2021 Outlook For Belgian And Dutch Housing Markets

Given the pandemic, the steep house price increases seen in both Belgium and the Netherlands last year were a surprise. However, three factors helped to drive confidence and demand in the housing market. Firstly government support, secondly, increased investor activity and finally a further decrease in interest rates improved affordability of homes.

Belgium

House price growth was unexpectedly strong in 2020 in Belgium. Income support provided by the government, increased activity by investors and low interest rates can explain the strong growth. Looking at 2021, we expect the upward pressure from these factors to fade, leading to more modest growth figures for the year.

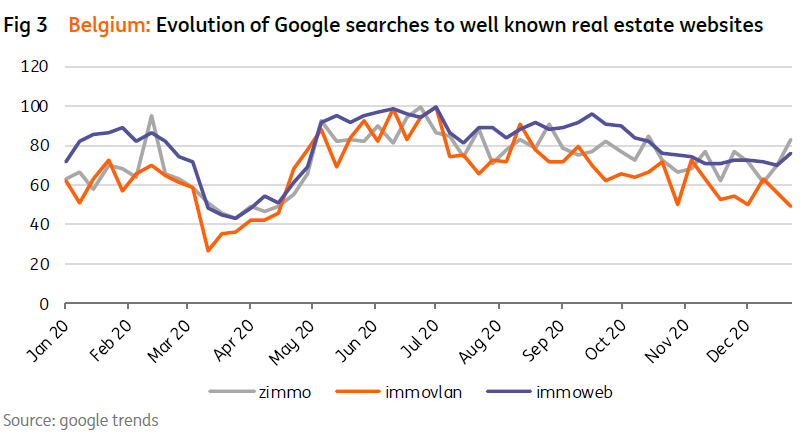

Interest in residential real estate in Belgium recovered rapidly after the first lockdown in March 2020. The number of Google searches made to well known Belgian real estate websites even rose to a level that was higher than before the lockdown and a recovery in the number of transactions followed.

There is evidence that housing preferences shifted during the crisis with more interest than usual in houses and apartments that were larger and had a garden or terrace.

Despite the rapid recovery in activity, the number of transactions for 2020 as a whole is expected to be much lower compared to 2019 (official figures will only be published in April). This is obviously due to the disruption from COVID-19 lockdowns, but also to do with the abolition of the ‘woonbonus’ in Flanders, a system of tax deduction for households with a mortgage. The announcement of the abolition led to a rush on real estate at the end of 2019.

House price evolution is expected to be remarkably positive when official figures for 2020 as a whole become available in April. Unofficial sources point to house price increases of close to 6%. Part of this sharp growth could be explained by the shift in preferences by house buyers towards more expensive houses. If a greater number of expensive houses was sold during 2020 compared to 2019, then the median price will increase. So part of the price increase might be explained by a composition effect.

But there are also several macroeconomic factors that explain the vibrant price evolution. A first crucial factor is the interest rate. The European Central Bank did everything it could to keep the market rate down and we see that this translated into a decline in the average mortgage rate in Belgium in 2020. Low mortgage rates are a fundamental aspect of the purchasing power of households as a small change in the mortgage rate has a large impact on the loan capacity. If the mortgage rate drops from 1.7% to 1.4%, as it did over the course of 2020, then the loan capacity increases by 3% for a mortgage with a maturity of 20 years.

The fall in the average mortgage interest rate, however, is also related to the macroprudential policy pursued by the National Bank of Belgium. Under new rules in force since January 2020, there are restrictions on the loan amount in relation to the value of the home (loan-to-value ratio). This ensures that banks grant fewer loans with very high loan-to-value ratios. As these new loans are less risky, they have a lower mortgage interest rate, and so the average mortgage interest rate falls.

A second factor contributing to the strong price growth has been the income supporting measures from the government. Income loss for households on a macroeconomic level was moderate due to these policies. The moratorium on mortgage payments also supported prices in ensuring fewer forced sales, which are generally a cause of downward price pressure.

Furthermore, those households that suffered loss of income as a result of the pandemic are generally not the households that are looking to buy a house. Home ownership is lower among lower income households, and the COVID-19 crisis has had a greater negative impact on sectors in which average wages are lower.

Lastly, we note that the low yield on bonds and high volatility of the stock market over 2020 made an investment in physical real estate more attractive for many Belgians. Hence, real estate investors also supported house prices.

Can this high house price growth continue?

