Debt Bombs Ticking Across The Globe

There are times when writing from the macro perspective can be challenging, particularly when macro takes a backseat as it is prone to do during parts of the business cycle. This year macro is back with a bang.

JPMorgan recently assessed the chance of a recession in 2019 has risen to 35%from just 16% in March based on macro data alone. The markets realize that the underlying dynamics have changed and are grappling with what to expect next:

- As we mentioned last time, in 2017 only 1 of the 70 asset classes Deutsche Bank tracks closed in negative territory despite many being inversely correlated – clearly a market behaving oddly. As of mid-November, 90% were in the red for 2018 as the overexuberance of 2017 is forced to pay the piper.

- In 2017 44 of the 47 country stocks in the global MSCI index closed up for the year. As of the December 11thclosing, only 3 are in the green.

- The suppressed volatility in 2017 has led to hyper in 2018 as the S&P 500 has lost 3% or more in three market sessions this year with not one gain of 3% or more, a dynamic which last happened in 1936. The Dow Jones Industrial Average has experienced four days of 3%+ losses and no daily gains of that magnitude, a dynamic which last happened in 1897. (Hat tip to David Rosenberg of Gluskin Sheff)

Market dynamics are reflecting the increase in macro/political volatility across much of the world, but the headlines have yet to catch up with the primary drivers underlying the deep changes. In our previous Context & Perspectives piece, I discussed how we are seeing a profound decline in the level of liquidity at a time when debt levels are back to record highs. This week is a highlight reel of warning signs in the context those record levels of debt.

- US employment

- US Treasury balance sheet and yield curve inversion

- Oval Office produces day time TV level drama

- US China Trade War

- UK Brexit Drama Spikes

- Paris on Fire

- Italy sees an opportunity

USA Employment Picture

Last Friday’s Nonfarm payrolls were significantly below expectations at +155k versus expectations closer to +200k on top of downward revisions of 12k to the prior two months. That’s not great, but amidst all the hype around this being a phenomenally strong economy, the workweek shrunk to a 14-month low of 34.4 hours from 34.5 in October. That translated effectively into 370k jobs lost, which means that the real picture for employment was a net loss of -215k (+155k new payroll -370k from shortened work week). The -0.2% decline in aggregate hours worked, the second decline in the past three months, means that unless there was a big jump in productivity, output, aka real economic activity, contracted for the month.

We also saw a decline in earnings with average weekly income falling -0.1% given the decline in the average workweek and an increase of hourly earnings of +0.2% versus +0.3% expected. This is the first decline in weekly earnings in 2018 and may call into question the expectations around Christmas shopping.

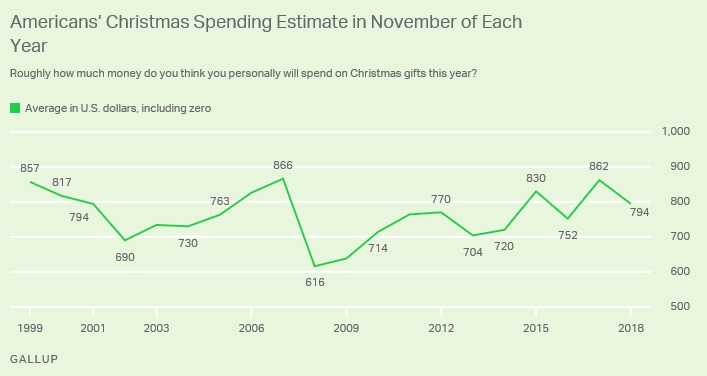

The recent University of Michigan Consumer Sentiment survey found that an increasing number of respondents are expecting unemployment to be higher in the next twelve months than lower and a recent Gallup poll found that Americans plan to spend less on holiday gifts today than they expected back in October and less than they expected to spend in 2017. The $91 decline in expected spending since October is, “one of the steeper mid-season declines, exceeded only by a $185 drop that occurred in 2008, as the Wall Street financial crisis was unfolding, and a $102 drop in 2009 during the 2007-2009 recession.” The environment is changing.

Putting it all together, last month saw a contraction in the workweek, in the index of aggregate hours worked and in average weekly earnings – not exactly a story of a robust economy despite the headline 3.1% year-over-year rise in average hourly earnings, the strongest read since 2009. Digging into the details can give a different picture.

