Economy Could Take Major Hit To Start 2021 Due To This

No Rent Payments

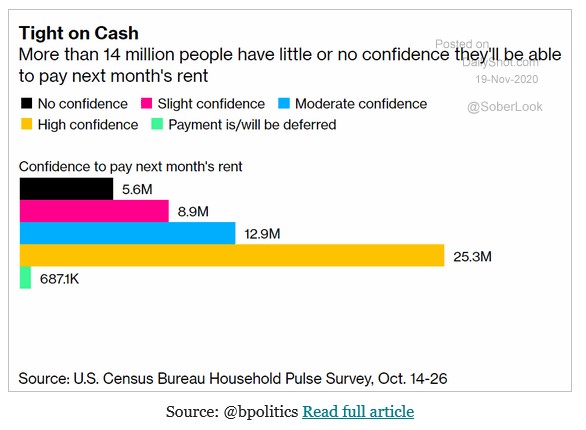

This current economy is rough for renters and great for single family home buyers. As you can see from the chart below, 14.5 million people either have no or slight confidence that they will have enough for rent next month. This survey was done from mid to late October. Imagine how much worse the data would be if this survey was taken 4 weeks later with COVID-19 worse and restrictions higher.

We Need Benefits To Be Extended

This recession accelerated the growing difference between the haves and have nots. It’s much tougher/impossible for low income people to work from home, while it’s easy for the upper middle class and rich to do so. The government absolutely needs to extend the pandemic benefits because if it doesn’t, it’s estimated that 12 million people could lose them.

If the government doesn’t proactively extend them, there won’t be benefits through January. Adding benefits in March is too little too late. As people get their jobs back, it would make sense to do another round of checks to make up for the losses this winter.

Merrill Lynch estimates the expiration of federal unemployment insurance programs, PUA and PUEC, alone will be a 1.5% drag on Q1 GDP growth. Economists are trying to figure out whether the slowdown will have more of a drag on Q4 or Q1. It doesn’t matter for traders. We know there is a small window of a couple of months where the pandemic related trends will accelerate before reversing starting in the spring.

While many wouldn’t go long the work from home stocks, we wouldn’t be surprised if they beat the reopening stocks in the next 6 weeks. It’s a battle because we will get bad news on COVID-19 and shutdowns, but we will get good vaccine news.

It’s pretty obvious to almost everyone that we need the pandemic benefits extended, but the government is dragging its feet. As you can see from the chart above, 68% of Americans stated a stimulus is needed as soon as possible. 11% said it is needed after the inauguration on January 20th. That’s too late.

Dual Georgia Senate runoff election will determine the balance of the Senate. Dems need to win both to tie the Senate. A tie is a win for the Dems because the Vice President is the tiebreaker. That election is on January 5th. Both elections are a toss-up. Some guess it will split, but we won’t get a good idea until there is more polling in December.

Mixed Economic Forecasts

There are mixed economic forecasts for the next few months. If you just take into account the latest data and markets, you will be optimistic, but if you assume COVID-19 hurts the economy and the vaccines don’t stop the spread soon, it’s clear that there will be a mini slowdown. JP Morgan is forecasting a 1% decline in Q1 GDP. They also see a quick recovery due to the vaccine as they predict 4.5% and 6.5% growth in Q2 and Q3.

Economists are wavering between whether the worst quarter of this slowdown will be Q4 or Q1. October was a decent month for the economy and November is looking ok. If only December is bad, Q1 growth might not be terrible. On the other hand, there will be no benefit from the vaccines.

Government agencies are stating vaccines could start going out in 8 weeks. January and February should have a lot of cases and shutdowns, but the vaccines should build up their impact throughout the quarter. March might have an economic rebound.

Atlanta Fed GDP Nowcast predicted 5.8% growth as of November 18th. That’s because October was a good month and early indications are that November wasn’t terrible. NY Fed weekly economic index in the week of November 14th improved from -2.96 to -2.84.

It was the slowest pace of improvement in 4 weeks. But the point here is the economy still improved in the first half of November. Through the 20th, we only have a “lockdown light.”

As you can see from the chart above, the ECRI weekly leading index’s growth rate improved in the week of November 13th. The index was up from 143.8 to 141.9 and the growth rate increased from 7.4% to 8.6%. It’s definitely helped by the stock market.

In October, the coincident index was up from 179.5 to 181.3 which pushed the growth rate up from -0.4% to 1.9% which further supports my point that October was a good month for the economy.

Self-Employment Recovers

In the past few months, we’ve seen the business applications index explode while the overall labor market struggled to get back to normal. The unemployment rate has fallen solidly, but the labor force participation rate is still down a lot from February. Because parts of the economy such as leisure and hospitality are still shuttered, we haven’t had a complete labor market recovery.

Those two trends have meant that self-employed job growth has recovered quicker than payroll employment growth. As you can see from the chart above, self-employed unincorporated jobs are about 2.5% off their pre-recession high, while payroll employment is off about 7% from before the recession. This might be because self-employed workers are more likely to work remotely which is good in this socially distanced economy.

Conclusion

14.5 million people are having trouble making rent and 12 million people are about to run out of unemployment benefits. The economy will probably be weak from December to February which might end up hurting Q1 more than Q4.

Work from home trade is back, but there is only a small window for it to work as the vaccines will be distributed to government agencies starting in 8 weeks. The economy might show significant improvement starting in March. Self-employment has recovered much quicker than payroll employment.

Disclaimer: Neither TheoTrade or any of its officers, directors, employees, other personnel, representatives, agents or independent contractors is, in such capacities, a licensed financial adviser, ...

more