Image source: Pixabay

Most people believe members of the Federal Reserve are highly trained experts who are imminently qualified to run monetary policy. Guided by this perception, the mainstream treats Fed pronouncements as gospel. But if you compare Fed projections to actual outcomes, it looks like they’re just guessing. In fact, you would probably get more accurate results throwing darts at a dartboard.

Now, it may seem a little presumptuous for me to question the knowledge of these highly trained economists. I mean, they have that job and I’m over here writing articles. But think about how wrong these people have been.

We all remember “transitory” inflation.

Surprise!

Fast-forward 18 months and “transitory” has morphed into “sticky” and “persistent.”

If Fed members’ jobs depended on them being right, the whole lot of them would be in the unemployment line.

And that’s not the only recent Fed projection that was wildly wrong.

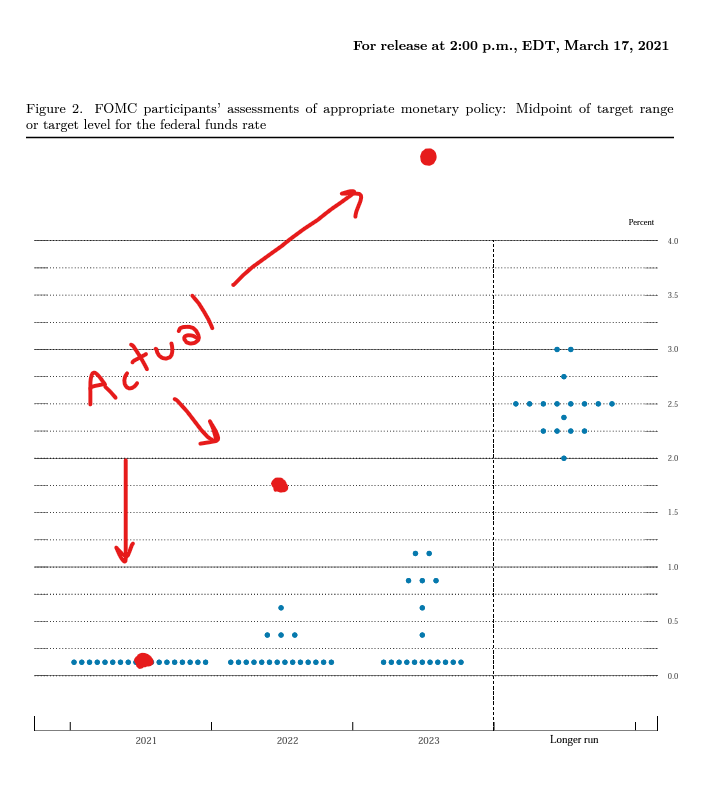

In March 2021, the Federal Open Market Committee (FOMC) released a “dot plot” projecting the trajectory of interest rates over the following several years.

Their guesses weren’t even in the ballpark.

As you can see from the dot plot, most of the FOMC members thought interest rates would still be at zero in 2022. A couple of members predicted a quarter percent, and one said half a percent.

The actual 2022 rate was 1.75%.

In 2023, the vast majority of FOMC members thought the rate would still be zero percent. Two projected it would rise to 1% and there were five who said it would be between a quarter percent and three-quarter percent. The actual rate – over 5%. As you can see, the actual rate doesn’t even fit on the dot-plot graph.

They also have a category they called “longer run.” The highest anybody on the FOMC saw rates climbing in the long-term was 3%. The vast majority were locked in at 2.5%.

The FOMC released a new dot plot after the June meeting, projecting that rates would climb even higher than recently anticipated, and that they would stay higher longer.

During the post-meeting press conference, Powell doubled down on the hawkishness, saying he doesn’t see rate cuts in the near future, and perhaps not for years.

It will be appropriate to cut rates at such time as inflation is coming down really significantly. And again, we’re talking about a couple of years out. As anyone can see, not a single person on the committee wrote down a rate cut this year, nor do I think it is at all likely to be appropriate.”

If I were you, I’d throw that dot plot in the garbage.

According to fund manager David Hay, the Fed has only gotten interest rate projections right 37% of the time. And as Hay pointed out, “They control interest rates!”

I think it’s far more likely that rates are zero in two years than 2 or 3%.

This is just one example of how horribly wrong the Fed has been. I can cite other examples.

Remember back in 2006 when the central bankers insisted there was no housing bubble? Then when things started to unravel, they promised the problem was contained to subprime.

In 2008, Ben Bernanke launched quantitative easing and swore that it wasn’t debt monetization. He said the Fed would sell all of the bonds it planned to buy once the emergency was over. Today, virtually all of those bonds remain on the Fed’s balance sheet.

In 2018, the Fed finally started to tighten monetary policy after a decade of easy money in the wake of the Great Recession. Fed officials said balance sheet reduction was “on autopilot.” By the end of 2019, the central bank was already expanding its balance sheet — prior to the pandemic.

It’s almost like the Fed people are wrong about everything.

Perhaps the Fed should go ahead and invest in that dartboard.

More By This Author:

Eight Central Banks Increased Gold Holdings In MayFed People Saying Stuff

An Amazing Freak Show: Treasury Increases National Debt By Over $850 Billion in Just One Month

Comments

Log in or sign up to join the conversation.