The Ultimate Financial Crisis Will Be Inflationary

I’ve read many comments to the effect that the next financial crisis will be like 2007-2008, only worse. However, the sole reason that many people are talking about a coming 2008-like crisis is because the happenings of 2008 are still fresh in the memory. Market participants often expect the next crisis to look like the last one, but it never does. Consequently, the general prediction about the next financial crisis with the highest probability of success is that it won’t be anything like 2008. It could, for example, revolve around an inflation scare rather than a deflation scare. In fact, the current monetary system’s ultimate financial crisis, meaning the crisis that leads to a new monetary system, will have to be inflationary.

The ultimate financial crisis will have to be inflationary, because deflation scares provide ‘justification’ for central bank money-pumping and thus enable the long-term credit expansion to continue with only minor interruptions. To put it another way, a crisis won’t be system-threatening as long as it can be ameliorated by central banks doing what they do best, which is promote inflation.

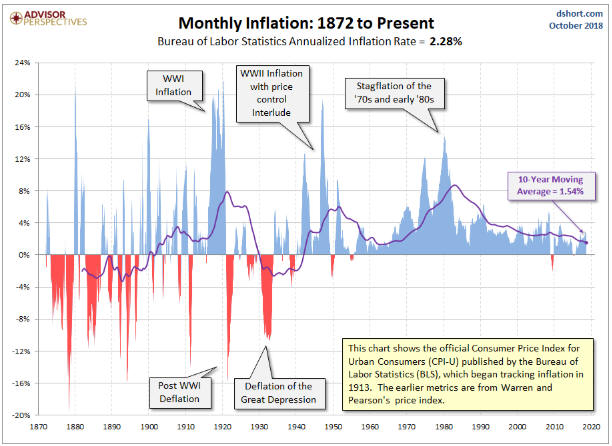

A related point is that a crisis won’t be system-threatening as long as it involves an increase in demand for the official money. The 2007-2008 crisis was such an animal. Like every other crisis in the US since 1940 it did not involve genuine deflation, almost regardless of how the word deflation is defined. The money supply continued to grow, the total supply of credit did no worse than flatten out, and, as illustrated by the following long-term chart, there was nothing more than a downward blip in the Consumer Price Index. However, with the stock market losing more than half its value and commodity prices collapsing, for 6-12 months it sure felt like deflation was happening.

Chart source: dshort

What actually happened during 2008 was a deflation scare, as opposed to genuine deflation. I define a deflation scare as a period when the total supply of money and credit continues to grow, but a surge in the demand for money makes it seem as if the economy is experiencing severe deflation.

Since there is no limit to the amount of new money and credit that can be created out of nothing by the central bank, it will always be possible for the central bank to keep the current system going in the face of a crisis that involves a surge in the demand to hold the official money. The problem (for the monetary authorities) will occur when the crisis involves a plunge in the demand for the official money. In such a situation the central bank’s most powerful weapon becomes not just ineffective, but counter-productive*.

The bottom line is that regardless of its other details, if the next crisis involves deflation or a deflation scare then it will be just another bump in the road. It will prompt another bout of aggressive money-pumping that will alleviate the perceived shortage of money and eventually inflate new investment bubbles. Only a crisis that entails a decline in the desire to hold the official money can be an existential threat to the monetary system.

*Creating money out of nothing is always counter-productive if the goal is to hasten long-term economic progress, but it can be productive if the goal is to prolong the existence of a debt-based monetary system.

Disclosure: None.