NFIB Survey Trips Economic Alarms

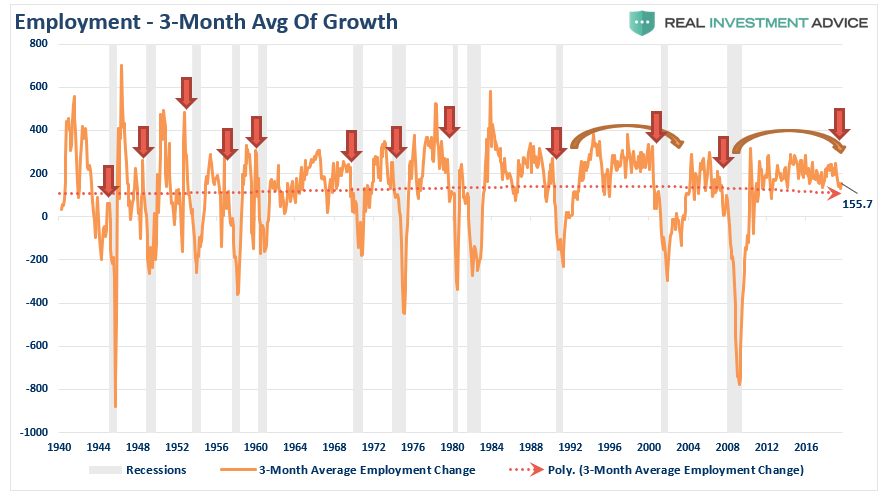

Last week, I wrote an article discussing the August employment report, which clearly showed a slowdown in employment activity and an overall deterioration the trend of the data. To wit:

“While the recent employment report was slightly below expectations, the annual rate of growth is slowing at a faster pace. Therefore, by applying a 3-month average of the seasonally-adjusted employment report, we see the slowdown more clearly.”

I want to follow that report up with analysis from the latest National Federation of Independent Businesses monthly Small Business Survey. While the mainstream media overlooks this data, it really shouldn’t be.

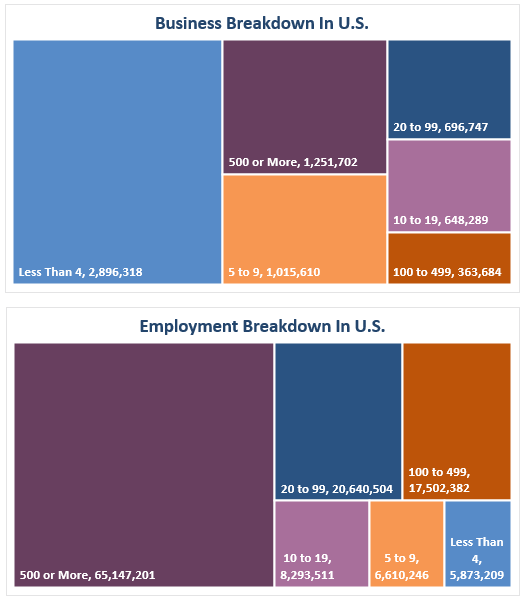

There are 28.8 million small businesses in the United States, according to the U.S. Small Business Administration, and they have 56.8 million employees. Small businesses (defined as businesses with fewer than 500 employees) account for 99.7% of all business in the U.S. The chart below shows the breakdown of firms and employment from the 2016 Census Bureau Data.

Simply, it is small businesses that drive the economy, employment, and wages. Therefore, what the NFIB says is extremely relevant to what is happening in the actual economy versus the headline economic data from Government sources.

