Financial Stocks Are Unattractive

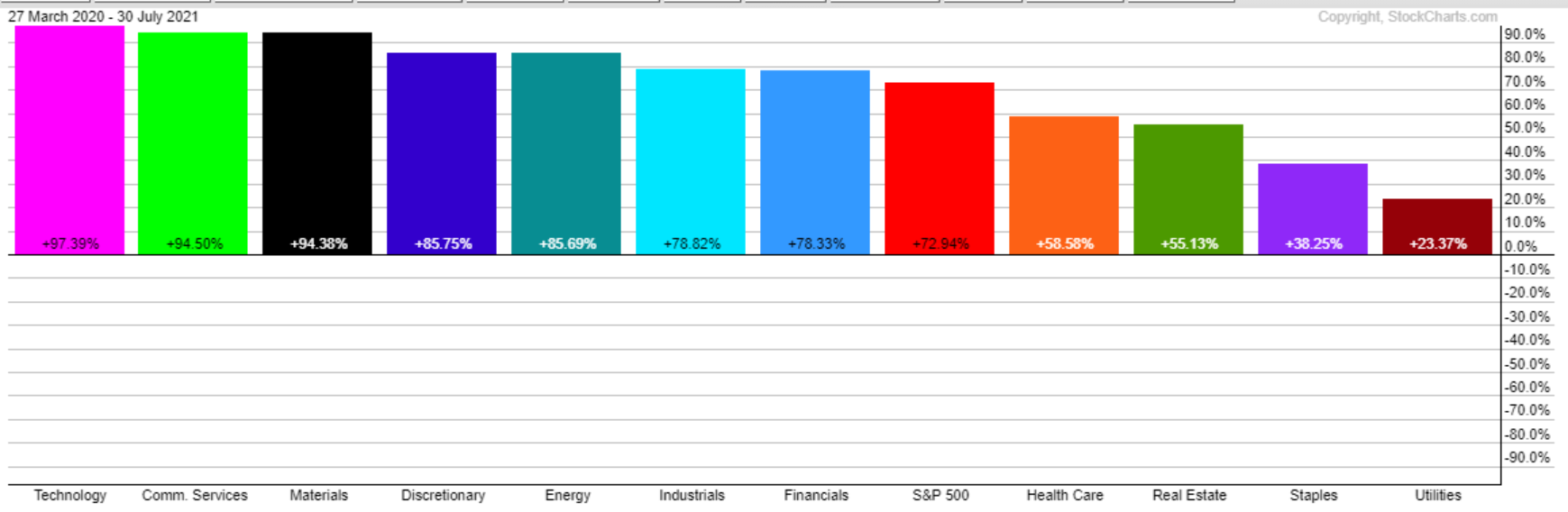

Since March 2020, the beginning of a new business cycle, financial stocks have provided solid return +78% (S&P 500: +73%) as shown in the chart below.

Utilities (NYSEARCA: XLU), staples (NYSEARCA: XLP), healthcare (NYSEARCA: XLV), and real estate (NYSEARCA: XLRE) were the worst performers. These sectors perform well in the declining phases of the business cycle and underperform in the rising phases of the business cycle.

(Click on image to enlarge)

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management

Financial stocks performed well because they outperform the market during the rising phase of the business cycle. The reason for this outperformance was the strengthening of the business cycle since March 2020. This important pattern was reviewed in my article “Bank Stocks, Interest Rates, And Business Cycles - Not That Obvious (March 25, 2021)”.

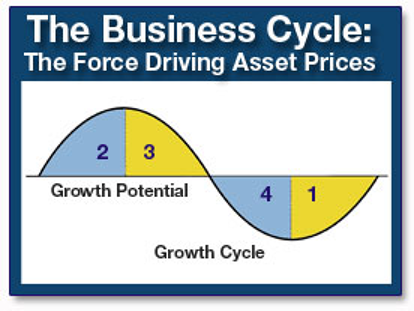

There have been important changes in the economy and in our business cycle indicator to suggest some adjustments to the outlook for financials and bank stocks.

Source: The Peter Dag Portfolio Strategy and Management

The downturn of the business cycle (Phases 3 & 4) reflects a significant slowdown in business activity. This is the time when portfolios should avoid cyclical sectors and be overweight defensive sectors and bonds as I discussed in my article here.

The decline of the business cycle is anticipated by a rise in commodities and inflation. The reason is these trends undermine consumers’ purchasing power. The resulting slowdown in demand is not recognized at first by business which remains mainly focused on replenishing inventories. Production must be increased to meet sales growth.

