Much Ado About Nothing: Repo Rates And Doom Narratives

Oh look, the market found something new to obsessively fret about…

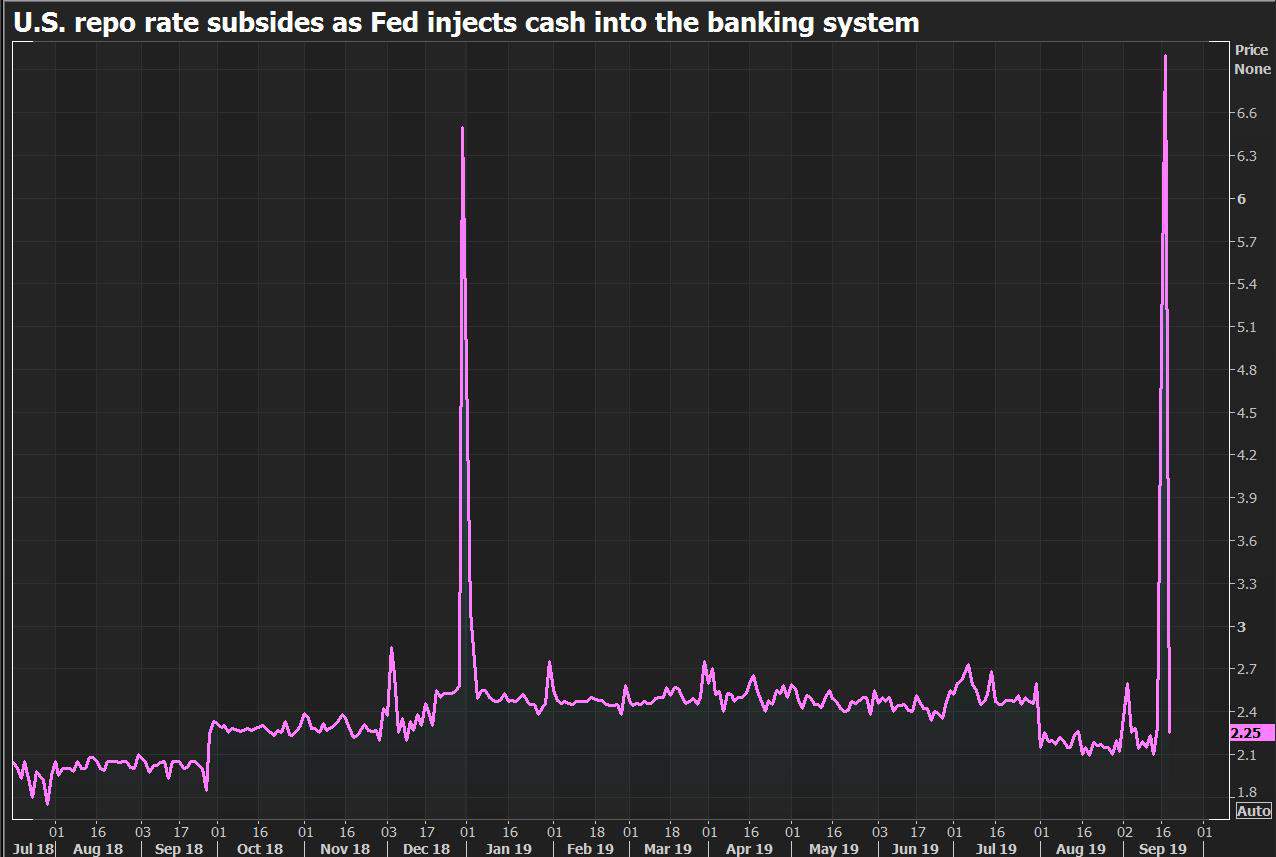

All the fuss is being made over the chart below which shows a “flash crash” in the overnight funding market otherwise known as the repo market.

(Click on image to enlarge)

To be honest, I’m somewhat surprised people are so agitated over this. The repo market is an abstruse corner of our financial plumbing. One that is poorly understood by most and apparently that includes the many financial journos writing hysteria-filled headlines about it.

Take a deep breath. And consider this a short and friendly public service announcement (PSA).

This does not portend doom. Just because we saw similar spikes in the overnight rate in the lead up to the GFC, does not mean this is a precursor to something similar. Like in all things, context matters.

The repo market, to put it in extremely simple terms, is a market where those who have cash can provide very short-term loans to those who need quick liquidity in exchange for safe collateral, such as Treasuries — think broker-dealers who hold lots of securities but need short-term cash loans to fund day to day operations.

The rate at which this money is lent is tied to the fed-funds rate. The fed-funds market is a market for overnight unsecured loans of reserves between banks and other parties. The Fed operates in this market by creating or destroying reserves and lending them out.

New regulations since the GFC require banks to hold a certain level of reserve balances. When the banks experience rising demand for cash relative to their reserves it puts upward pressure on the repo rate, which signals that the Fed needs to add more reserves to the system to allow things to clear.