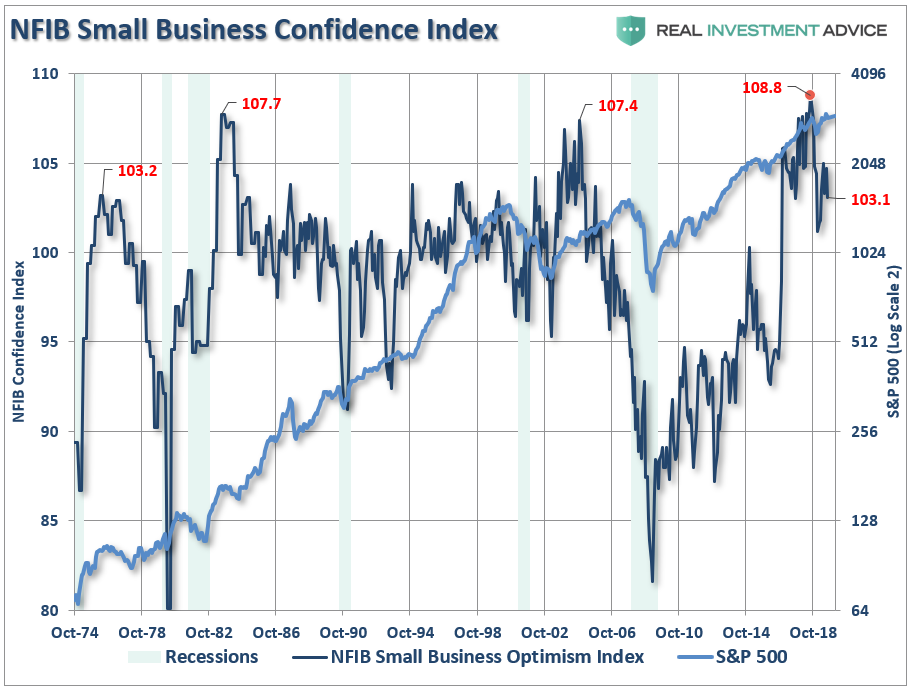

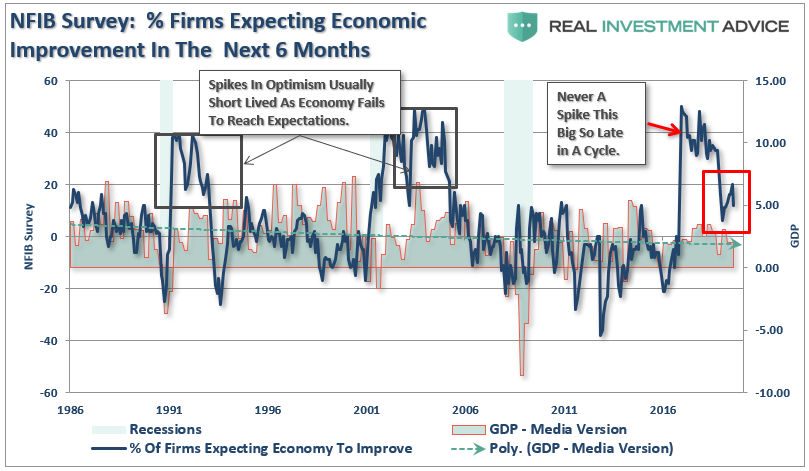

In August, the survey declined 1.6 points to 103.1. While that may not sound like much, it is where the deterioration occurred that is most important.

As I discussed previously, when the index hit its record high:

“Record levels of anything are records for a reason. It is where the point where previous limits were reached. Therefore, when a ‘record level’ is reached, it is NOT THE BEGINNING, but rather an indication of the MATURITY of a cycle.”

That point of “exuberance” was the peak.

