The Global Outlook Is Looking Slightly Less Gloomy

“Owing to a recent easing of both Sino-American tensions and monetary policies, many investors seem to be betting on another era of expansion for the global economy. But they would do well to remember that the fundamental risks to growth remain and are actually getting worse.”

(Nouriel Roubini, Project Syndicate, Nov. 20, 2019)

Pundits are currently somewhat more optimistic that the lengthy global economic recovery from the Great Recession, which ended in 2019, may have more legs.

The renewed optimism is partly based on strong equity markets, but also on the expectation that the global economic growth outlook for 2020 should be slightly stronger than this year’s slow growth.

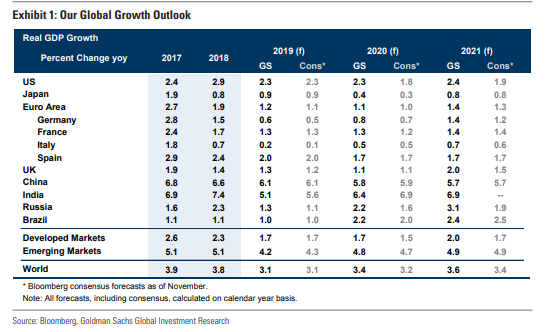

For example, according to the IMF, this year’s slow 3.2% global growth rate should be followed in 2020 with about 3.4% growth, and as well, the international pace of inflation should also increase next year. The Goldman Sachs global projections which are presented below are entirely consistent with this view.

As Roubini observes, the modest shift in the optimistic direction seems to hinge of four somewhat newer factors.

The first is a slight easing in the concern surrounding the US-China trade war, since it is assumed that a “phase-one” trade deal will be concluded this year, and which suggests that at least for a while there will not be a further escalation in the trade and technology war.

Second, markets are also hoping for a slightly improved outlook on the Brexit file. The assumption is that Boris Johnson will win the UK election and in turn should be able to achieve a rather softer Brexit deal with the EU. In other words, the UK will be able to avoid crashing disastrously out of the EU bloc. Avoiding a no deal Brexit would also boost European growth next year and in 2021.

In addition, on the economic policy side the key central banks - the US Federal Reserve, the European Central Bank, and the Bank of Japan -- have sharply eased on their monetary policies. Of course, widespread monetary easing has also boosted equity markets and market expectations.

Roubini’s fourth source of global risk reduction was the realization by the Trump Administration that oil prices would sharply escalate if the US responded aggressively to Iran’s provocations in the Middle East. The fact that Trump backed off is, of course, positive as well.

Obviously, the global economy still suffers from many potential risks which have not really gone away.

A successful China-US phase one deal cannot be fully counted on. Neither of course, can we assume that a soft Brexit solution will be realized. Moreover, the statistical odds associated with strong equity markets continuing on also cannot be counted on. Market participants who have any sense of history must worry that the US about to add another year to its longest economic expansion on record.

Nonetheless, if a soft landing does occur, among the advanced economies one should have the greatest confidence in the US economy. As long as the American economy is responsive to easy financial conditions, improved US growth would tend to spill over to all of the advanced economies.

The international soft-landing scenario also partly depends on the Brexit drag on the UK economy easing back a bit. As well there should be a economic gradual growth pickup in Europe in 2020 while Japan’s economy simply plods along very slowly. There is still the negative impact from Japan’s October consumption tax hike to work through on its economy.

China’s economy will continue to grow a bit slower in coming years, but on the positive side, we should recall that China’s economic policy levers work very positively and quickly on the domestic economy.

The following soft-landing global projections are taken from a recent Goldman Sachs report.

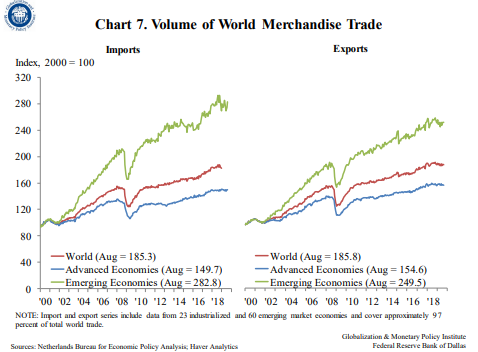

Indicators Of The Troubled Global Economic Outlook

(World Economic Growth Has Slowed. There Has Been A Significant Downshift In World Trade, Manufacturing And Services Production. Central Banks Have Vigorously Eased Their Policies In The Face Of The Slowdown.)