Tax Cuts & The Failure To Change The Economic Balance

As we approach “tax day” in the U.S., I wanted to take a moment to revisit the issue of taxes, who pays what, and why the “Tax Cut and Jobs Act” will likely have limited impact on economic growth.

This week, Laura Saunders penned for the WSJ an analysis of “who pays what” under the U.S. progressive tax system. The data she used was from the Tax Policy center which divided about 175 million American households into five income tiers of roughly 65 million people each. This article was widely discussed on radio shows across the country as “clear evidence” recent tax reform was having a “huge effect” on average households and a clear step in “Making America Great Again.”

The reality, however, is far different than the politically driven spin.

First, the data.

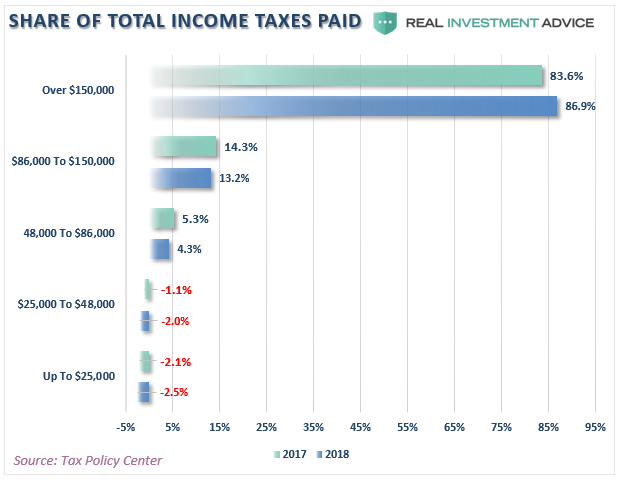

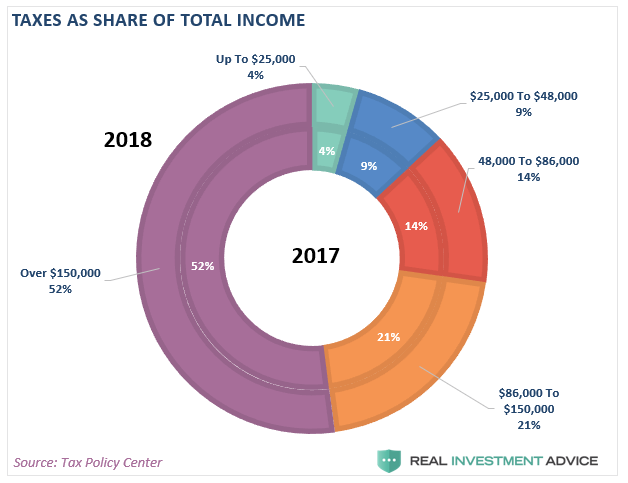

“The results show how steeply progressive the U.S. income tax remains. For 2018, households in the top 20% will have income of about $150,000 or more and 52% of total income, about the same as in 2017. But they will pay about 87% of income taxes, up from about 84% last year.”

See, the “rich” are clearly paying more.

Not really, percentages are very deceiving. If the total amount of revenue being collected is reduced, the purpose of a tax cut, the top 20% can pay LESS in actual dollars, but MORE in terms of percentage. For example:

- Year 1: Top 20% pays $84 of $100 collected = 84%

- Year 2: Top 20% pays $78 of $90 collected = 87%

This is how “less” equals “more.”

So, where is the “less?”

“By contrast, the lower 60% of households, who have income up to about $86,000, receive about 27% of income. As a group, this tier will pay no net federal income tax in 2018 vs. 2% of it last year.”

“Roughly one million households in the top 1% will pay for 43% of income tax, up from 38% in 2017. These filers earn above about $730,000.”

While the “percentage or share” of the total will rise for the top 5%, the total amount of taxes estimated to be collected will fall by more than $1 Trillion for 2018. As Roberton Williams, an income-tax specialist with the Tax Policy Center, noted while the share of taxes paid by the top 5% will rise, the people in the top 5% were the largest beneficiaries of the overhaul’s tax cut, both in dollars and percentages.

Not surprisingly, as I noted previously, income taxes for the bottom 2-tiers of income earners, or roughly 77-million households, will have a negative income tax rate. Why? Because, despite the fact they pay ZERO in income taxes, Congress has chosen to funnel benefits for lower earners through the income tax rather than other channels such as federal programs. Since the recent tax legislation nearly doubled the standard deduction and expanded tax credits, it further lowered the share of income tax for people in those tiers.