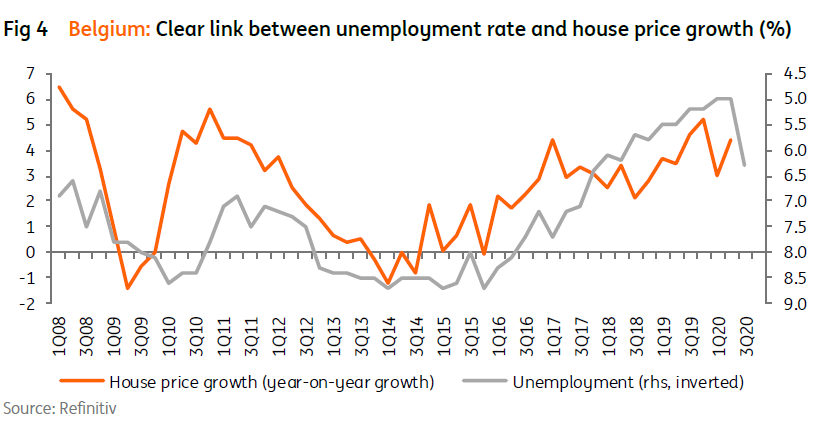

The factors that influenced the high house price growth in Belgium in 2020 will fade over the coming months, we believe. The second wave of the pandemic and the negative effects of the first wave will cause unemployment to rise, even in sectors not directly affected by the pandemic, putting downward pressure on house prices.

The Belgian government’s income support measures are expected to become more targeted during the second wave and will inevitably result in a loss of income for a larger number of families. And the moratorium on mortgage interest payments will eventually expire. In addition, the strong house price increases will dampen the attractiveness of real estate for investors.

In 2021, we expect the real estate market to cool, with lower quarter-on-quarter growth figures. However, due to base effects, the expected growth for the full year is still high, at 3%.

The Netherlands

The Dutch housing market is still showing strength despite the COVID-19 crisis. Stable affordability, increased activity by investors and further tightening of the housing market explain why prices have on average increased by 7.8% on an annual basis (+6.9% in 2019). For 2021, we assume a cooling of the housing market, but the surrounding uncertainties are higher than normal. The pace of economic recovery and developments in confidence in the housing market and interest rates will largely determine the impact of the crisis on the housing market in 2021.

1) Affordability maintained in 2020

Two factors positively affected the affordability of homes in 2020: disposable income increased on average, while unemployment among potential home buyers remained low. It was mainly young people with flexible employment contracts that faced unemployment due to the COVID-19 pandemic in 2020. In combination with a further fall in mortgage interest rates of around 0.3ppt on average, this has sustained the affordability and demand for homes.

2) Increased activity by investors in 2020

Investor interest in the housing market has increased further. In the first half of 2020, private landlords accounted for about 20% of all home purchases, a higher rate compared to the same period in 20191. This has put extra upward pressure on house prices. An increase in transfer tax from 2% to 8% for buy-to-let houses as of January 2021 has led to a year-end rush by investors, providing further upside pressure to the market in 2020.