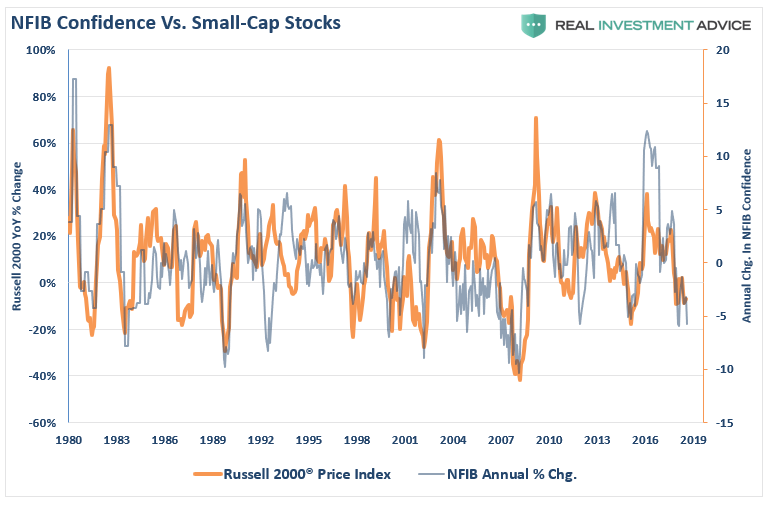

It is also important to note that small business confidence is highly correlated to changes in, not surprisingly, small-capitalization stocks.

The stock market, and the NFIB report, confirm risk is rising. As noted by the NFIB:

“The Uncertainty Index rose four points in August, suggesting that small business owners are reluctant to make major spending commitments.”

Before we dig into the details, let me remind you this is a “sentiment” based survey. This is a crucial concept to understand.

“Planning” to do something is a far different factor than actually “doing” it.

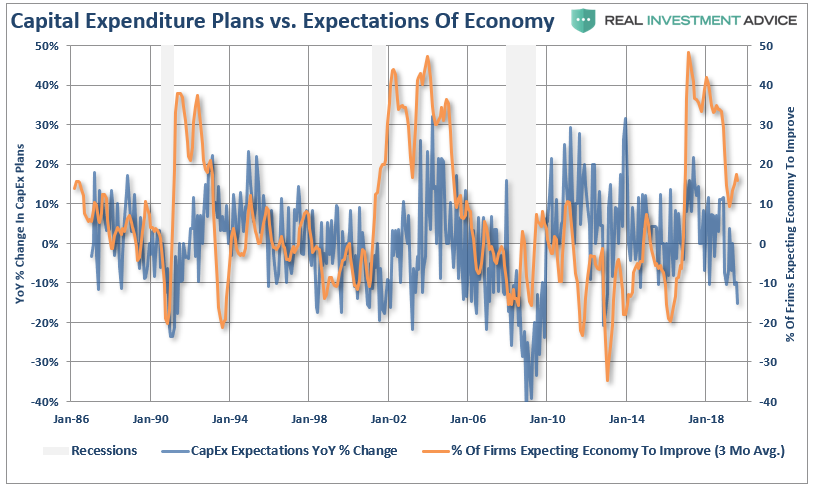

For example, the survey stated that 28% of business owners are “planning” capital outlays in the next few months. That’s sounds very positive until you look at the trend which has been negative. In other words, “plans” can change very quickly.

This is especially the case when you compare their “plans” to the outlook for economic growth.

The “Trump” boom appears to have run its course.

