payment, these may also be reprofiled or swapped.

Compared to the amount of freely available FX reserves available today, these are relatively high amounts. Moreover, as the ongoing imbroglio with the BA province shows, other issuers should also have foreign currency needs as well.

Local market conditions could become more volatile after May

The ideal scenario for the government would be to conclude the renegotiation of all its long-term debt by April. In May, as seen in the chart above, market tension would tend to increase in anticipation of the heavier debt servicing schedule for that month, which includes a US$2bn amortization due to the Paris Club, and the US$1.3 due in the BONAR 24, a local-law USD-denominated bond.

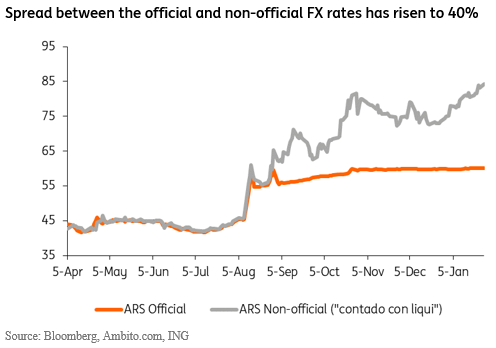

By then, if the debt renegotiation hasn't been concluded, there will probably be some tensions arising in the FX market (ie, a growing gap between the non-official and official FX rate, as seen in the chart below), and additional FX market restrictions, possibly affecting imports.

Overall, assuming a scenario in which the administration would postpone all local-law USD-denominated debt-servicing, it appears that they could have enough FX reserves to service all its foreign-law debt-servicing requirements until yearend.

But this is far from an ideal scenario for the Fernandez administration, given the increasing financial market volatility it would generate and the persistent drag this uncertainty would represent for the economic recovery.

IMF's involvement remains unclear

The Fernandez administration could also buy some time by seeking an agreement with the IMF, reviving the US$56bn Standby Agreement, and possibly regain access to the disbursements that were interrupted after the August primaries.

Following a meeting between Economy Minister Martin Guzman and IMF representatives this week in New York, the Fund has agreed to send a technical mission to Buenos Aires next month.

It’s still unclear if Fernandez will seek an understanding with the Fund right away, or will prioritize an agreement with private bondholders, before seeking the IMF’s stamp-of-approval. The initial signs from the administration suggested continued reluctance to prioritize the Fund.

Having an IMF program in place would make any new agreement with private bondholders much more credible, also presumably because of the conditionalities the Fund would impose on Argentina. However, the IMF’s involvement could possibly delay negotiations by turning Argentina’s negotiating stance more stringent, by demanding a larger haircut.

This would reflect the fact that debt-sustainability exercises conducted by the Fund, similar to the one included in the Fund’s June 2019 Article IV report, should likely conclude that, at current levels, Argentina’s public debt trajectory is unlikely to stabilize in the foreseeable future.

At the time, the Fund concluded that “Argentina’s debt is sustainable, but not with a high probability”. And given the deterioration in macroeconomic dynamics since then, the assumptions used in that analysis look quite optimistic now. As a result, the Fund’s assessment likely became considerably direr.

Limited contagion risk from Argentina on other sovereigns

Market consensus is that Argentina’s recession will continue in 2020, albeit at a shallower pace. Another year of recession is bound to continue to depress consumption and imports from its regional peers. Brazil’s manufacturing exports to the country have been particularly affected, and that should continue until a recovery takes place. However, given the large-scale adjustment that already took place in recent quarters, with imports dropping 25% in 2019 and imports from Brazil falling by a larger 35%, the scope for further import reduction has been sharply reduced.

The risk of financial market contagion in the event of a default, for instance, is possibly larger, but even then, it should remain relatively limited and, as seen after the election primaries in August last year, any contagion is likely to be temporary.

Mitigating factors should help limit the negative fallout for other emerging market sovereigns. These include the fact that Argentina’s troubles are long in the making and are seen as largely self-inflicted. Current bond pricing already indicates expectations for a low recovery value, implying less room for a downside surprise. Meanwhile, the market backdrop has remained strong reflected by ongoing inflows into EM debt (US$8bn in the first three weeks of 2020 according to EPFR Global), containing wider selling pressure from idiosyncratic events.

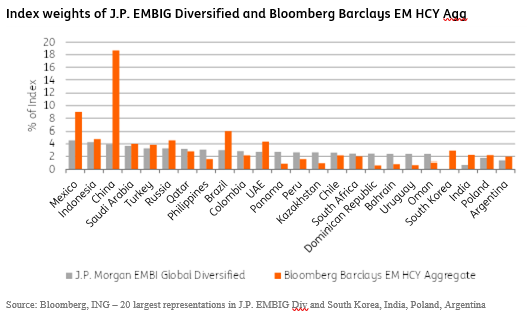

Structurally, we also note that investors’ average exposure to Argentina has dropped significantly as the growing EM universe over the last two decades resulted in the dilution of index weights. Argentina specifically has seen its share in the J.P. EMBI Global Diversified falling from north of 10% at the turn of the century to below 2%. Meanwhile, the number of individual country risks within the EMBIG Diversified has more than doubled from below 30 to 73. All in all, this implies a lower concentration risk and limited fallout from Argentina.

A less constructive assessment could emerge, however, in the context of a reversal in the supportive backdrop and flow picture we have now, which would increase the scrutiny on sovereigns with weaker fiscal and external balance sheets.

The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. more