Federal Debt A Danger To Business, But Not This Year

Federal debt as a percent of GDP DR. BILL CONERLY BASED ON DATA FROM OFFICE OF MANAGEMENT & BUDGET

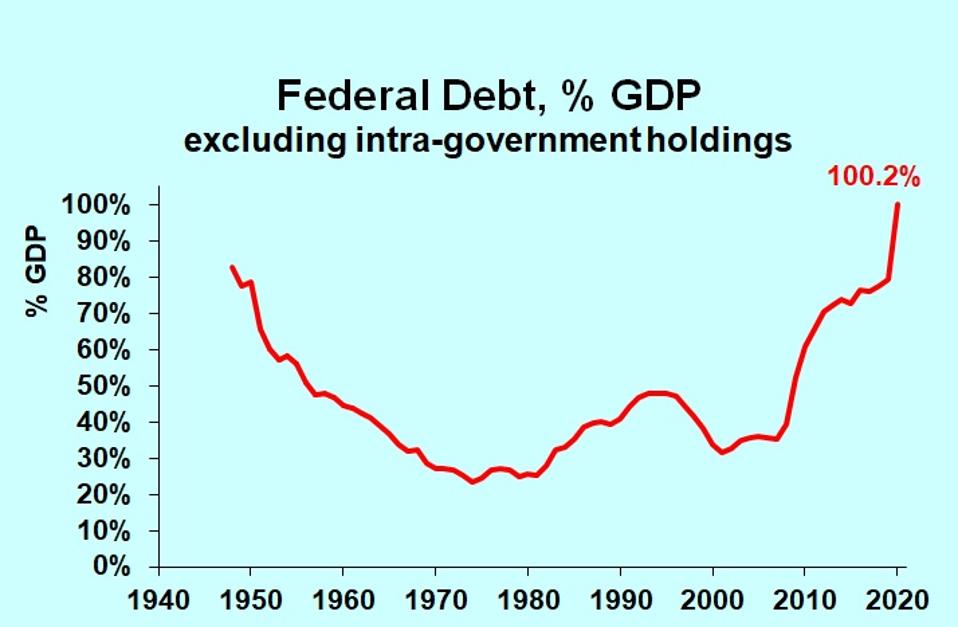

The U.S. government’s debt exceeded gross domestic product in the recent fiscal year. Another big addition to debt will come with the new $900 billion relief bill passed by Congress. Do we have too much debt, so much that it will prevent future economic growth?

The debt level, both current and anticipated in 2021, is worrisome but not likely to trigger an immediate problem. The new spending does raise the question of when our debt will be a serious problem. Economists are not very good at pinpointing the date of an upcoming crisis, but the country cannot continue on the current path without a day of reckoning. Business strategists should think about higher inflation and greater variability of the economy.

The nation has, in the past, enjoyed robust growth when debt was high. After World War II, debt held by the public reached 106% of GDP. (Debt held by the public excludes debt held in intra-government accounts. The Social Security trust fund, for example, holds U.S. treasury bonds, which are not counted as “debt held by the public.”) The post-war years saw debt grow slowly while GDP grew rapidly, brining the ratio down to a low of 23%. So the high debt itself was not a deterrent to further economic expansion.

The post-war era, though, was marked by fiscal conservatism, as the budget bounced between deficit and surplus. When deficits occurred, they were small relative to GDP, much smaller than U.S. deficits during the good years between the 2008 recession and the pandemic recession. So we are not likely to repeat that benign experience, though it’s possible.

We’ve got another problem not counted as official debt: U.S. obligations to pay Social Security and Medicare. The trust funds are not adequate to cover the liabilities. Our unfunded liabilities are not counted as debt, but they really are. So we are in worse shape than the chart shows.

There’s no magic in the ratio of debt to GDP. Computing debt this way makes comparisons over time and across countries easier. But debt is a point-in-time measurement, while GDP is a flow over a period of time. Although the ratio helps to see trends, the actual number is meaningless by itself.

Compared to other developed countries, the U.S. before the pandemic had high debt relative to GDP, but not the highest (which was Japan). We were just a little above France, Belgium, Spain, and the United Kingdom. Complete data for 2021 will not show us above Japan, Greece, and Italy.

The worst possible result of too much borrowing is a debt crisis, which occurs when lenders won’t extend further credit to a country. The trigger point for a debt crisis is extremely difficult to pinpoint. It’s not the case that a country’s borrowing cost gradually rises as its debt-to-GDP ratio rises. Rather, borrowing rolls along just fine until, suddenly, nobody wants to buy the country’s bonds. The U.S. is probably far away from that threshold, but it’s hard to be sure given that the threshold is very difficult to identify prospectively.

The more likely problem from our debt is that it converts into the money supply that fuels inflation. That would not happen if the Fed refrained from buying the government’s bonds. We would just get higher interest rates. The higher interest rates would eventually limit capital spending and consumer borrowing, slowing both expenditures and additions to productive capacity. But that’s not what is happening.

With the Federal Reserve buying massive amounts of government debt, the reserves to the banking system are skyrocketing. Eventually, those reserves will turn into a money supply. Without a concomitant increase in productive capacity, too many dollars will chase too few goods. Inflation will result.

When inflation rises, the Federal Reserve will tighten monetary policy. Getting the timing and magnitude of tightening just right is extremely difficult, so a recession is likely. Once the economy loses stability, it can easily oscillate between boom and bust, setting up a weak decade, with hard-to-forecast business cycles and low productivity growth.

Inflation will also act like a tax on people’s assets. Those who buy a bond or a certificate of deposit expect a return of their purchasing power plus interest. With inflation, they will find that the interest fails to cover the loss of purchasing power. Although some inflation hedges may hold their value, few if any will earn a reasonable return on the investment, and all come with significant risk. So the overwhelming majority of people with assets, whether in small business, stocks, bonds, or through IRAs and 401k plans, will suffer a loss of real value. That is how we will pay for the relief bill.

If the relief bill would stimulate the economy, businesses and consumers might end up better off, but that won’t happen. The relief bill helps some people and businesses now suffering but won’t solve the economy’s problem: limited economic activity because of social distancing, both voluntary and compulsory.

Business strategy going forward should not anticipate an immediate crisis but should be based on inflation and greater volatility of the economy than we have seen in recent years. With the timing of future inflation and business cycles uncertain, the flexibility of tactics must be a key element of strategy.

The $900 billion relief spending is not free. It will be paid back by the people of the country. The bill won’t come due in 2021 and probably not in 2022, but eventually, we, the people, will pay the bill.

Disclosure: None.