As Jim Reid notes in his EMR note, "we had two US payrolls and two inflation releases to get through before the next FOMC in September and although the first of these on Friday was a mixed affair, it did trigger a big rally across the US rate curve with 2yr and 10yrs -11.7bps and -14.1bps tighter, respectively, on the day even if yields were still higher at the long-end on the week."

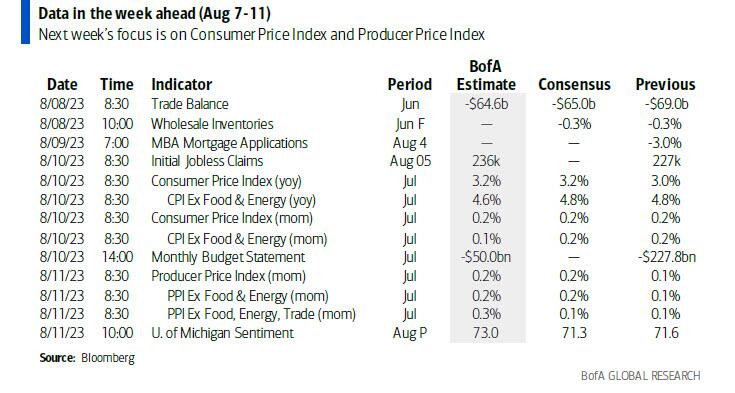

So with jobs out the way we now move on to the next big one, namely US CPI on Thursday. PPI follows fast behind on Friday alongside the University of Michigan consumer survey which contains the all-important inflation expectations series.

One thing to bear in mind for inflation over the next few months is the +15.8% surge in oil prices last month while gasoline prices are rising fast too. According to Reid, it's "too early perhaps to make much inroads yet but a complication if prices stay elevated." In fact, for now, with seasonally adjusted gas prices down a bit from June, DB economists expect a slightly weaker headline (+0.17% forecast vs. +0.18% previously) reading relative to core (+0.21% vs. +0.16%). This would equate to 4.8% YoY for core (though it is very close to rounding down to 4.7%), however, shorter-term trends should show significant improvement. The three-month annualized rate should fall by about 80bps to 3.3%, while the six-month annualised rate should fall by 40bps to 4.2%, both the lowest in over two years.

With regards to the ever-important core services excluding rent and medical services sector, last month's data showed significant progress. This category posted the second-lowest monthly print in the last 21 months (unch.), though much of this weakness was due to a sharp -8.1% drop in airfares. DB's economists explain that this decline brings airfares back to pre-pandemic levels, so is that normality returning or was last month an anomaly. We will see.

Staying with inflation, China CPI and PPI numbers on Wednesday are interesting as the country sits on the brink of consumer price deflation with the latest readings printing 0.0% for the CPI and -5.4% for the PPI YoY. Current median estimates on Bloomberg point to a -0.5% YoY CPI and -4.0% YoY PPI reading.

Meanwhile, after last week's juggernaut, corporate earnings wind down quite sharply with 33 S&P 500 and 55 Stoxx 600 companies reporting this week. Here are the most notable reporters:

(Click on image to enlarge)

Source: earnings whispers.

Here is a day-by-day calendar of events

Monday August 7

- Data: US June consumer credit, China July foreign reserves, Japan June leading index, coincident index, Germany June industrial production

- Central banks: BoJ July meeting summary of opinions, Fed's Bostic and Bowman speak, BoE's Pill speaks

- Earnings: Saudi Aramco, Toshiba, KKR & Co, Palantir, Siemens Energy, Paramount Global

Tuesday, August 8

- Data: US July NFIB small business optimism, June wholesale trade sales, trade balance, China July trade balance, Japan July Economy Watchers survey, bank lending, June trade balance, labor cash earnings, household spending, current account balance, France June trade balance, current account balance, Canada June international merchandise trade

- Central banks: ECB Consumer Expectations Survey, Fed's Harker speaks

- Earnings: Eli Lilly & Co, UPS, Glencore, SoftBank, Bayer, Li Auto, Coupang, Barrick Gold, Take-Two Interactive, Rivian, Lyft, AMC Entertainment Holdings

Wednesday, August 9

- Data: China July CPI, PPI, Japan July M2, M3, machine tool orders, Canada June building permits

- Earnings: Walt Disney, Sony, Illumina, Vestas, ROBLOX, Viasat

Thursday, August 10

- Data: US July CPI, monthly budget statement, initial jobless claims, UK July RICS house price balance, Japan July PPI

