Fact And Fiction About Low-Risk Investing

One of the most popular and successful strategies over the last decade has been low-risk (i.e., low-beta or low-volatility) investing. New research shows that those strategies have persisted even after the publication of the research documenting their existence, and that they can be pursued in low-cost, low-turnover portfolios.

One of the big problems for the first formal asset pricing model developed by financial economists, the capital asset pricing model (CAPM), was that it predicts a positive relationship between risk and return. However, the historical evidence demonstrates that the slope of the security market line is flatter than the CAPM suggests. Most importantly, the quintile of stocks with the highest beta meaningfully underperform those in the lowest-beta quintile – high-beta stocks provide the lowest returns while experiencing much higher volatility. The publication of research findings led to low-risk (low-beta and low-volatility) investing receiving a tremendous amount of attention, especially since the financial crisis that began in late 2007.

Three economic theories explain the low-risk anomaly:

- Many investors are either constrained against the use of leverage or have an aversion to its use. Such investors who seek higher returns do so by investing in high-beta stocks despite the fact that the evidence shows they have delivered poor risk-adjusted returns. Limits to arbitrage and aversion to shorting, as well as the high cost of shorting such stocks, prevent arbitrageurs from correcting the pricing mistake.

- Some individual investors have a “taste” for lottery-like investments. This leads them to “irrationally” invest in high-volatility stocks (which have lottery-like distributions) despite their poor returns. They pay a premium to gamble.

- Mutual fund managers who are judged against benchmarks have an incentive to own higher-beta stocks. In addition, managers’ bonuses are options on the performance of invested stocks and thus are more valuable for high-volatility stocks.

Those three theories provide reasons to believe that the low-risk premium not only exists but is also likely to persist.

AQR Capital Management’s Ron Alquist, Andrea Frazzini, Antti Ilmanen and Lasse Pedersen contribute to our understanding of the low-risk anomaly with their February 2020 paper, Fact and Fiction about Low-Risk Investing. Their analysis uses metrics created by ranking U.S. stocks each month since 1931 for six statistical risk metrics, or since 1957 for four fundamental risk measures that have later data availability. The six statistical risk metrics are: the betting-against-beta (BAB) factor – buying stocks with low beta and selling stocks with high beta; the stable-minus-risky (SMR) factor, which ranks stocks using betas but weights them in a dollar-neutral rather than a market-neutral way, resulting in negative exposure to beta; SMRMN, the market-neutral version of SMR; the betting-against-correlation (BAC) factor; idiosyncratic volatility (VOL); and maximum recent daily return (MAX). The four fundamental risk measures are quality-minus-junk (QMJ), which is based on 16 single metrics, and its subgroups profitability, growth and safety.

Following is a summary of their findings:

- Low-risk strategies outperform, delivering alphas relative to commonly used factor models (Fama-French three- and five-factor plus momentum).

- Low-risk strategies have similar CAPM alphas to the other common factors.

- The low-risk premium is significant out-of-sample. The authors wrote: “They have actually performed better during the out-of-sample period than during the in-sample period.”

- Low-risk strategies work within industries, disputing the myth that their performance is based on industry bets.

- Low-risk strategies have some sensitivity to interest rates (for example, the standard BAB, which is not industry-neutral, exhibits no significant equity market beta, but it does have a statistically significant bond beta). However, the impact on alpha is modest.

- The risk-adjusted performance of low-risk strategies is pervasive across countries and has been robust across many asset classes and even outside financial markets. For example, the QMJ strategy has delivered positive excess returns and negative market betas in 22 of the 24 countries. And while the term premium exists for short- and long-term bonds, short-term bonds deliver larger risk-adjusted returns – the slope of the term premium is not steep enough.

- Low-risk investing can be implemented with moderate turnover, refuting the claim that it doesn’t survive transactions costs. Low-risk strategies also have significant CAPM alphas among both large stocks and small stocks. Like with most strategies, low-risk investing does work better in small caps, perhaps because of higher variation in betas and more limits to arbitrage.

- Long-only, low-risk investing does lose money in down markets, though less so – due to beta being well below 1. The BAB is designed to be market neutral, and thus BAB can lose money in bull and bear markets. The QMJ strategy has a small negative beta and therefore makes money more often than not in bear markets. The long-short SMR (dollar-neutral) strategy has a negative net beta of around -0.8 and thus made money in all bear markets.

The authors addressed the claim that “the CAPM is dead and so is low-risk investing.” They noted: “If the CAPM does not work because the SML is too flat, then low-risk investing must be profitable!” They explained: “Fama and French state that the low-risk effect can be explained by their two newest factors, profitability (RMW) and investment (CMA). Even if true, this means that low-risk investing is profitable but can be ‘explained’ by fundamental low-risk factors; recall that profitability is one of the fundamental low-risk factors. We are ‘explaining’ low-risk using low-risk.”

You cannot believe both that the CAPM is dead and that low-risk investing does not work. Either the CAPM holds, or BAB can be explained by non-CAPM factors – evidence in favor of BAB.