And it’s in this that the key differences between the repo market issues of today and those that arose in the lead up to the GFC, lay.

You see, rising demand for reserves generally comes from three things (1) Transactions demand (2) Speculative Demand and (3) Precautionary demand. Here’s a clip from a recent report put out by Credit Suisse (CS) explaining the differences.

Transactions demand is based on how much money is being spent. A growing economy or rising inflation supports transactions demand. Transactions are not the same as GDP because many transactions do not add to GDP. Transactions demand is related to money velocity, a slippery and often confusing concept defined by the identity MV = PT (money times velocity equals price times transactions) or MV = PY (money times velocity equals price times income). In these identities money can be base money or a broad aggregate. Usually, it is helpful not to think about money velocity at all or to only consider its inverse, the level of money balances relative to nominal income or total nominal transactions.

Speculative demand means money held in portfolios as an investment. Raising your cash allocation because you expect bond or stock prices to fall is an example of speculative demand. Speculative demand is more appropriate when thinking about the demand for broad money aggregates than it is for reserve balances. However, banks can decide to increase their reserve balances because they dislike other investment opportunities. The decisions by the Fed in 2011 to pay interest on reserve balances support the speculative demand for reserves.

Precautionary demand is balances held to meet sudden payment needs. Precautionary demand is nonlinear: it surges during panics. It was once said that precautionary demand is like a gossamer thread on a gusty night. It is near impossible to forecast. In the 19th century and early 20th century, financial panics coincided with spikes in short-term interest rates because fear led to cash hoarding. The best purses shut. Rates soared, forcing liquidations as payment needs became difficult. After the early 20th century, and particularly after the Great Depression, the Fed committed itself to expanding its balance sheet to meet demand and maintain constant short -term rates. This has been done successfully, so short -term rates fall during financial crises in the post war period, the opposite of the prewar period, when the Fed’s balance sheet was less elastic.

As the CS report goes on to note, in 07’ we saw a sudden spike due to “precautionary demand”. Banks and institutions hoarded reserves while demand for reserves spiked. This led to a jump in repo rates. Today, the demand for reserves is being driven by a rise in speculative demand as well as regulatory changes, such as Basel 3, which require banks to hold greater reserve balances.

We’re also seeing supply-side issues such as the rising fiscal-deficit leading to greater treasury issuance which when combined with an inverted yield curve and high USD funding costs, is hurting foreign Treasury demand leading to bloated inventories amongst primary dealers. And, as CS points out “Primary dealers fund those inventories in the repo market. But if the providers of repo funding find themselves constrained and unable to lend, repo rates spike.”

There’s also things like corporate cash demand for quarterly federal tax payments (Monday was the deadline) and things like dividend payouts that lead to these cyclical stresses in the overnight funding market.

CS concludes the report with the following (emphasis by me).

Understanding the institutional details of the funding markets is important for those who seek to understand risks to the financial system. Zoltan has argued that either reserves or collateral face relative scarcity, always. The immediate post-crisis period, with all that QE, was a time of reserve satiation, and therefore a collateral shortage. Now, through myriad forces, it has become apparent that we are back in relative reserve scarcity, in spite of the Fed’s large balance sheet. There is nothing to fear in this, as it is the usual state of affairs. It does mean that the overnight injection of reserves that we have seen today (September 17) is likely to be only the start of the Fed’s attempt to regain a strict hold on overnight rates. Zoltan has laid out various options including QE, a permanent repo facility, or an aggressive reduction in short term rates, to deal with this problem. But one way or another, the classic solution of a steady increase in reserves supply to match an apparent increase in demand is most likely.

In our view the Fed would be wise to leave interest rate setting to the usual process, which is focused more on growth and inflation concerns than plumbing. Let plumbing decide the balance sheet’s size, stick to a credible interest rate target, and conduct policy accordingly. What we have seen this week is not a crisis but a symptom that we have reentered an old regime for Fed policy operations. To answer the question at the start, is the Fed losing control, we say no it isn’t, but it must now move to allowing its balance sheet to grow in order to maintain its interest rate target. With stable inflation and healthy banks, there is no constraint on the Fed’s ability to do this.

That’s it. The “Repo Flash Crash!!!” is really just an esoteric financial plumbing issue that’s not due to anything sinister and doesn’t presage an impending crisis. It’s something that can and will be handled by policymakers at the Fed, likely through increasing the size of their balance sheet — oh and this would not be a resumption of QE, so disregard those who say it is. It’s literally just managing reserve levels in order to grease the payment settlement system, allowing it to operate properly.

I think the biggest takeaway from all this hoopla is that the doom and gloom machine is still alive and well. Fear is ever-present in this market which is why it’s likely to keep heading much higher.

Mark Dow hit the nail on the head with this tweet.

So feel free to block out this nonsense and continue on with your day.

Disclaimer: All statements are solely opinions and are for educational purposes only.