Earlier this week the JOLTS (Job Openings and Labor Turnover Survey) saw the number of job openings increase in October to 7.08m from September’s 6.96m, but still below the August peak of 7.29m. The number of voluntary quits declined to a 4-month low. This was likely thanks to, per data from the Atlanta Fed Wage tracker, ‘job switchers’ and ‘job stayers’ enjoying the same wage gains for the first time in three years. This is an indicator of rising wage pressures which puts pressure on margins at a time when as the FT put it, “Cracks in the corporate debt market begin to show.”

October also saw a greater-than-expected increase in consumer credit to $25.4b versus the $15b driven largely by student debt and auto loans – debt, debt and more debt.

Over the past few weeks your Tematica Research team has called out some Thematic Signals here, here and here that illustrate between the impact our Aging of the Population and the Middle Class Squeeze investing themes, many American consumers continue to struggle.

US Treasury Balance Sheet and Yield Curve Inversions

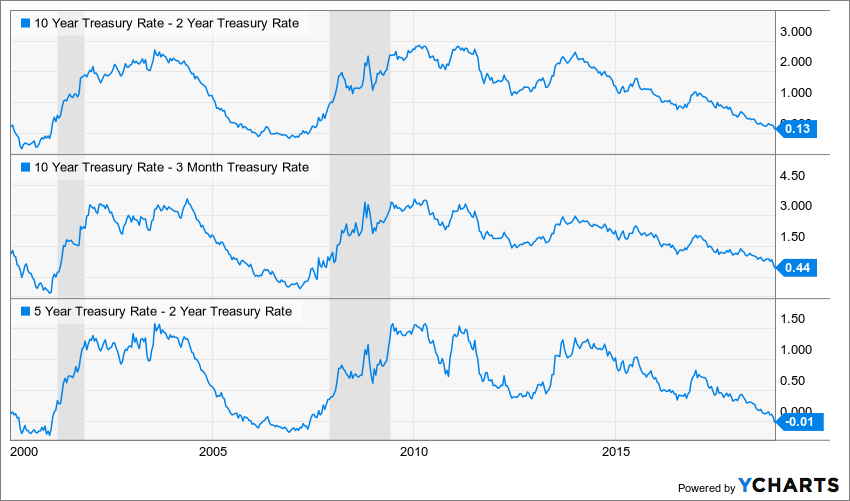

This week’s CPI report was in line with expectations at 2.2% year-over-year and showed inflation that is high enough for the Federal Reserve to proceed with another rate hike this month, but the bond yield landscape is changing. On December 3rd, the 3-year Treasury note yield exceeded that of the 5-year for the first time since 2007, which is known as a yield curve inversion. As of December 12th, the 5-year yield sat below the 2-year. The spread between the 10-year and the 2-year is at a level not seen since 2007 and is close to inverting as well. The spread between the 10-year and the 3-month (which is closely watched as a recessionary signal) has plummeted from 136 basis points in February to just 44 and been cut in half in the past month alone. This has the Federal Reserve’s attention.

As a reluctantly avid Fed watcher, (I wish monetary policy wasn’t such a driving force in the global economy these days) I’d be remiss if I didn’t point out this fascinating tidbit. On June 27, 2017, when the VIX Volatility Index sat at 11, US Federal Reserve Chair Janet Yellen said,

“You know probably that would be going too far but I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will be.”

On Tuesday December 11th, 2018 (532 days or 1.46 years later) when the VIX sat at 22, now former US Federal Reserve Chair Janet Yellen said on CNBC,

“I’m not sure we’re working on those things in the way we should, and then there remain holes, and then there’s regulatory pushback. So I do worry that we could have another financial crisis. ″

You can’t make this stuff up.

On top of raising rates to tighten financial conditions, the Federal Reserve tapering has reduced its balance sheet by 8.3% since its tapering program commenced 13 months ago – that’s a solid level of liquidity drain as we’ve discussed in our last Context & Perspective piece.

The futures market is now pricing in less than 20 basis points of rate hikes next year versus over 55 basis points just a few months ago.

Oval Office Drama

Just when you thought the acrimony inside the beltway could not possibly get worse, it did. On Tuesday December 11thPresident Trump and Vice President Pence met with House Minority Leader Nancy Pelosi and Senate Majority Leader Chuck Schumer in the Oval Office while the network TV cameras rolled to discuss the impending government shutdown.

