Economists were focused on three facets of the U.S. Federal Reserve (the Fed)’s meeting today. Importantly, none of these three outcomes were particularly consequential for investors.

1. New forward guidance

Would the Fed clarify its forward guidance on interest rates following Powell’s announcement at the annual Jackson Hole, Wyoming, economic symposium about the transition to a new average inflation targeting (AIT) framework?

As a reminder, AIT is basically a commitment to keep interest rates lower for longer, allowing inflation to overshoot the 2% objective for a time to compensate for undershoots that normally occur during recessions and the early years of an economic recovery. The Fed did enhance its forward guidance today, committing to keep interest rates at zero until the U.S. economy reaches full employment, and “inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

Put differently, the Fed has pinned liftoff to an economic outcome, namely that inflation must hit its 2% objective and be expected to exceed it for some time. No major surprises here, although some economists did not think the Fed would be able to agree on this new language until the November meeting.

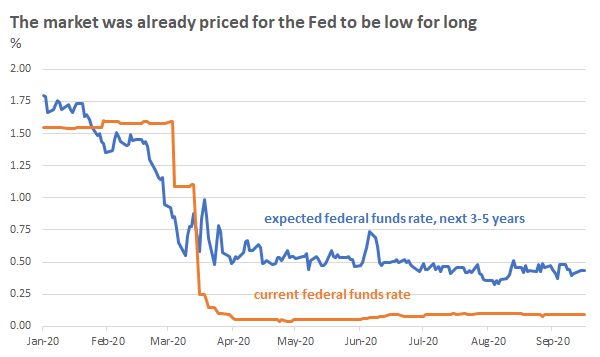

2. Interest rate forecasts for 2023

Would the Fed show any rate hikes in its updated forecasts, which now include the central bank’s expectations for 2023 for the first time?

13 out of the 17 Federal Open Market Committee (FOMC) participants penciled the federal funds rate to remain at the zero bound through the end of 2023 under their baseline outlook. While this is a dovish statement on the surface, it will not have been very surprising to professional investors given fixed income markets were already priced to the floor with only one quarter-point rate hike expected from the Fed over the next five years (chart). This pricing did not move much in the 30 minutes around the announcement.

(Click on image to enlarge)

Source: Thomson Reuters Datastream, Russell Investments calculations as of 11:30 a.m. Pacific time on September 16, 2020.

3. Asset purchases

Would the Fed change the average maturity of its asset purchases to focus more on longer-term bonds?

The Federal Reserve’s quantitative easing (QE) program to-date has bought Treasury securities across the Treasury curve. There is a view in the market—with short-term rates already glued to the floor—that the Fed could get more bang for the buck in terms of easing financial conditions by purchasing more duration from the market. Chair Jerome Powell did not go there today.

If we were to try to unpack why the FOMC did not do so, it is probably because they see too much uncertainty in the economic outlook from the virus to be that precise OR that they view the prevailing level of long-term rates as already being sufficiently accommodative.

Rate and market outlook

The path forward largely hinges on the medium-term outlook for U.S. inflation. As we’ve written about, inflationary pressures are normally a consequence of an economy having more aggregate demand for goods and services than its productive capacity can handle. Given COVID-19 drove a recession and a shortfall in aggregate demand, we do not see upside risks to inflation as being a major concern for at least the next one to two years.

Put differently, there is still a hole for the economy to climb out of before the output gap (economist lingo) closes. In our most bullish scenario for the economy (reflecting on the historic levels of fiscal stimulus, the natural disaster nature of the COVID-19 shock, and the better-than-expected economic news in recent months), we see rate hikes as being possible in late 2022. However, our central tendency is similar to the Fed’s, with it being much more likely that the central bank remains on hold through 2023 before inflationary pressures start showing an overshoot.

Zooming in on the next 12 months, in particular, we think the Fed is all but certain to hold interest rates near zero and, contingent on positive vaccine news, we see potential for the 10-year Treasury yield to rise modestly to 1%—resulting in a modest steepening of the yield curve. If this view is correct, it could contribute to a rotation from longer-duration growth stocks to shorter-duration value stocks.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and ...

more

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

Investing involves risk and principal loss is possible.

Past performance does not guarantee future performance.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk. Although steps can be taken to help reduce risk it cannot be completely removed. They do no not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors, and size of companies preferred by the investment managers. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Please see a prospectus for further details.

Indexes are unmanaged and cannot be invested in directly.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments' management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

Copyright © Russell Investments Group LLC 2020. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-11741

Disclaimer: Opinions expressed by readers don’t necessarily represent Russell’s views. Links to external web sites may contain information concerning investments other than those offered by Russell Investments, its affiliates or subsidiaries. Neither Russell Investments nor its affiliates are responsible for investment decisions with respect to such investments or for the accuracy or completeness of information about such investments. Descriptions of, references to, or links to products or publications within any linked web site does not imply endorsement of that product or publication by Russell Investments. Any opinions or recommendations expressed are solely those of the independent providers and are not the opinions or recommendations of Russell Investments, which is not responsible for any inaccuracies or errors.

Investing in capital markets involves risk, principal loss is possible. There is no guarantee the stated outcomes in the presentation will be met.

This is a publication of Russell Investments. Nothing in this publication is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The contents in this publication are intended for general information purposes only and should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional concerning your own situation and any specific investment questions you may have.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

less

How did you like this article? Let us know so we can better customize your reading experience.