Eventually, because of slowing demand, inventories start rising faster than sales. The decision must be made to reduce production to cut inventories.

The reduction in production requires a cut in working hours. The cut in working hours is followed by layoffs, reduction in purchases of raw materials and borrowing to finance operations.

The forces unleashed by the inventory correction are visible in slower growth in manufacturing employment, declines in commodity prices, and lower yields.

This transition from Phase 2 to Phase 3 has major strategic importance for investors. Stocks outperforming during the strong phase of the business cycle (such as industrials) start disappointing because of the uncertain outlook for their profits. The defensive sectors (such as utilities), on the other hand, begin to outperform as investors choose them for their reliable profitability.

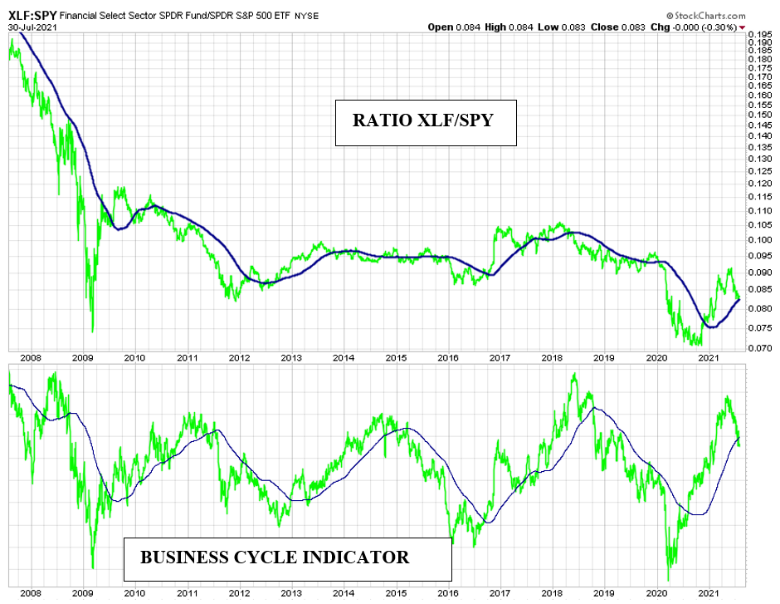

The following chart reviews the performance of the financial stocks (NYSEARCA: XLF) with the updated version of our business cycle indicator.

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management.

The above chart shows the ratio of XLF (financials) and SPY (S&P 500). XLF outperforms SPY when the ratio rises. XLF underperforms SPY when the ratio declines. Investors should be overweight financial stocks when the ratio rises and be underweight financials when the ratio declines.

The lower panel of the chart shows the business cycle indicator, a proprietary indicator updated in each issue of The Peter Dag Portfolio Strategy and Management. The graphs show the best time to own financials is when the business cycle indicator rises, reflecting a strengthening economy.

The business cycle indicator has been declining, as discussed also in previous articles. A likely continuation of the declining of the business cycle indicator points to underperformance of the financial stocks.

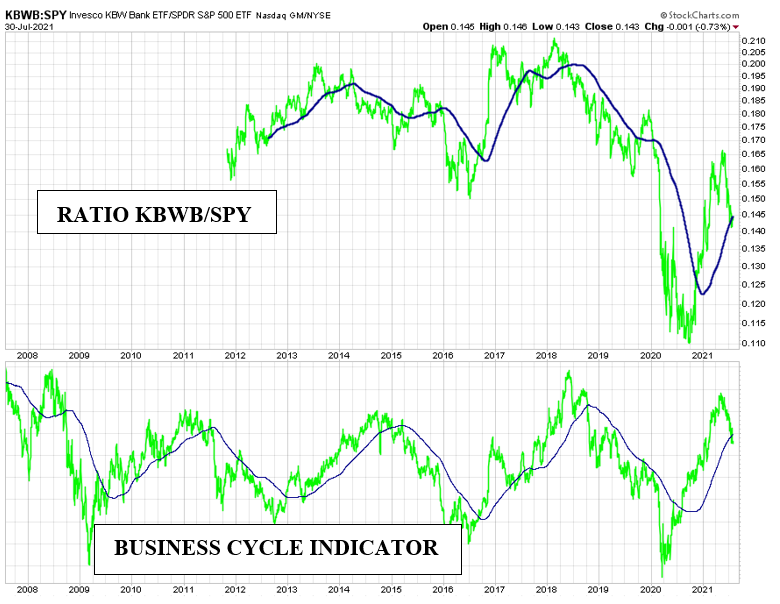

The following chart shows how the banking sector, a subset of the financial sector, performs during a complete business cycle.