Confidence bounces back to normal and further tightening of housing market

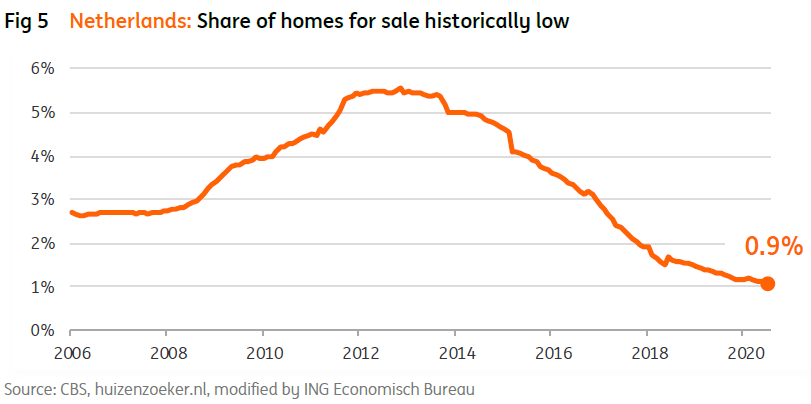

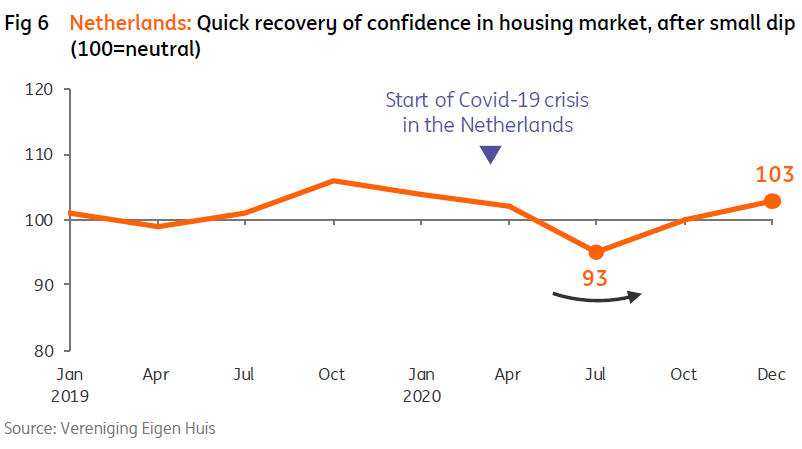

Unlike in previous economic crises, Dutch consumers have remained confident in the housing market. This partly explains the 7.7% increase in the number of home sales in 2020 compared to 2019. A further tightening of the housing market has been the result, as becomes clear from the share of owner-occupied homes that are for sale. This share fell from 1.2% to 0.9% during 2020, the lowest level ever reported. The rapid recovery of confidence in the housing market can be explained by two factors. First, as already mentioned, income losses of potential home buyers have so far been limited. This is due to the government’s stimulus policy in response to the crisis. Second, the COVID-19 crisis is not caused by vulnerabilities in the economy, but has an epidemiological cause and rapid economic recovery seems possible once the virus is under control. Both factors contributed to the quick recovery of confidence in the housing market in the second half of the year, after a small decline from April to July. The quick recovery of confidence has prevented a drop in home sales and resulted in a further tightening of the housing market in 2020. This helps to explain last year’s strong activity in the Dutch housing market.

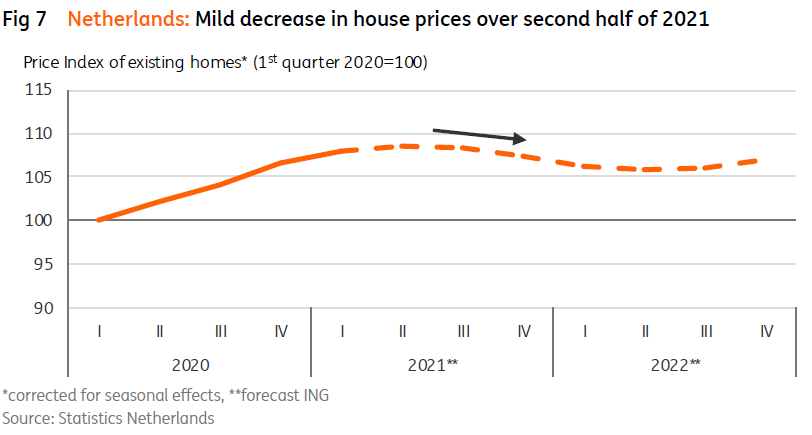

Base case for 2021: cooling down of the housing market

ING takes a cooling down of the Dutch housing market as base case for 2021. The economic impact of the COVID-19 crisis and phasing out of government support will lower confidence levels in 2021. And unlike in 2020, the crisis will increasingly affect people with fixed employment contracts in 2021. As a result, potential home buyers will more often postpone their purchasing plans. A gradual increase in interest rates with a more moderate wage increase than in 2020 will, on average, mean affordability declines. First time buyers – about 30% of the market - will experience a windfall, as for them the transfer tax of 2% no longer applies. Higher interest rates, higher transfer taxes for buy-to-let and lower rents will, on the other hand, discourage investors. Hence, in our base case scenario we assume a flattening of price increases in the first half of 2021, followed by a mild decline in house prices continuing until the beginning of 2022. At the lowest point, we see house prices about 2.5% lower on average than the price peak in 2021. On an annual basis, house prices in our base scenario are still 5.0% higher compared to the 2020 average2. Home sales are expected to fall by 10% in 2021 compared to last year, due to lower confidence levels and the limited supply of homes.

…but uncertainties for second half of the year are greater than ever

Our base case, however, could easily become outdated. Uncertainties on the housing market are greater than ever. First, there is uncertainty about the economic impact of the COVID-19 crisis. Second, the role of psychological factors on the housing market increase uncertainty levels around short-term house price developments. Future confidence in the housing market will be a result of a mixed bag of influences, such as unemployment development, economic performance and interest rate developments. A turn in confidence could happen rapidly. Together with the high cyclicity of the housing market and many self-enforcing mechanisms, this amplifies the possible impact of the crisis on the housing market. The most positive scenario is a situation in which the economy recovers fast, the COVID-19 virus is successfully controlled and interest rates remain low. This will support consumer confidence and limit income losses of households, thereby preventing a significant drop in housing demand. In this scenario, wealth effects of second-time buyers could lead to even further prices increases. If, however, economic recovery takes longer, uncertainties related to the pandemic remain high and push risk premiums in mortgage rates up, and this could result in plunging housing demand and lower house prices.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more