The downward momentum in Hungary’s labour market seems to have come to an end. However, the road ahead remains bumpy as sectoral divergences persist and stubbornly strong wage growth raises the possibility of inflationary risks

| 4.4% |

Unemployment rate (Feb-Apr)ING Forecast 4.5% / Previous 4.4% |

While April wasn't particularly strong, the big picture is encouraging

According to the latest unemployment statistics, there has been no significant change in the Hungarian labour market, with the model estimate for April 2024 showing an unchanged unemployment rate of 4.4%. Meanwhile, the official three-month moving average rate moved to 4.5%, an improvement of 0.1 percentage points. However, this positive change is largely statistical, as the unemployment rate rose sharply in the first month of the year – an effect that has now been removed from the three-month moving average.

In last month's favourable release, we had already indicated that we would need to see at least three consecutive months of meaningful positive change before we could say that the labour market had turned the corner. But so far, the change in the April data is only marginal.

As for the number of those unemployed, both statistics show only a change within the margin of error, and the number of people out of work was around 220,000. While it may sound like we are downplaying the improvement, in general the developments over the past three months have been quite encouraging.

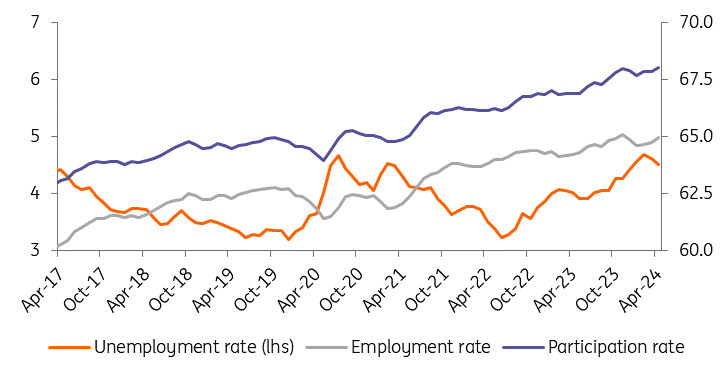

Historical trends in the Hungarian labour market (%, 3-m moving average)

(Click on image to enlarge)

Source: HCSO, ING

The detailed data also shows that the number of inactive persons fell in April as a result of the population decline. However, around 3,000 people returned to the labour market as active participants and a similar number found employment. Of course, one month's data is not a good basis for drawing firm conclusions, but it does seem to suggest that demand for labour is picking up somewhat. After all, employment has expanded for the fourth month in a row, albeit at a slightly decelerating pace. The official three-month moving averages show a broadly similar trend.

In other words, as the Hungarian economy emerges from recession, the state of the labour market is improving somewhat at the level of the national economy. This is encouraging and could even herald a sustained positive trend ahead.

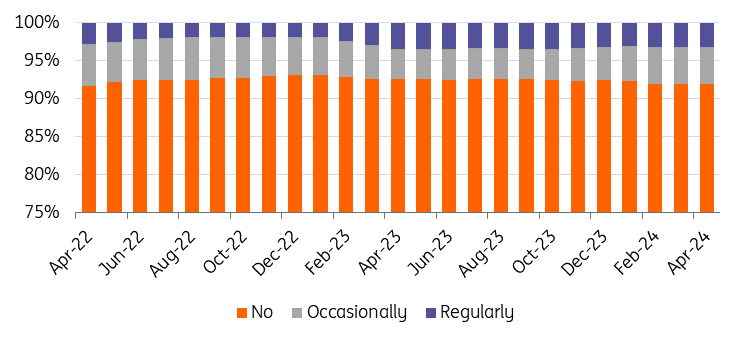

For now, we can only speculate as to what might be driving the increase in the participation rate. The 68% rate is an all-time high. Given that the unemployment rate for women is falling more dynamically, it is likely that they are the main demographic returning to work. The suspicion remains that livelihood issues are driving the return of families to dual-earner status. This may be facilitated by employer flexibility, with more flexible working hours and even working from home several days a week becoming more common.

Change of teleworking of employees (3-m moving average)

(Click on image to enlarge)

Source: HCSO, ING

In light of the latest labour market data, we are a step closer to answering the question of why wages are still rising so dynamically, with surveys predicting pay rises of 5-10% for the existing workforce this year. It may well be that new entrants or job changers are currently driving this trend.

In the coming months, the labour market will be shaped by two forces. On the one hand, seasonal employment will increase as summer approaches, which should help to sustain the slow improvement in interest rates. On the other hand, the slump in industry is leading to working time rationalisation in the face of falling orders. This mainly means more flexible use of working hours, but redundancies are already being made in some parts of the sector. All in all, a marginal improvement is expected in the coming months, provided that the favourable trends in the domestic market continue. In other words, we expect a significant improvement in Hungarian labour market data in the second half of the year.

This is suggested by various confidence indices and surveys, which already show an improving trend in most sectors (not only in Hungary, but also in Europe). However, the labour market typically follows changes in the real economy with a considerable lag. In other words, the improved economic performance expected for the first half of this year is likely to be reflected to a greater extent in companies' labour market decisions only in the second half of the year. For the year as a whole, the unemployment rate is expected to be around 4.5%.

| 13.9% |

Average wage growth (Mar)ING Forecast 9.9% / Previous 14.0% |

Wage growth remains perplexingly strong

According to the latest data, the significant slowdown in wage growth anticipated by us has not materialised. Instead, the annual pace of average wage growth remained remarkably high at 13.9% in March, showing only a minimal deceleration. In this regard, the current wage outflow dynamic continues to be extraordinarily robust.

