In broad brush, central banks got away with the illusion of permanently low inflation even as they pumped trillions in new currency into the global economy for one reason: China. It is useful to think of China in the early-to-mid 1990s as a system of vast, interconnected, untapped pools of:

1. Cheap labor just awaiting exploitation by global corporations, local entrepreneurs and state entities

2. Ambition, drive and long-frustrated desires for improved opportunities for individual/family betterment

3. Need for capital/credit to build a modern economy and infrastructure

4. Potential for national issuance of currency and credit on an unimaginably large scale

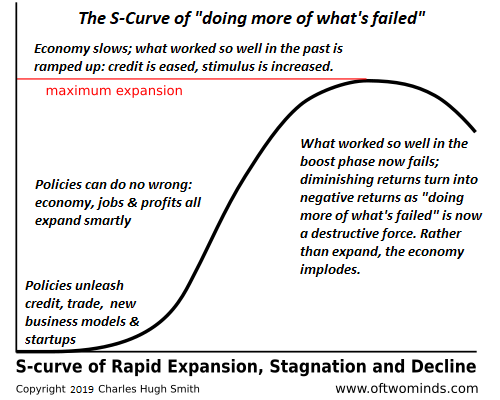

All four pools were tapped at ever larger scales over the past 30 years, enabling China to deflate the cost of good globally as "the workshop of the world." All else being equal, issuing unprecedented quantities of currency and credit, both public and private, typically boosts consumption and production in the early "boost phase" of the S-Curve. But once the most productive uses of credit are satiated, the new money flows into unproductive speculation and financial skimming operations.

At that point, all the new money flooding into the system drives inflation, a trend reinforced by the depletion of all the cheap pools of labor and easiest-to-exploit materials.

The pool of cheap, abundant Chinese labor has been completely drained. Wages in China have soared, along with inflation, and demographics is shrinking the labor pool even as the high expectations generated by 30 years of rapid expansion have diminished the labor force's willingness to perform low-paid factory work far from home and family.

China's economy is now beset with the inevitable downside of the S-Curve. Pouring more new money into an economy that is inflating speculative bubbles with the money doesn't create productive uses for the new credit; it simply encourages the perverse incentives to speculate and skim.

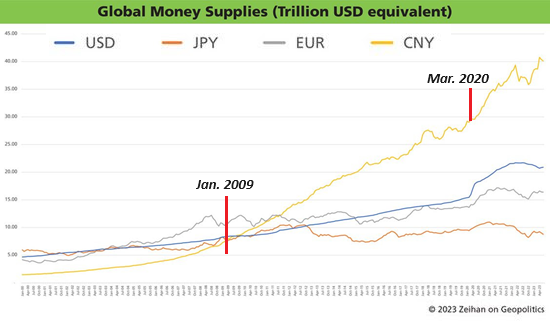

China is not alone in boosting its money supply and debt, but it is the current leader, whose gigantic expansion of credit bailed out the Chinese and global economy in 2009 and again in 2020. But that mechanism is now crippled by diminishing returns; inflating the money supply, borrowing trillions to fund deficit fiscal spending and expanding private credit to fund student loans, auto loans and bloated mortgages globally is no longer creating growth--it's creating inflation and the permanent drag of higher debt service.

If excesses pop a few of the planet's proliferating speculative asset bubbles, we'll discover that deflation in overvalued assets won't translate into lower-real-world inflation of goods and services, which depend on the costs of labor, capital and risk, all of which are rising in long-overdue turns of cycles.

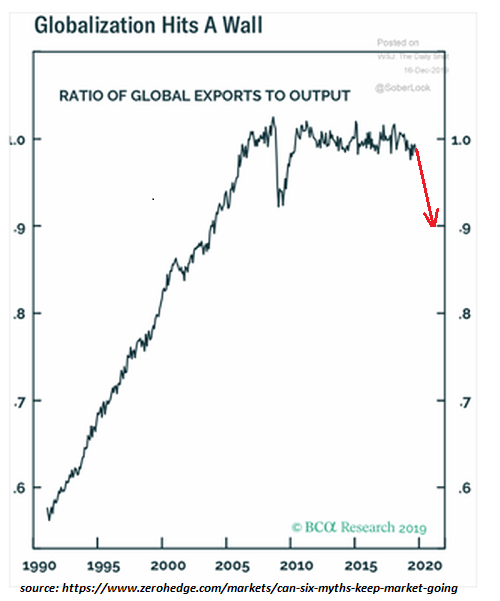

Meanwhile, for a variety of well-known reasons, globalization as a source of deflation has run its course and is no longer able to offset inflation in either China or the nations importing Chinese goods globally. Wages in the US have been suppressed for 45 years in favor of capital and financiers, and now the pendulum is swinging to higher wages for demographic, financial and political reasons.

Reshoring, friend-shoring, building redundant supply chains, securing national-security sources of minerals and energy--every one of these costs far more than the supply chains being replaced, not just initially, but into the future.

With China as a global deflator now a spent force, inflation will not drop to 2% and linger there indefinitely. All the currency and credit flooding into the global economy while production, quality and quantity all stagnate or collapse will fuel inflation.

All those counting on AI to magically boost productivity globally on a scale large enough to counter the tsunami of new currency and credit being issued to "bring demand forward" will be disappointed. When consumers run out of credit, the profit spigot dries up, AI or no AI. When higher debt payments suck companies and government entities dry, adding more currency and debt isn't a solution, it becomes the problem.

Where is the global deflator expansive enough to replace China's one-off deflation of global inflationary forces? There isn't one, and those counting on AI are forgetting that right now AI is a bottomless sinkhole of corporate spending, as CEOs are just as motivated by fads and the crowd as any clueless consumer. Most of the billions being dumped into AI projects will return nothing in the way of higher productivity or profits because AI is already a commodity.

Sure, inflation may well drop for a time as consumers rein in spending, but the "solution"--the accelerating issuance of more currency and debt--will only fuel inflation. The decades-long swing of the deflationary zero-interest rate pendulum has ended, and the swing to higher interest rates and higher inflation will only gather momentum in the decade ahead.

More By This Author:

What The Fed Accomplished: Distorted The Economy, Enriched The Rich And Crushed The Middle Class2023: The Fed Declares Victory; 2024: The Year Of Hubris And Nemesis

What If There Are No Analogs For 2024?

Comments

Log in or sign up to join the conversation.