Finally, the authors also addressed the claim that low-risk strategies have become so expensive that they cannot do well going forward. They noted: “A long-standing concern has been that low-risk stocks have increased in value relative to high-risk stocks, creating a potential headwind for low-risk investing in the future.” They then noted: “Low-beta stocks were extremely cheap during the tech bubble 20 years ago and have looked richer since then. The recent value spreads of the US BAB equity strategy are at a moderately rich level that is similar to the one that prevailed at the end of 2009. Yet, BAB has been among the best-performing factors in 2010s.” They concluded: “This strong performance during a period of moderate richness is an example of factors being difficult to time-based on their value spreads.” That said, they also noted that investors who are concerned with valuation spreads can simply combine strategies by buying cheap, low-risk assets. With that in mind, let’s review the literature that examined this issue.

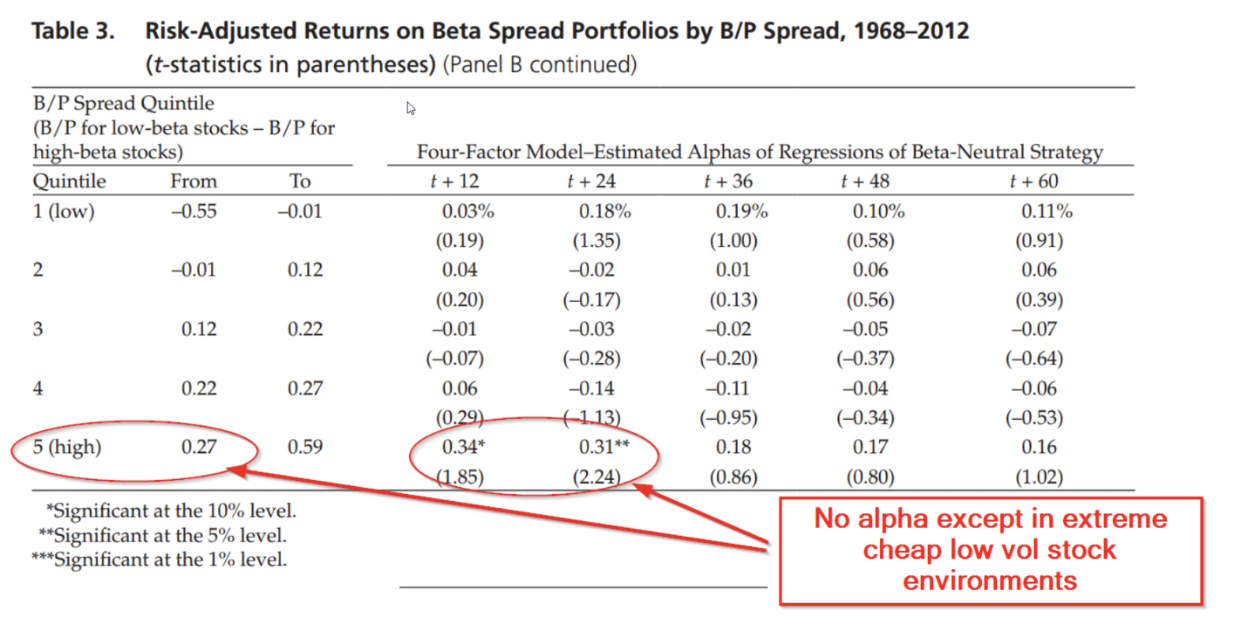

Historically, there is a clear relationship between valuation and low-volatility strategies. The paper, Low-Volatility Cycles: The Influence of Valuation and Momentum on Low-Volatility Portfolios, published in a 2015 issue of the CFA Institute’s Financial Analysts Journal, summarized the situation (the paper was also summarized in an Alpha Architect article). The authors wrote: “Our results suggest time-variation in the performance of low-risk strategies is likely influenced by the approach to constructing the low-risk portfolio strategy and by the market environment and associated valuation premia.”

The table below from the study highlights the key result:

A 2012 paper by Pim van Vliet, Enhancing a Low Volatility Strategy is Particularly Helpful When Generic Low Volatility is Expensive, highlighted a similar finding. For the period 1929 through 2010, while on average low-volatility strategies tended to have exposure to the value factor, that exposure was time-varying. The low-volatility factor spent about 62% of the time in a value regime and 38% of the time in a growth regime. The regime-shifting behavior impacts the performance of low-volatility strategies. When low-volatility stocks have value exposure, they outperformed the market on average by 2.0%. However, when low-volatility stocks have growth exposure, they underperformed on average by 1.4%.

Investors in low-volatility strategies should be aware of current valuations.

Summary

Low-risk securities have historically delivered higher risk-adjusted returns than high-risk assets. They have also performed well after their discovery and in other asset classes and countries, are backed by economic and behavioral theories of leverage constraints and lottery demand, and can lose money when the market is down. In addition, low-risk investing does not require high turnover (because safe securities tend to remain safe for a long time), nor is it only present among securities with high transaction costs. It is also neither an industry nor a bond market bet.