We still question whether the high wage outflows witnessed in the first quarter truly reflect this year's wage setting processes. Considering the prevalent practice among numerous companies of adopting a spring-to-spring wage cycle (where wage increases occur in March-April rather than January), we anticipated and continue to expect a substantial slowdown in wage growth during the spring months. So far, the March data strongly contradicts our assumption. Based on these findings, the behavior suggested by various surveys – indicating that employers are contemplating wage increases of between 5-10% for the current year – remains questionable.

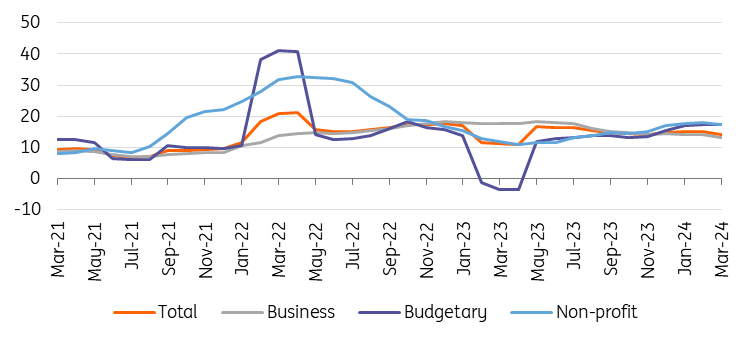

Wage dynamics (3-month moving average, % YoY)

(Click on image to enlarge)

Source: HCSO, ING

While high wage dynamics can induce positive changes in the real economy by boosting consumption, they also present upside risks on the inflation front. If the average wage growth rate continues to exceed 10% in the coming months, contrary to labour market survey projections, it could not only erode households' precautionary motives and strengthen demand but also bolster companies' pricing power.

Retrospective repricing is a particularly concerning practice in Hungary, also highlighted by the central bank. In this regard, if there were a substantial expansion in households’ purchasing power, it could enable some companies to implement large price increases. This scenario raises the possibility of a potential wage-price spiral. Consequently, in our view, the central bank must closely monitor the development of wages alongside services inflation when making future interest rate decisions.

Looking at the sectoral breakdown, it remains evident that wage growth in the public sector significantly outpaced the national average in March, reaching 17.4%. This is primarily a consequence of the ongoing wage adjustments in the education sector. A similar acceleration is observable in the non-profit sector as well, as educational institutions operating under foundation structures fall within this category. Contrary to expectations, the private sector did not experience a slowdown, with wage growth remaining close to 13%. This indicates that the high national average wage outflow cannot be solely attributed to the public sector, further reinforcing the question of when – or if – the anticipated slowdown forecasted by surveys will materialise.

Certain sub-sectors within the private sector warrant particular attention; construction, logistics, accommodation services, catering, and real estate activities exhibit exceptionally robust wage growth. This is especially surprising in the construction industry given its weak performance, and regarding the real estate sector, one might have a similar impression. However, high wage increases seem more understandable in the other two sectors mentioned above given the fact that they are grappling with labour shortages.

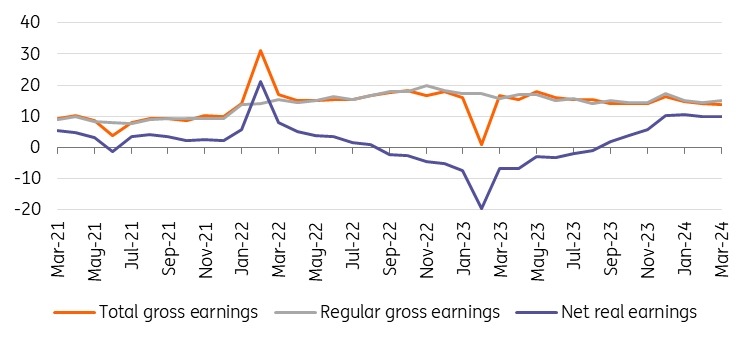

Nominal and real wage growth (% YoY)

(Click on image to enlarge)

Source: HCSO, ING

It is also noteworthy that the gap between average and median wages continued to narrow, likely reflecting the impact of the minimum wage increase, and suggesting that wage growth is below average in sectors with inherently higher earnings. Moreover, the robust growth in regular earnings indicates that bonus payments cannot account for the high pace of wage increases observed in March.

Given that inflation has essentially bottomed out this year, while the pace of average wage growth has remained broadly unchanged, real wage growth on an annual basis was 9.9%, similar to the previous month. Looking ahead to the rest of the year, wage growth in purchasing power is likely to erode further.

On the one hand, we still expect wage outflows to slow (although this is increasingly questionable), while inflation is expected to pick up. For now, we maintain our expectation that the pace of wage growth for 2024 as a whole will be around 10%, surrounded by strong upside risks. As we expect inflation to be around 4.5% for the year on average, this means that we are calculating with a meaningful real wage growth.

More By This Author:

Think Ahead: What If US Inflation Is Much Lower Than We Think?Asia Morning Bites For Friday, May 24

Asia Week Ahead: Australia Reports Inflation While China Releases Latest PMI Readings

Comments

Log in or sign up to join the conversation.