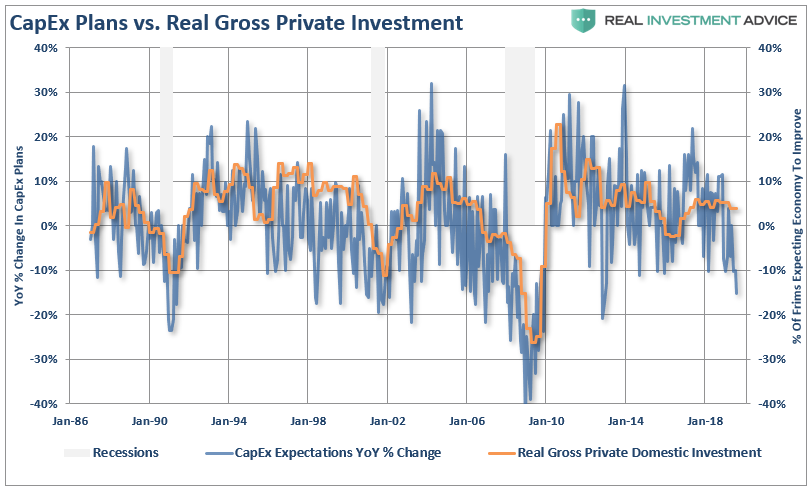

This has significant implications to the economy since “business investment” is an important component of the GDP calculation. Small business “plans” to make capital expenditures, which drives economic growth, has a high correlation with Real Gross Private Investment.

As I stated above, “expectations” are very fragile. The “uncertainty” arising from the ongoing trade war is weighing heavily on that previous exuberance.

If small businesses were convinced that the economy was “actually” improving over the longer term, they would be increasing capital expenditure plans rather than contracting their plans. The linkage between the economic outlook and CapEx plans is confirmation that business owners are concerned about committing capital in an uncertain environment.

In other words, they may “say” they are hopeful about the “economy,” they are just unwilling to ‘bet’ their capital on it.

This is easy to see when you compare business owner’s economic outlook as compared to economic growth. Not surprisingly, there is a high correlation between the two given the fact that business owners are the “boots on the ground” for the economy. Importantly, their current outlook does not support the ideas of stronger economic growth into the end of the year.

Of course, the Federal Reserve has been NO help in instilling confidence in small business owners to deploy capital into the economy. As NFIB’s Chief Economist Bill Dunkleberg stated:

“They are also quite unsure that cutting interest rates now will help the Federal Reserve to get more inflation or spur spending. On Main Street, inflation pressures are very low. Spending and hiring are strong, but a quarter-point reduction will not spur more borrowing and spending, especially when expectations for business conditions and sales are falling because of all the news about the coming recession. Cheap money is nice but not if there are fewer opportunities to invest it profitably.”