The 80/20 Rule

In order for tax cuts to truly be effective, given roughly 70% of the economy is driven by personal consumption, the amount of disposable incomes available to individuals must increase to expand consumption further.

Since more than 80% of income taxes are paid by the top 20%, the reality is tax cuts only have a limited impact on consumption for those individuals as they are already consuming at a level with which they are satisfied.

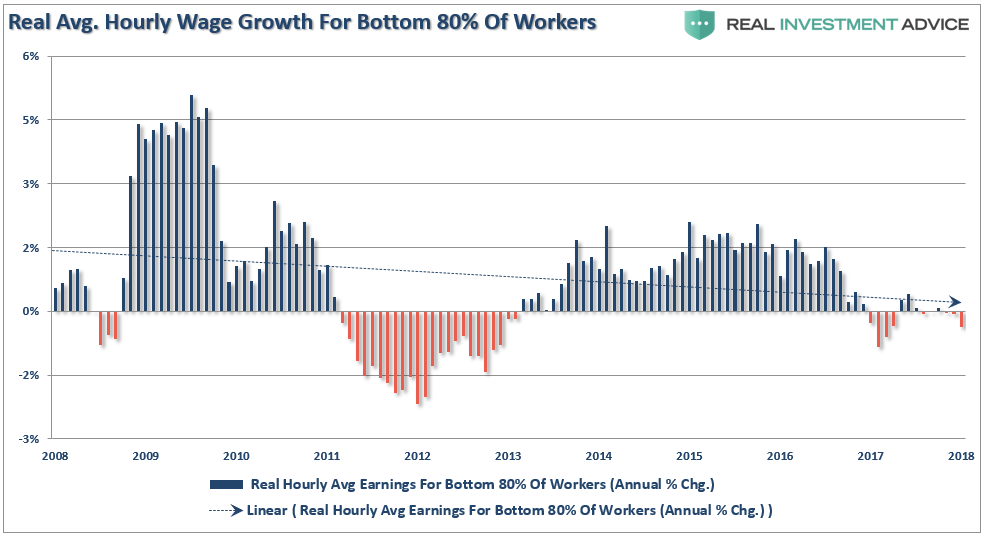

The real problem is the bottom 80% that pay 20% of the taxes. As I have detailed previously, the vast majority of Americans are living paycheck to paycheck. According to CNN, almost six out of every ten Americans do not have enough money saved to even cover a $500 emergency expense. That lack of savings can be directly attributed to the lack of income growth for those in the bottom 80% of income earners.

(Click on image to enlarge)

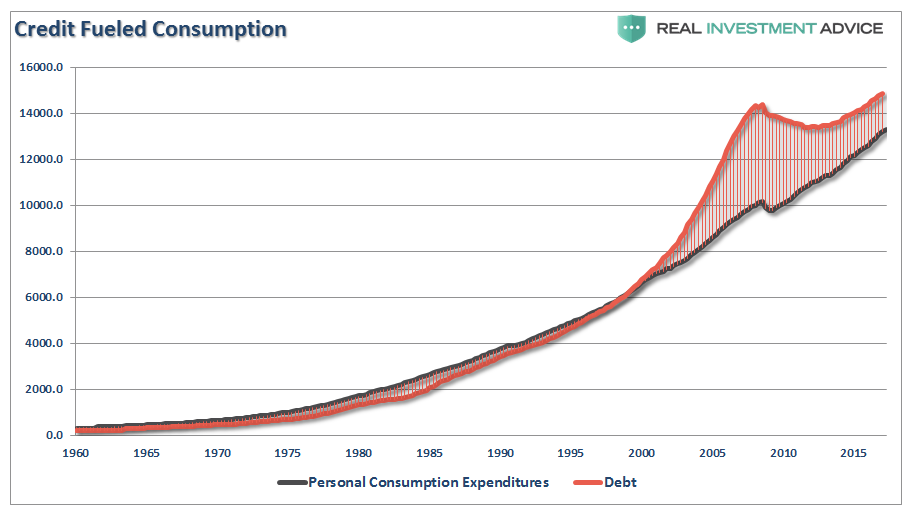

So, with 80% of Americans living paycheck-to-paycheck, the need to supplant debt to maintain the standard of living has led to interest payments consuming a bulk of actual disposable income. The chart below shows that beginning in 2000, debt exceeded personal consumption expenditures for the first time in history. Therefore, any tax relief will most likely evaporate into the maintaining the current cost of living and debt service which will have an extremely limited, if any, impact on fostering a higher level of consumption in the economy.