The above chart shows the ratio of KBWB and SPY. The Invesco KBW Bank ETF (NASDAQ: KBWB) normally invests at least 90% of its total assets in companies primarily engaged in US banking activities. KBWB outperforms SPY when the ratio rises. KBWB underperforms SPY when the ratio declines.

The above graphs show KBWB performs like XLF during a business cycle. The time to be overweight in KBWB is when the business cycle indicator (lower panel) rises, reflecting a strengthening economy. Investors should be underweight bank stocks when the business cycle indicator declines, reflecting a weakening economy.

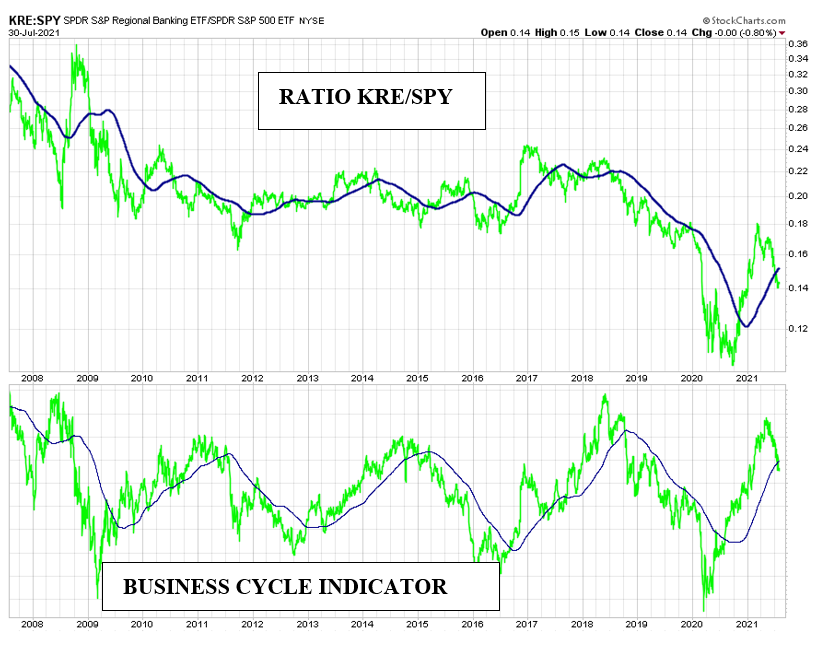

Do regional banks perform differently from financial and bank stocks?

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management

The upper panel of this chart shows the ratio of KRE (regional banks) and SPY. The chart shows regional banks become unattractive (the ratio declines) when the business cycle declines, reflecting a weakening economy.