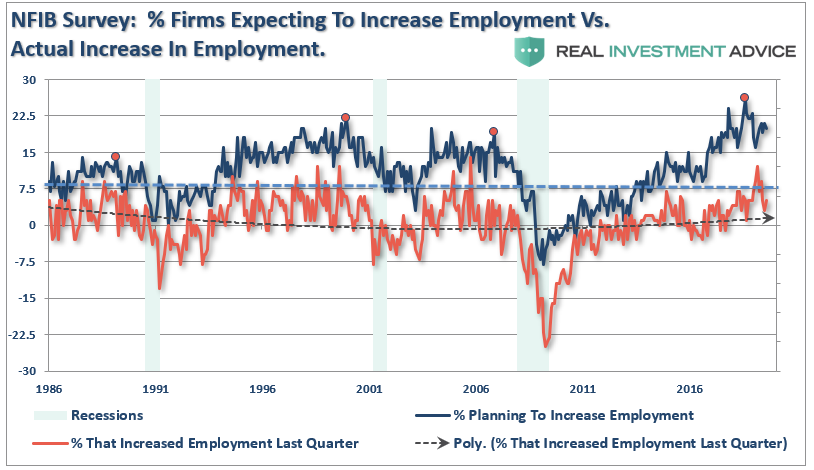

Fantasy Vs. Reality

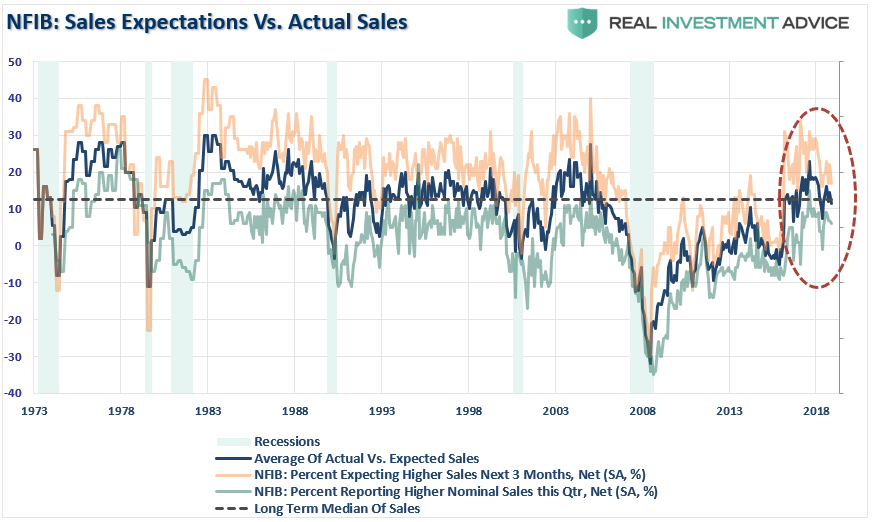

The gap between those employers expecting to increase employment versus those that did has been widening. Currently, hiring has fallen back to the lower end of the range and contrasts the stats produced by the BLS showing large month gains every month in employment data. While those “expectations” should be “leading” actions, this has not been the case.

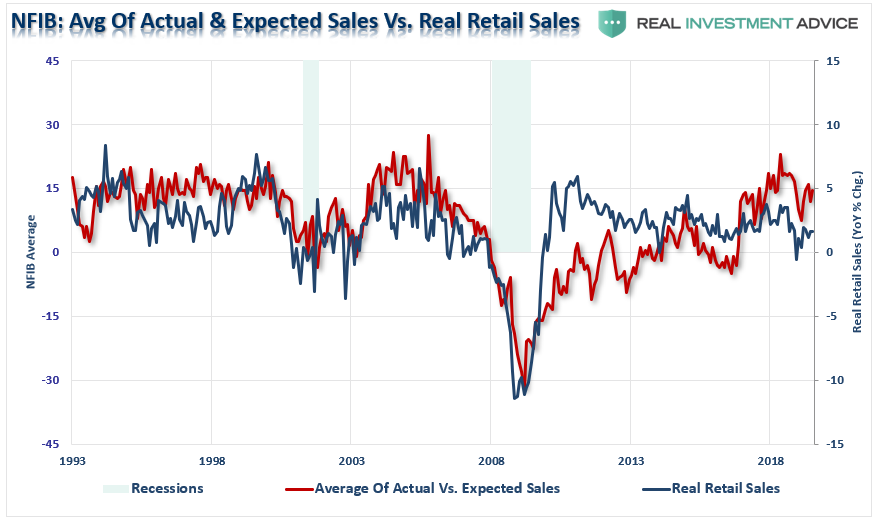

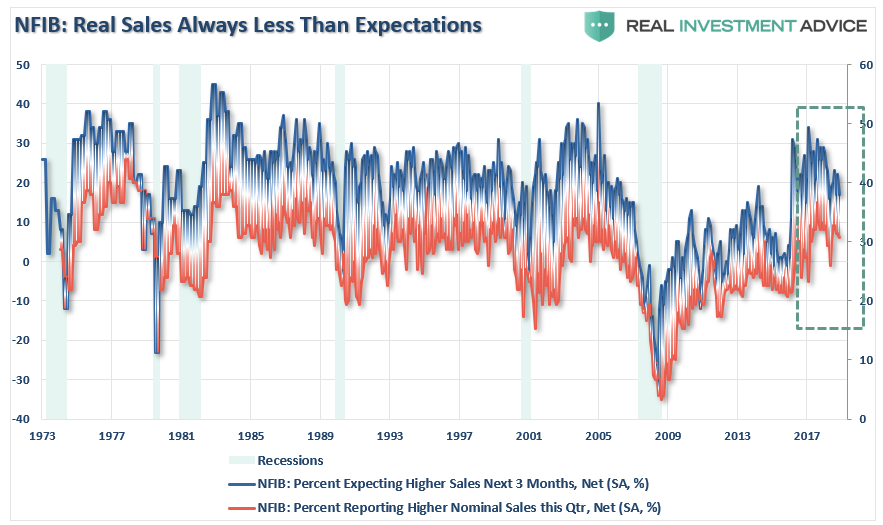

The divergence between expectations and reality can also be seen in actual sales versus expectations of increased sales. Employers do not hire just for the sake of hiring. Employees are one of the highest costs associated with any enterprise. Therefore, hiring takes place when there is an expectation of an increase in demand for a company’s product or services.