(Click on image to enlarge)

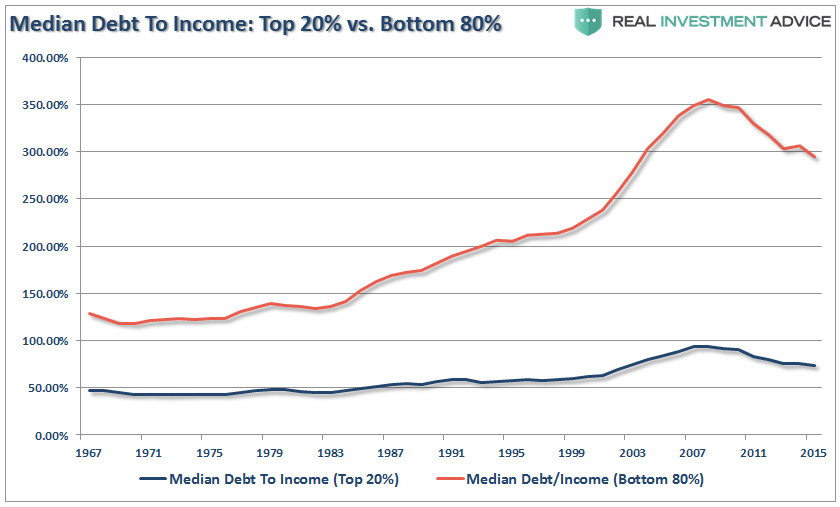

But again, there is a vast difference between the level of indebtedness (per household) for those in the bottom 80% versus those in the top 20%.

(Click on image to enlarge)

The rise in the cost of living has outpaced income growth over the past 14 years. While median household incomes may have grown over the last couple of years, expenses have outpaced that growth significantly. As Stephanie Pomboy recently stated:

” In January, the savings rate went from 2.5% to 3.2% in one month—a massive increase. People look at the headline for spending and acknowledge that it’s not fabulous, but they see it as a sustainable formula for growth that will generate the earnings necessary to validate asset price levels.”

Unfortunately, the headline spending numbers are actually far more disturbing once you dig into “where” consumers are spending their dollars. As Stephanie goes on to state:

“When you go through that kind of detail, you discover that they are buying more because they have to. They are spending more on food, energy, healthcare, housing, all the nondiscretionary stuff, and relying on credit and dis-saving [to pay for it]. Consumers have had to draw down whatever savings they amassed after the crisis and run up credit-card debt to keep up with the basic necessities of life.”

When a bulk of incomes are diverted to areas which must be purchased, there is very little of a “multiplier effect” through the economy and spending on discretionary products or services becomes restricted. This problem is magnified when the Fed hikes short-term interest rates, which increases debt payments, and an Administration engages in a “trade war” which increases prices of purchased goods.

Higher costs and stagnant wages are not a good economic mix.

The Corporate Tax Cut Sham

But this was never actually a “tax cut for the middle-class.”

The entire piece of legislation was a corporate lobby-group inspired “give away” disguised as a piece of tax reform legislation. A total sham.

Why do I say that? Simple.

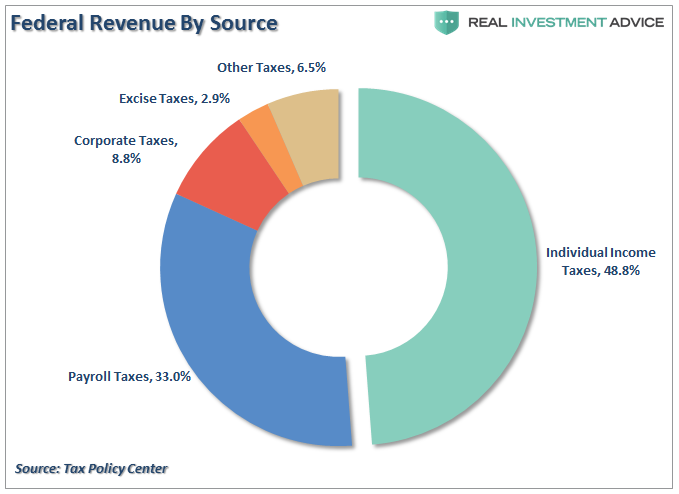

If the Administration were truly interested in a tax cut for the middle class, every piece of the legislation would have been focused on the nearly 80% of Federal revenue collected from individual income and payroll taxes.

