Effective vaccines, historic fiscal stimulus, Democratic Party control of the legislature, even more stimulus, reopening economies, 6% U.S. real GDP (gross domestic product) growth, 25% U.S. EPS (earnings per share) growth, and maybe even an infrastructure plan sprinkled on top. On the surface that sounds like the perfect recipe for a bond market massacre. But levels matter A LOT for interest rates (I’ll explain). And U.S. Federal Reserve (the Fed) Chairman Jay Powell still has a very heavy hand to play in Treasury markets before a complete recovery is achieved.

The Fed will keep overnight interest rates at zero this year. That’s a slam dunk—or at least the closest thing to a slam dunk that my compliance department will allow me to commit to paper here. Millions of Americans remain out of work, inflation is below target and the Fed wants to engineer an inflation overshoot before liftoff. Our best guess is it will be early 2024 before all of these boxes for liftoff are checked.

Longer-term interest rates are, well, more interesting. That is because their pricing hinges on not only what the Fed is expected to do this year, but several years into the future as well. Our central tendency for the 10-year Treasury yield is between 1.1% and 1.6% at the end of 2021. That would only represent a modest lift in yields from current levels. Critical to this outcome is when inflationary pressures are likely to threaten on a sustained basis and, relatedly, how long the Fed intervenes in financial markets with their $120 billion per month of Treasury and mortgage-backed securities (MBS) purchases (quantitative easing).

Inflation is a lagging indicator and the Fed wants to generate a lot more of it

We’ve written a lot about the early recovery phase of the business cycle in terms of our equity strategy. The recovery phase tends to be a strong phase of the cycle for stocks because it is characterized by significantly above-trend growth. For bonds it is the level of economic activity (not the growth rate of economic activity) that matters more. That is because the level of economic activity is what drives inflationary dynamics and therefore how investors price a fixed stream of cash flows (i.e., a bond).

There are a lot of misconceptions about what actually causes inflation. Most of us learned about the hyperinflations of the Weimar Republic or Zimbabwe in our economics programs and therefore think money printing causes runaway inflation and currency debasement. Being an economist, I am of course the proud owner of a 100-trillion Zimbabwean dollar note, which is probably evidence enough that your professors weren’t totally wrong. But the reality of how inflation actually works is just a little bit more complicated.

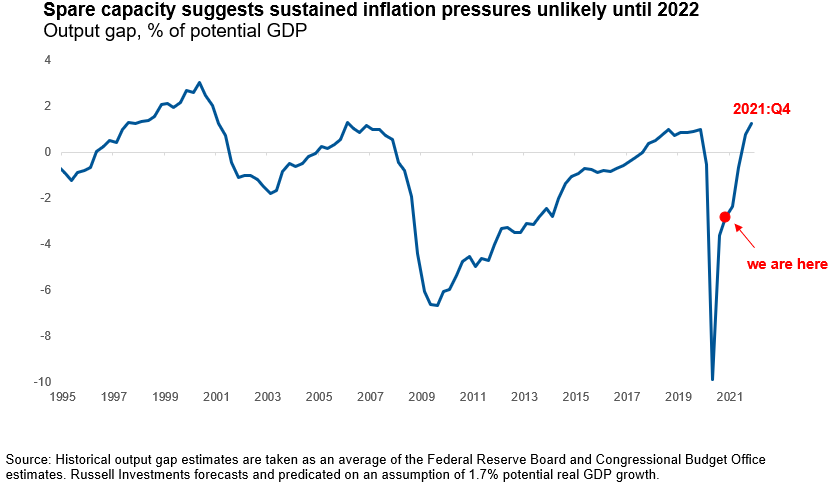

Inflation is really just a way of balancing supply and demand. If you tried to buy your child a PlayStation 5 for Christmas, you might’ve needed to shelve out multiples of the MSRP (manufacturer’s suggested retail price) to secure a unit on eBay, because there was just way too much demand relative to the available supply of consoles from Sony. That’s an example of inflation at a micro level. At a macro level, economists look for evidence that aggregate demand has pushed beyond the economy’s productive capacity (supply). Aggregate demand is a function of consumer, business and government spending (basically GDP). Aggregate supply is a function of the number and quality of people and machines to meet that demand. The chart below plots the output gap—a summary measure that compares current demand to potential supply.

(Click on image to enlarge)

When the line is above zero, inflationary pressures are building. When the line is below zero, disinflationary pressures dominate. And so the reason inflation rates were slowing in early 2020 or early 2009—when Fed chairs rolled out the printing press and Congress passed stimulus measures—was very simply a shortfall of aggregate demand. A lot of economists got this simple idea very wrong.

The bottom line: Persistent rise in inflation unlikely until next year

Today, even with historic stimulus and a partial economic recovery underway, aggregate demand (particularly for services) remains weak. The very strong growth that we expect in 2021 should help us climb out of this hole much faster than the post-GFC (Global Financial Crisis) experience. It’s worth noting that a short-term spike in inflation is possible later this year, as more COVID-19 restrictions are rolled back and pent-up consumer demand is unleashed. Chair Powell said as much at last week’s Fed policy meeting, stressing that any rapid bursts in inflation will be transient—and not long-lasting. We agree and believe that sustained inflationary pressures are unlikely until 2022 at the earliest.

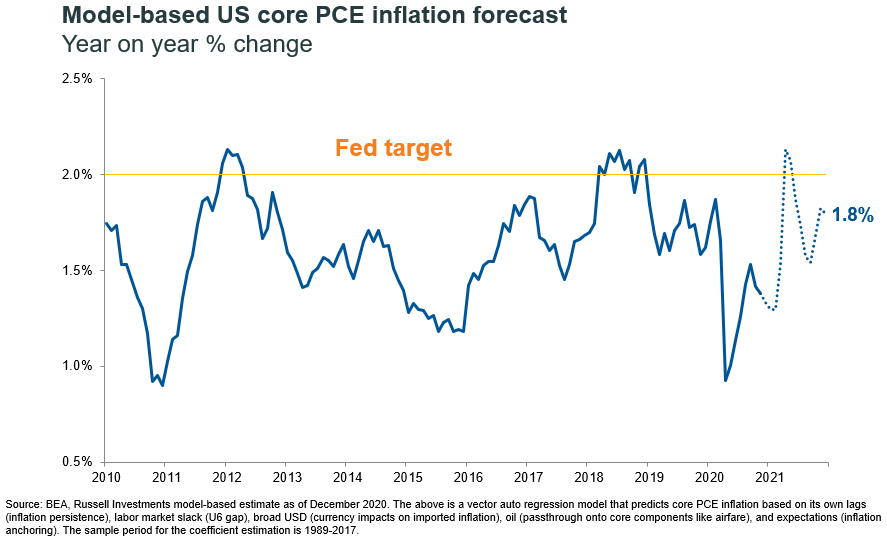

Our inflation model reflects this and only looks for core PCE (personal consumption expenditures) inflation—the Fed’s preferred measure—to reach 1.8% by year-end.

(Click on image to enlarge)

1.8% is below the Fed’s target. And inflation has been below target for the better part of the last decade. The Fed’s average inflation targeting framework is trying to engineer the opposite—an inflation overshoot—which should mean very accommodative policy for a lot longer.

Comments

Log in or sign up to join the conversation.