This is also one of the great dichotomies the economic commentary which suggests retail consumption is “strong.” While business remain optimistic at the moment, actual weakness in retail sales is continuing to erode that exuberance.

Lastly, despite hopes of continued debt-driven consumption, business owners are still faced with actual sales that are at levels more normally associated with the onset of a recession.

With small business optimism waning currently, combined with many broader economic measures, it suggests the risk of a recession has risen in recent months.

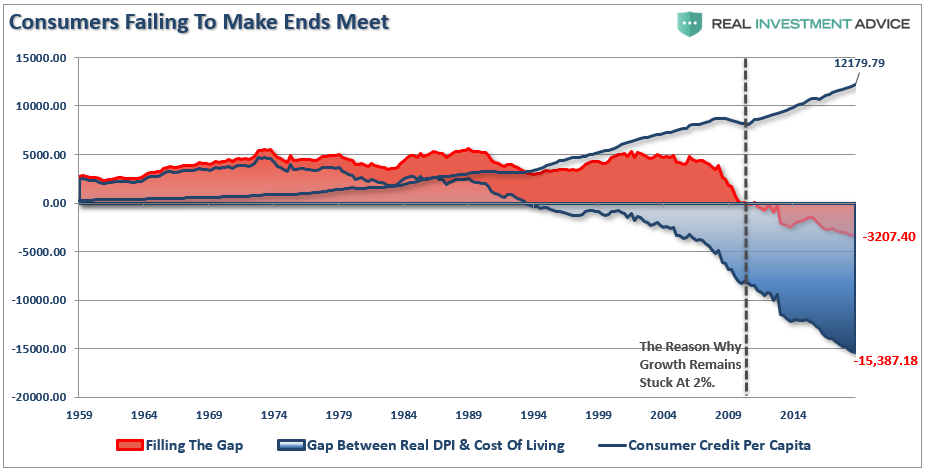

Customers Are Cash Constrained

As I discussed previously, the gap between incomes and the cost of living is once again being filled by debt.

Record levels of consumer debt is a problem. There is simply a limit to how much “debt” each household can carry even at historically low interest rates. In turn, business owners remain on the defensive, reacting to increases in demand caused by population growth rather than building in anticipation of stronger economic activity.