Instead, the bulk of the “tax reform” plan focused on the 8.8% of total Federal revenue collected from corporate taxes.

“But business owners and CEO’s will use their windfall to boost wages and increase productivity. Right?”

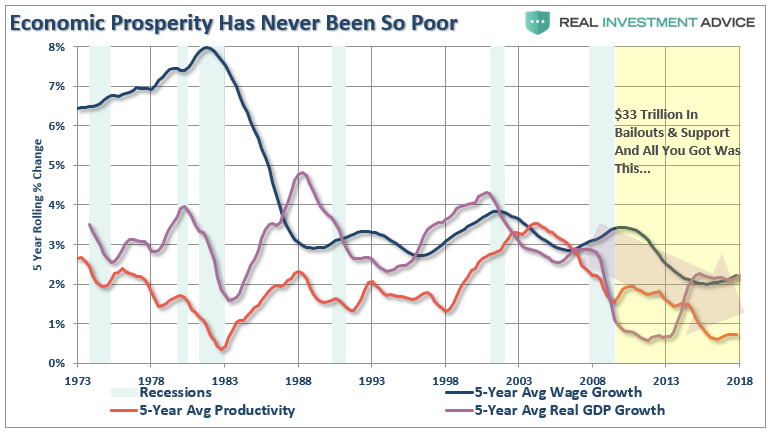

As I showed previously, there is simply no historical evidence to support that claim.

(Click on image to enlarge)

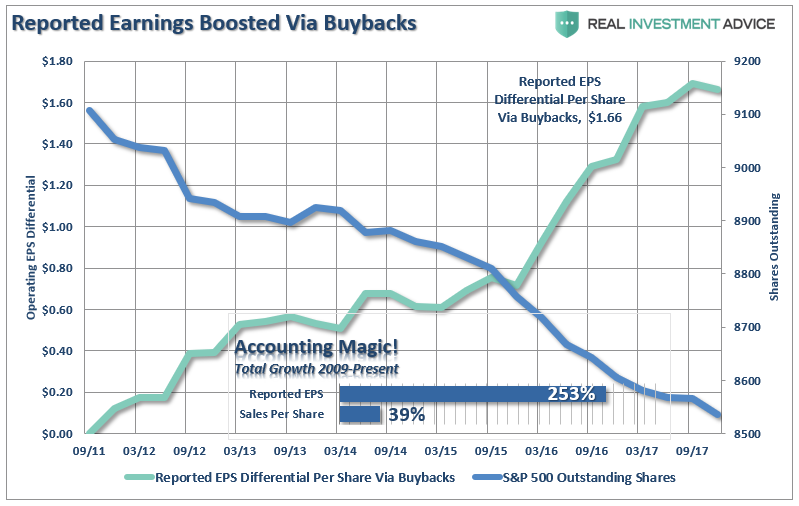

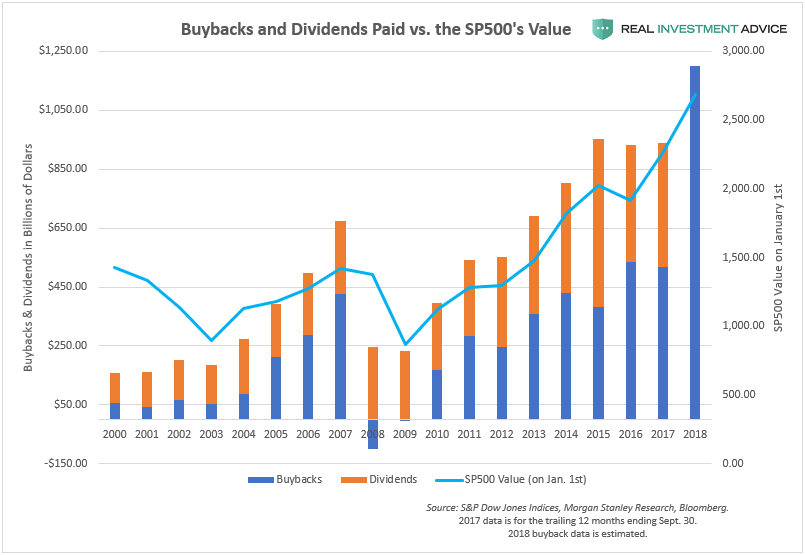

Corporations are thrilled with the bill because corporate tax cuts immediately drop to the bottom lines of the income statement. With revenue growth, as shown below, running at exceptionally weak levels, corporations continue to opt for share buybacks, wage suppression and accounting gimmicks to fuel bottom lines earnings per share. The requirement to meet Wall Street expectations to support share prices is more important to the “C-suite” executives than being benevolent to the working class.