If this is a preview of what we can expect in the next two years with a divided government, the markets are right to be concerned with Capitol Hill’s ability to take constructive action if/when the economy slides into a recession let alone deal with the immediacy of a potential government shutdown which would leave federal employees without a paycheck at Christmas.

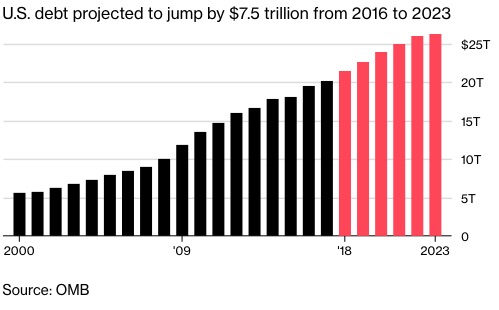

At a time when corporate balance sheets are the weakest they’ve been since the financial crisis, the federal deficit is at a percent of GDP not seen outside of a war or a recession. Total public debt outstanding has risen by $1.7 trillion (or 6.6%) since the start of the year. The current debates in DC are not focused on reducing the deficit, but rather a battle over where to spend. This means we are likely to see a greater supply of Treasury bonds on the market in the coming year(s) to compete with the high level of corporate debt that will need to be refinanced as we discussed in our last piece.

This level of dysfunction is particularly concerning when we look around the world and see political volatility outside the US also reaching heights rarely seen. Keep in mind that during the prior financial crisis leadership in much of the world’s leading nations were much more stable. The bottom line here is the current market volatility doesn’t fully reflect the heightened political risks emerging.

US China Trade War

The trade war between the US and China has seen some major fireworks over the past few weeks from the arrest of China’s Huawei’s CFO Meng Wanzhou to Canada granting her bail to rumors that China plans to submit a proposal to reduce its 25% surcharge on US-made vehicles. One day it is acrimony, the next rumors of attrition. What we do know is that China’s economy is weakening, (China imports rose just 3% year-over-year versus expectations for 14%) and the trade wars are having an impact on both nations. Regardless of one’s political preferences on this topic, when the two largest economies in the world go head-to-head, it is going to have a negative impact on global growth in at least the near-to-medium term.

Tying this back to the debt issue, given China’s black box economy with data tightly controlled by its government, it is impossible to have accurate data on just how high the nation’s debt level has reached. Estimates are that China’s total debt has hit more than 300% of GDP(according to the Institute of International Finance), versus the “official’ level of 47%, and Chinese distressed assets have grown by over 25% in the 18 months according to data from PwC.

China’s economic growth has been heavily dependent on ever-rising levels of debt and is showing signs of stumbling. As the world’s second largest economy, when China struggles the world will feel it.

UK Brexit Drama Spikes

The UK was not to be outshined by this week’s Oval Office “disagreement” as its political strife spiked when Prime Minister Theresa May postponed the Parliamentary vote on the agreement she reached with the European Union on fears that it had a snowball’s chance in hell of passing. The EU leaders insist that there will be no fundamental changes made and the Prime Minister survived a vote of no confidence in her leadership the night of December 12thas euro-skeptic MPs attempted a coup against her to wrest control of the final 106 days of Brexit talks. She was forced to agree to not lead the Tories into the next election, which puts her at risk of becoming a lame duck like her German counterpart, Angela Merkel.

We are quickly moving towards the worst of all possible outcomes, at least in the near-to-medium term, with no deal between the European Union and the United Kingdom and the UK lacking any strong leadership as it sails into uncharted political territory. All this uncertainty it a major headwind to economic activity on both sides at a time when people in the UK and the EU are increasingly angry over the lack of improvement in household finances as it has also been struggling under the Middle Class Squeeze. Voters will be looking for more rather than less government spending if/when their respective economies weaken, which means even more debt in a world awash with it.