- Central banks: Fed's Bostic speaks

- Earnings: Novo Nordisk, Alibaba, Siemens, Deutsche Telekom, Allianz, Tokyo Electron, Orsted, RWE, Rheinmetall, Entain, HelloFresh

Friday, August 11

- Data: US July PPI, August University of Michigan consumer survey, UK Q2 GDP, June monthly GDP, trade balance, industrial production, index of services, construction output, Italy June trade balance, Germany June current account balance, France Q2 ilo unemployment rate

* * *

Finally, turning to just the US, Goldman notes that the key economic data release this week is the CPI report on Thursday. There are several speaking engagements from Fed officials this week.

Monday, August 7

- 08:30 AM Atlanta Fed President Raphael Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic delivers welcoming and closing remarks at the bank's virtual Fed Listens event.

- 08:30 AM Fed Governor Michelle Bowman moderates a panel discussion: Fed Governor Michelle Bowman moderates a panel discussion at a Fed Listens virtual event hosted by the Atlanta Fed. A moderated Q&A is expected.

Tuesday, August 8

- 06:00 AM NFIB small business optimism, July (consensus 90.5, last 91.0)

- 08:15 AM Philadelphia Fed President Patrick Harker (FOMC voter) speaks

- 08:30 AM Trade balance, June (GS -$66.0bn, consensus -$65.0bn, last -$69.0bn): We estimate that the trade deficit narrowed by $3.0bn to $66.0bn in June.

- 10:00 AM Wholesale inventories, June final (consensus -0.3%, last -0.3%)

Wednesday, August 9

- No major data releases scheduled.

Thursday, August 10

- 08:30 AM Atlanta Fed President Raphael Bostic (FOMC non-voter) gives remarks: Federal Reserve Bank of Atlanta President Raphael Bostic gives pre-recorded, virtual welcoming remarks at a Fed webinar entitled Connecting Communities: Shifting Perspectives and Expectations on Employment.

- 08:30 AM CPI (mom), July (GS +0.16%, consensus +0.2%, last +0.2%); Core CPI (mom), July (GS +0.15%, consensus +0.2%, last +0.2%); CPI (yoy), July (GS +3.17%, consensus +3.3%, last +3.0%); Core CPI (yoy), July (GS +4.66%, consensus +4.8%, last +4.8%): We estimate a 0.15% increase in July core CPI (mom sa), which would lower the year-on-year rate by one tenth to 4.7%. Our forecast reflects a pullback in auto prices (used -3.0%, new -0.3%, mom sa) reflecting declines in used car auction prices and the further rebound in new car inventories and incentives. We also expect a decline in lodging and apparel prices due to residual seasonality. We expect shelter inflation to remain roughly at its current pace (we estimate +0.44% for rent and +0.47% for OER). On the positive side, we expect another gain in the car insurance category (we assume +1.4%), as carriers continue to offset higher repair and replacement costs. We also assume a 2.5% rebound in airfares following the outsized 8% drop in June. We estimate a 0.16% rise in headline CPI, reflecting higher food (+0.1%) and energy (+0.4%) prices.

- 08:30 AM Initial jobless claims, week ended August 5 (GS 225k, consensus 230k, last 227k): Continuing jobless claims, week ended July 29 (last 1,700k)

Friday, August 11

- 08:30 AM PPI final demand, July (GS +0.2%, consensus +0.2%, last +0.1%); PPI ex-food and energy, July (GS +0.2%, consensus +0.2%, last +0.1%): PPI ex-food, energy, and trade, July (GS +0.2%, consensus +0.1%, last +0.1%)

- 10:00 AM University of Michigan consumer sentiment, August preliminary (GS 71.3, consensus 71.0, last 71.6); University of Michigan 5-10-year inflation expectations, August preliminary (GS 3.0%, consensus 3.0%, last 3.0%): We expect the University of Michigan consumer sentiment index to decrease by 0.3pt to 71.3. We expect the report’s measure of long-term inflation expectations to be unchanged at 3.0%, as rebounding gasoline prices offset the disinflationary news heard by consumers in mid-to-late July.

Source: DB, Goldman, BofA

More By This Author:

Tesla Tumbles After Chief Financial Officer Zack Kirkhorn "Steps Down"Tyson Foods Plunges As Earnings Fall Short Amid Waning Meat Demand

Futures Rebound As Global Yields Resume Grind Higher

Comments

Log in or sign up to join the conversation.