Image Source: Pexels

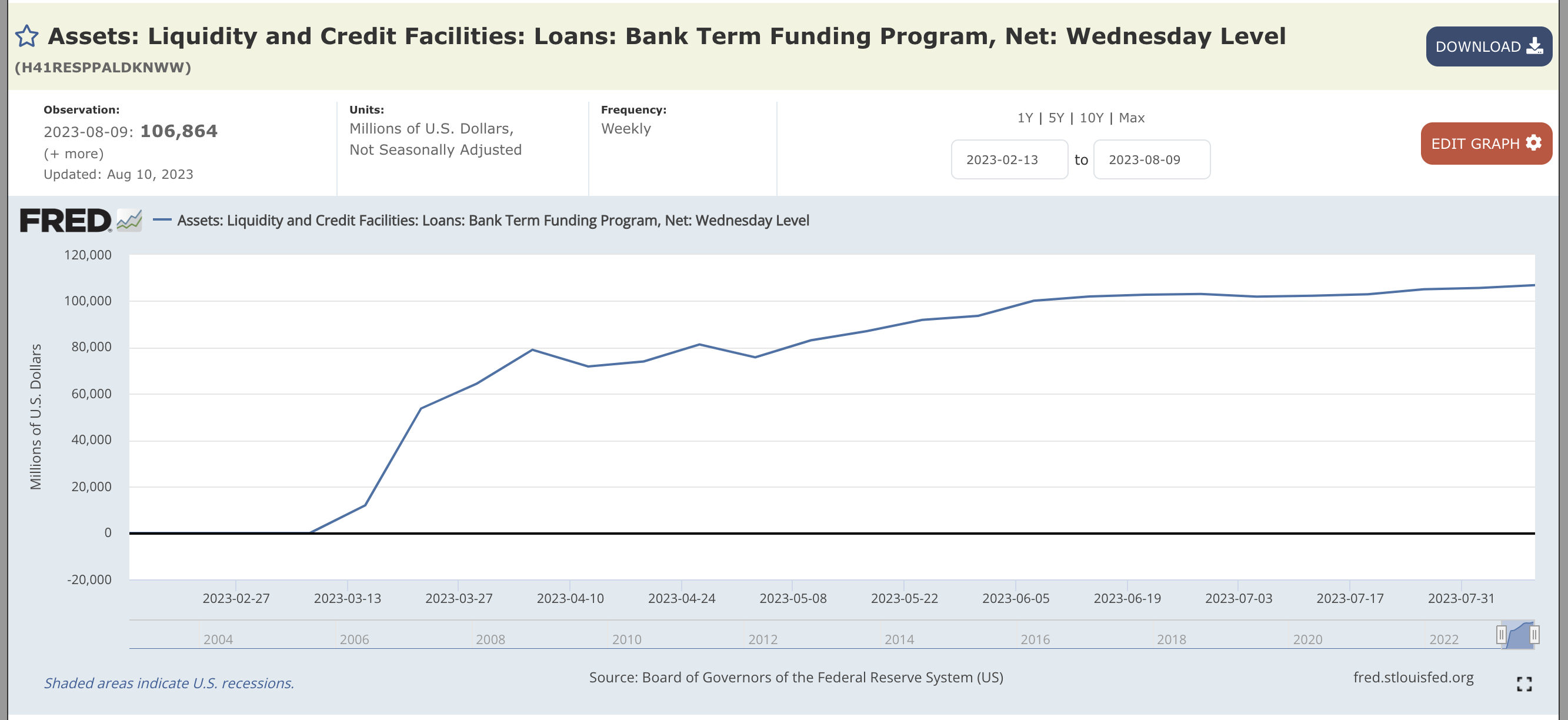

In another sign the financial crisis continues to bubble under the surface, banks borrowed an additional $3.7 billion from the Federal Reserve’s bank bailout program in July.

Currently, there are $106.9 billion in outstanding loans in the Bank Term Funding Program (BTFP).

After the collapse of Silicon Valley Bank and Signature Bank, the Fed created the BTFP, allowing banks to easily access capital “to help assure banks have the ability to meet the needs of all their depositors.”

The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging US Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. Banks can borrow against their assets “at par” (face value).

According to a Federal Reserve statement, “the BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.”

The ability to borrow against the face value of their bond portfolios is a sweetheart deal for banks given the big drop in bond prices.

As the Fed jacked up interest rates to fight price inflation, it decimated the bond market. (Bond prices and interest rates are inversely correlated. As interest rates rise, bond prices fall.) With interest rates rising so quickly, banks were not able to adjust their bond holdings. As a result, many banks have become undercapitalized on paper. The banking sector was buried under some $620 billion in unrealized losses on securities at the end of last year, according to the Federal Deposit Insurance Corp.

The BTFP gives banks a way out, or at least the opportunity to kick the can down the road for a year. Instead of selling bonds that have dropped in value at a big loss, banks can go to the Fed and borrow money at the bonds’ face value.

In the first week of the BTFP, banks borrowed $11.9 billion from the program, along with more than $300 billion from the already-established Fed Discount Window.

The Discount Window requires banks to post collateral at face value and loans come with a relatively high interest rate (currently 5.5%). While Discount Window borrowing surged in the weeks after the collapse of SVC and Signature Bank, the balances were quickly paid back down, and Discount Window borrowing returned to normal levels.

But BTFP balances continued to climb.

(Click on image to enlarge)

The fact that banks are still accessing the bailout program, and the pace of borrowing seems to have ticked up in July, reveals that the banking sector remains shaky.

There are other signs that all is not well in the world of banking.

Moody’s recently cut the credit rating of 10 small and midsize banks, placed six large banks on review for potential downgrades, and revised 11 more banks from a stable outlook to a negative outlook.

“As you look ahead, it doesn’t feel like the pressure from interest rates being higher and overall monetary policy tightening is close to abating,” Moody’s associate managing director Jill Cetina said.

We’ve seen funding strains in the banking sector. The interest rate risk, I think, was something that the US banking sector was not prepared particularly well for, and because of that, we have some challenges at certain banks.”

Most people blame the shakiness in the financial sector and the broader economy on recent interest rate hikes, but the real problem started years ago.

After the Great Recession, Federal Reserve policy intentionally incentivized borrowing to “stimulate” the economy. But this monetary inflation inevitably led to price inflation. That forced the Fed to raise interest rates. The central bank managed to cool price inflation (for now), but it also broke the financial system and loaded the economy with debt.

In effect, the Fed managed to paper over the financial crisis with this bailout program. It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

And it’s only a matter of time before something else breaks.

More By This Author:

Great News! Or Is It?

Another Blow To The Petrodollar: India And The UAE Complete First Oil Sale In Rupees

Silver Price Inexcusably Low Given The Market Dynamics

Comments

Log in or sign up to join the conversation.