(Click on image to enlarge)

“Not surprisingly, our guess that corporations would utilize the benefits of ‘tax cuts’ to boost bottom line earnings rather than increase wages has turned out to be true. As noted by Axios, in just the first two months of this year companies have already announced over $173 BILLION in stock buybacks. This is ‘financial engineering gone mad.’”

(Click on image to enlarge)

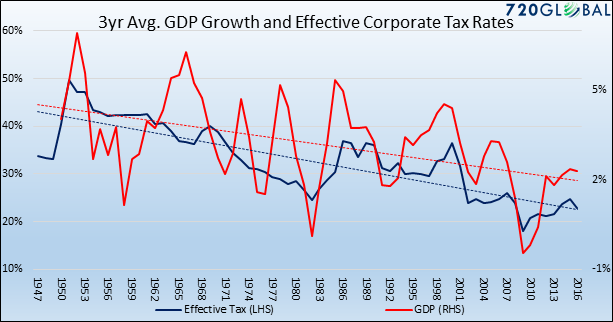

The historical evidence provides a very different story than the bill of goods being sold to citizens and investors. There is no historical evidence that cutting corporate tax rates increases economic growth. In fact, as recently noted by Michael Lebowitz, the opposite has been true with high correlation between lower tax rates and slower economic growth.

With the deficit set to exceed $1 Trillion next year, and every year afterward, the government must borrow money to fund the shortfall. This borrowing effectively crowds out investment that could have funded the real economy.

“Said differently, the money required to fund the government’s deficit cannot be invested in the pursuit of innovation, improving workers skills, or other investments that pay economic dividends in the future. As we have discussed on numerous occasions, productivity growth drives economic growth over the longer term. Therefore, a lack productivity growth slows economic growth and ultimately weighs on corporate earnings.

A second consideration is that the long-term trend lower in the effective corporate tax has also been funded in part with personal tax receipts. In 1947, total personal taxes receipts were about twice that of corporate tax receipts. Currently, they are about four times larger. The current tax reform bill continues this trend as individuals in aggregate will pay more in taxes.

As personal taxes increase, consumers who account for approximately 70% of economic activity, have less money to spend.”

Summary

This issue of whether tax cuts lead to economic growth was examined in a 2014 study by William Gale and Andrew Samwick:

“The argument that income tax cuts raise growth is repeated so often that it is sometimes taken as gospel. However, theory, evidence, and simulation studies tell a different and more complicated story. Tax cuts offer the potential to raise economic growth by improving incentives to work, save, and invest. But they also create income effects that reduce the need to engage in productive economic activity, and they may subsidize old capital, which provides windfall gains to asset holders that undermine incentives for new activity.

In addition, tax cuts as a stand-alone policy (that is, not accompanied by spending cuts) will typically raise the federal budget deficit. The increase in the deficit will reduce national saving — and with it, the capital stock owned by Americans and future national income — and raise interest rates, which will negatively affect investment. The net effect of the tax cuts on growth is thus theoretically uncertain and depends on both the structure of the tax cut itself and the timing and structure of its financing.”

Again, the timing is not advantageous, the economic dynamics and the structure of the tax cuts are not self-supporting. As Dr. Lacy Hunt recently noted in his quarterly outlook:

“Considering the current public and private debt overhang, tax reductions are not likely to be as successful as the much larger tax cuts were for Presidents Ronald Reagan and George W. Bush. Gross federal debt now stands at 105.5% of GDP, compared with 31.7% and 57.0%, respectively, when the 1981 and 2002 tax laws were implemented.

However, if the household and corporate tax reductions and infrastructure tax credits proposed are not financed by other budget offsets, history suggests they will be met with little or no success.”

Since the current Administration has chosen to do the exact opposite by massively increasing spending, having no budget offsets, or slowing the rate of growth of either deficits or debts, the success of tax reform to boost economic growth is highly suspect.

Policymakers had the opportunity to pass true, pro-growth, tax reform and show they were serious about our nations fiscal future, they instead opted to continue enriching the top 1% at the expense of empowering the middle class.

The outcome will be very disappointing.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more