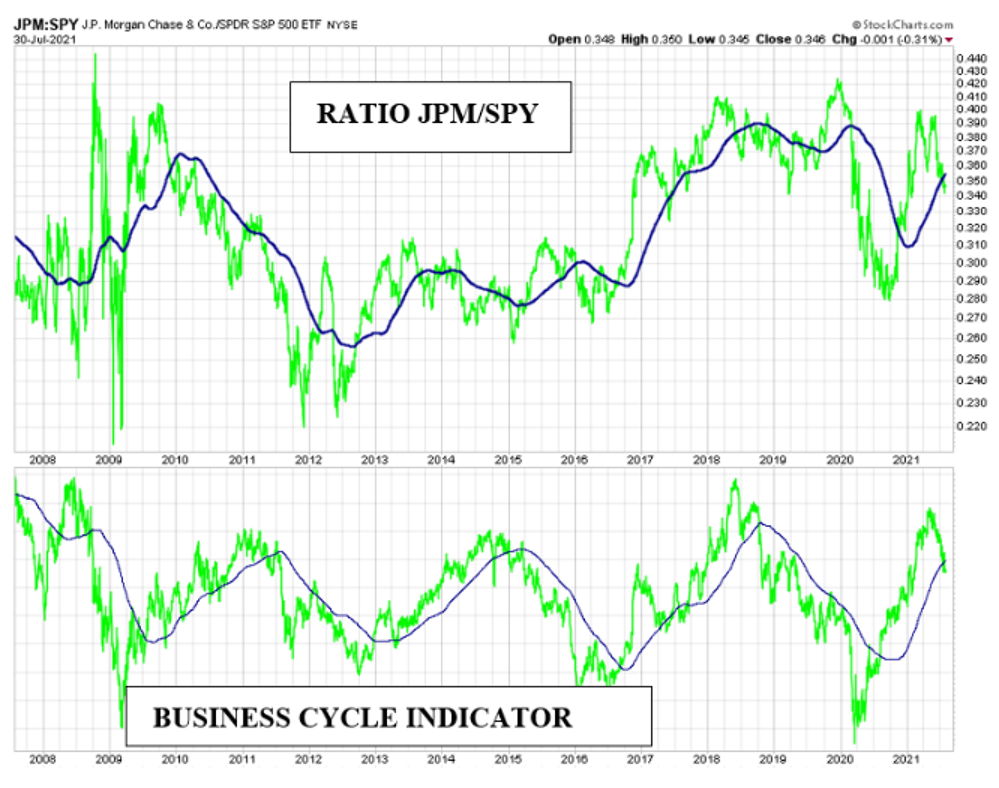

Are large money-center banks immune to the forces of the business cycle?

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management

The ratio of JPMorgan (NYSE: JPM) and SPY (upper panel) rises when the business cycle indicator (lower panel) rises, reflecting a strengthening economy. JPM underperforms SPY (the ratio declines) when the business cycle indicator declines, reflecting a weakening economy.

JPM, a major money center bank, is responding to changes of the business cycle like the overall financial stocks, bank stocks, and regional bank stocks (NYSEARCA: KRE).

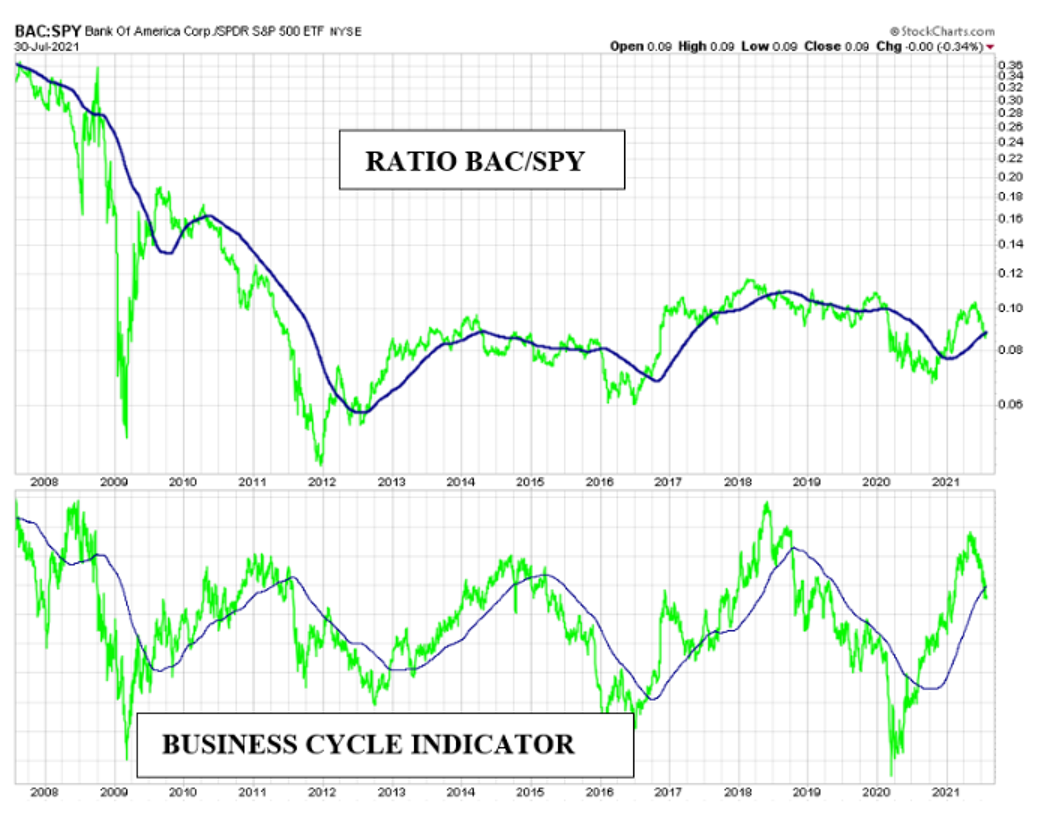

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management

Bank of America (NYSE: BAC) is also a money-center bank responding to the business cycle. The upper panel shows the ratio of BAC and SPY. BAC is also outperforming the market (NYSEARCA: SPY) when the business cycle rises. It underperforms the market when the business cycle declines, reflecting a weakening economy.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

Subscribe to ...

more