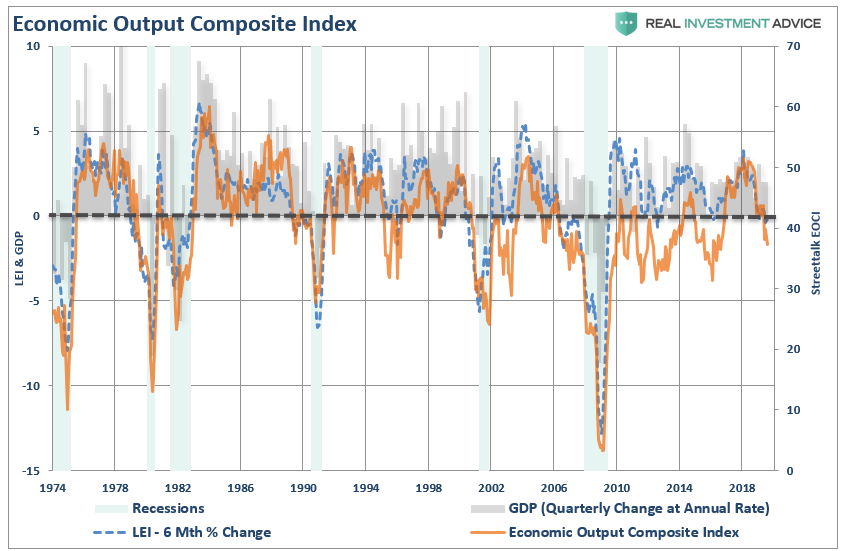

What this suggests is an inability for the current economy to gain traction as it takes increasing levels of debt just to sustain current levels of economic growth. However, that rate of growth is on the decline which we can see clearly in the RIA Economic Output Composite Index (EOCI).

All of these surveys (both soft and hard data) are blended into one composite index which, when compared to GDP and LEI, has provided strong indications of turning points in economic activity. (See construction here)

As shown, the slowdown in economic activity has been broad enough to turn this very complex indicator lower.

No Recession In Sight

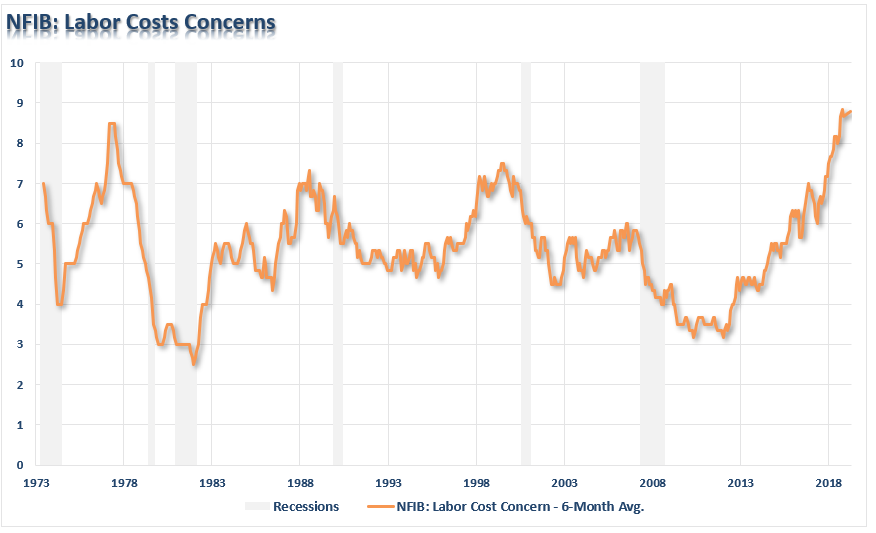

When you compare this data with last week’s employment data report, it is clear that “recession” risks are rising. One of the best leading indicators of a recession are “labor costs,” which as discussed in the report on “Cost & Consequences Of $15/hr Wages” is the highest cost to any business.

When those costs become onerous, businesses raise prices, consumers stop buying, and a recession sets in. So, what does this chart tell you?

Don’t ignore the data.

Today, we once again see many of the early warnings. If you have been paying attention to the trend of the economic data, and the yield curve, the warnings are becoming more pronounced.

In 2007, the market warned of a recession 14-months in advance of the recognition.

Today, you may not have as long as the economy is running at one-half the rate of growth.

However, there are three lessons to be learned from this analysis:

- The economic “number” reported today will not be the same when it is revised in the future.

- The trend and deviation of the data are far more important than the number itself.

- “Record” highs and lows are records for a reason as they denote historical turning points in the data.

We do know, with absolute certainty, this cycle will end.

“Economic cycles are only sustainable for as long as excesses are being built. The natural law of reversions, while they can be suspended by artificial interventions, cannot be repealed.”

Being optimistic about the economy and the markets currently is far more entertaining than doom and gloom. However, it is an honest assessment of the data, along with the underlying trends, which are useful in protecting one’s wealth longer-term.

Disclaimer: Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and ...

more