ISM Non-Manufacturing Report Review

Another Disappointing ISM Report

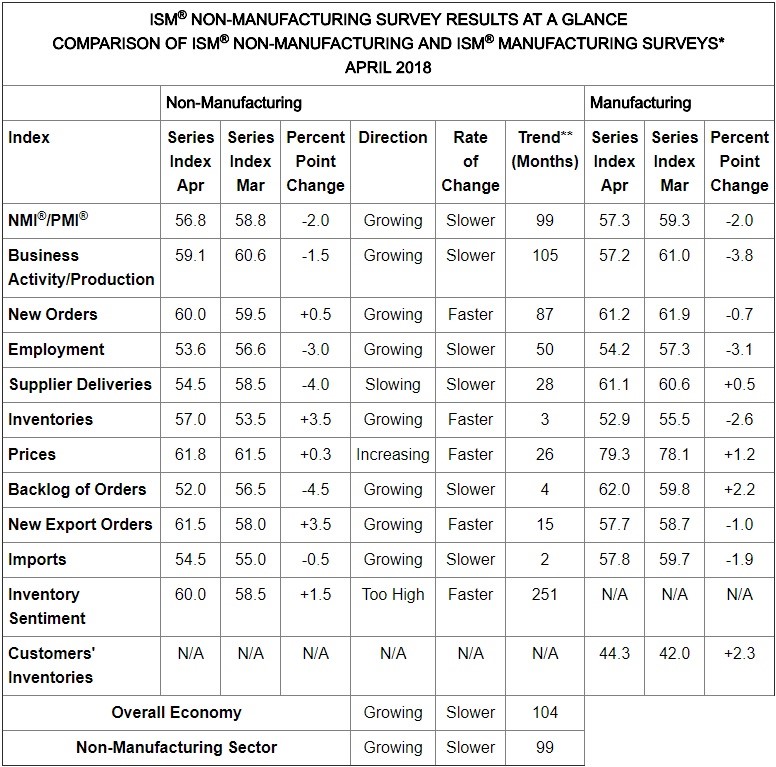

The April non-manufacturing ISM PMI was 56.8 which missed expectations for 58.4. Just like the manufacturing ISM report, it even missed the low end of the range which was 57.3. I’m starting to look for some signs of green shoots in the economy, but we aren’t seeing any in the ISM reports for April. As you can see from the top of the chart below, this is the 3rd straight monthly deceleration. This PMI is below the 12 month average of 57.6. On the bright side, the 12 month average is still increasing.

It’s important to recognize that just like the manufacturing report, this is a report which shows the data going from ‘great to good.’ This PMI is consistent with 2.9% GDP growth which is faster than last quarter’s 2.3% growth, but slower than what the PMI anticipated it would be. That’s a very bad shift in rate of change terms, but we have seen other bouts of weakness without recessions following soon afterwards in this expansion period. I still think there’s almost no chance of a recession in 2018. While that seems to be the consensus, it helps you avoid panicking when the S&P 500 approaches the low end of this recent range or the 200 day moving average. I get optimistic at those levels as the S&P 500 nears long term average valuations.

Specifics Of The PMI

The table below shows the details of the non-manufacturing report. Just like the manufacturing report, the new orders index was strong. In fact, it increased 0.5 to 60 which is impressive in a down report. Employment fell 3 points to 53.6 which was similar to the manufacturing report. I will be reviewing the ADP employment report for April later in this article. There was a sharp deviance between each sector of the economy in the backlog category as the manufacturing backlog was up from 59.8 to 62 while the non-manufacturing backlog fell 4.5 points to 52. The services sector isn’t seeing the same pressure on the supply chain as the manufacturing sector. This pressure on the manufacturing supply chain is causing price increases which aren’t as severe in the services sector. While both price indexes rose, manufacturing is at an extreme 79.3 and services is only at 61.8. Considering the fact that inflation isn’t that high, as the core PCE growth is 1.9%, it makes sense to see the non-manufacturing prices index at that level.

Quotes From The ISM Report

Let’s review some of the quotes from this disappointing report. A management and support services company stated, “Tax reform windfall continues to help business conditions.” As you can see, many of the firms in this report are experiencing positive business conditions which makes it tough to see what is moving the needle in the wrong direction. The economy was clearly helped by the tax cuts. It may explain why the American economy is outperforming Europe despite America’s tighter monetary policy. The benefit of the tax cut will shine through when America is able to cut rates during the next recession while the ECB has little wiggle room.

A construction company stated “The trade tensions are impacting purchasing of steel and are causing suppliers to send letters of concern regarding contracted purchases for this year and the future based on these proposed tariffs.” The construction industry is particularly affected by the tariffs because it uses steel and aluminum. The overall economy is experiencing some uncertainty because of the potential for a trade war. That can slow down new orders for some businesses. It’s an excuse to be conservative.

ADP Jobs Report

Usually, I review the ADP private sector employment report to get an idea of what the BLS report will be. At this time, the BLS report is already out, but it’s still interesting to see the details of the ADP report since I don’t think the BLS report is perfect. The ADP report was great as it showed 204,000 jobs were added. This was the 6th straight month of at least 200,000 jobs created. This beat estimates for 190,000 jobs, but was below the prior revised report which showed 228,000 jobs created.

Mid-sized businesses added the most jobs as there was an 88,000 increase. Small firms added 62,000 jobs and large firms added 54,000 jobs. In this expansion, large firms have been adding more jobs as a percentage of the labor market because the percentage of new businesses is falling. Millennials are the least entrepreneurial generation in over 100 years.

The goods producing sector did well as it added 44,000 jobs. The services sector added 160,000 jobs. The trade, transportation, and utilities segment added 14,000 jobs. This is an important part of the economy because there is currently a shortage of truckers which is causing huge cost increases for firms in the food services business. The increasing price of oil is a double whammy for firms that need to transport their products. The professional and business segment added 58,000 jobs which is a big positive.

Chances Of A Recession

As I mentioned previously, I don’t think there will be a recession this year. The chart below gives you the odds of a recession according to Goldman Sachs’ model. It shows there’s less than a 10% chance of a recession in the next 4 quarters. That implies there’s between a 0% and a 10% chance of a recession in 2018. While the numbers in the chart look great, when you look at the previous cycles, you can see they don’t get that high right before recessions. The line showing a recession in the next 4 quarters only gets to about 30% right before recessions implying we’re not completely in the clear. Since I think there will be a recession in 2019 or 2020, I think the line showing about a 35% chance of a recession in 12 quarters is too low.

Conclusion

I’m looking for a mild turnaround in the economy in the next few months as the decline in rate of change terms abates. So far, we haven’t seen such a turnaround as the ISM manufacturing and non-manufacturing reports have shown a string of months with decelerating growth.

Disclaimer: Neither TheoTrade or any of its officers, directors, employees, other personnel, representatives, agents or independent contractors is, in such capacities, a licensed financial ...

more