Paris on Fire

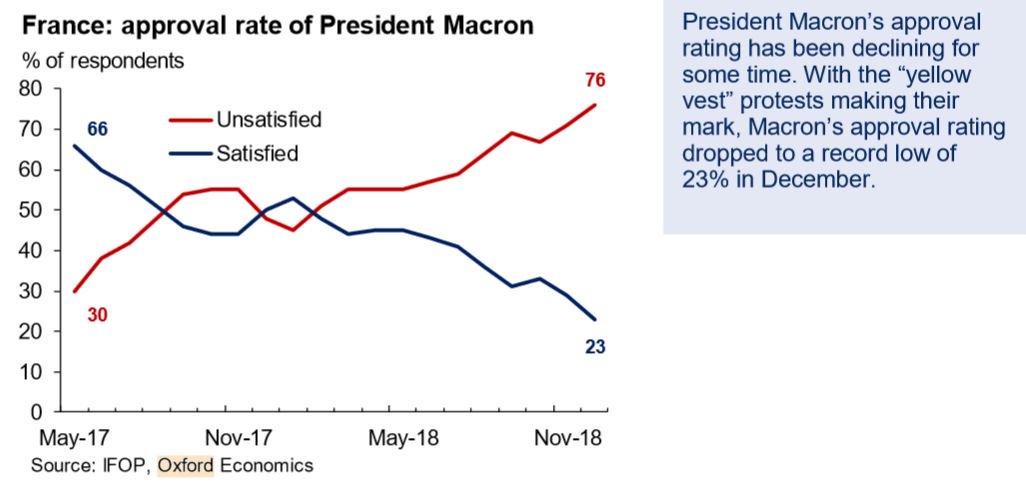

Over the past weekend Paris erupted into violent protests, the magnitude of which is under debate, but the result of which was a clear – a loss a political firepower for France’s President Macron as he agreed to roughly €10 billion in concessions, including a minimum wage hike and tax breaks for employers. Many in France have also been suffering from Middle Class Squeeze and are frustrated by their leaders’ ongoing inability to shift the economy into something that provides them with better opportunities. Their demands mean more government spending which means more debt.

France is now on track to have the biggest budget deficit in the EU next year and Macron’s credibility and political power have taken a serious blow. This is yet another dangerous blow to the European Union.

Italy Sees and Opportunity

While Paris was burning, Italy’s Matteo Salvini and Claudio Borghia were loving (and tweeting) what this would likely mean for their budget talks with Brussels, who as you may recall had sent the Italian leadership back to the drawing board in Rome to hammer out a budget with a smaller deficit. To put their deficit in perspective, the rejected plan was for 2.4% of GDP versus the US on track this year for over 6.6%. The troubles in Paris may give Rome confidence to push back against Brussel’s demands as they meet on December 12th. Late on the night of Wednesday December 12thrumors started to fly that perhaps the Italians would reduce the planned deficit to 2% of GDP. Either way, Italy is facing a weak and weakening economy with nearly €200 billion of Italian bonds coming due next year that will need to be reissued in addition to its current deficit.

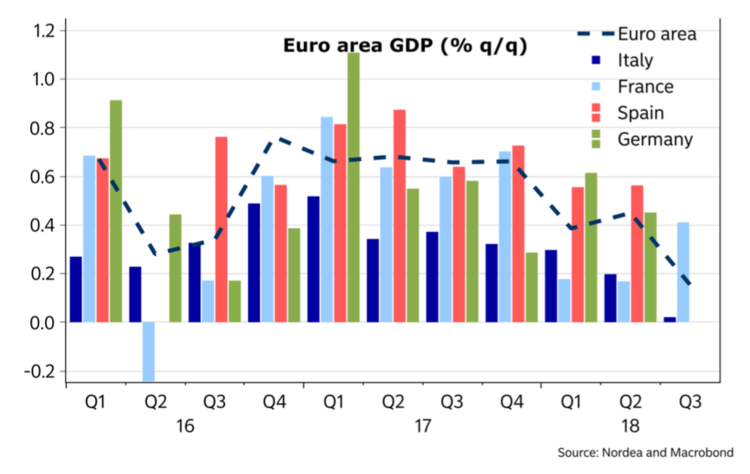

Fighting Brussels is one thing, but the debt markets are another thing entirely and they are not pleased with what they see as evidenced by the widening spread between the Italian and the German 10-year, which has reached the highest level since the worst of the eurozone crisis. Moody’s has downgraded Italy’s rating to Baa3 while S&P and Fitch held their ratings but downgraded the nation’s outlook. If Italy’s economy weakens further, and its economy already contracted by -0.1% in the third quarter versus the prior, it could lose its investment grade standing which would have a major impact on bond markets as Italy’s external debt was $2.5T at the end of 2017.

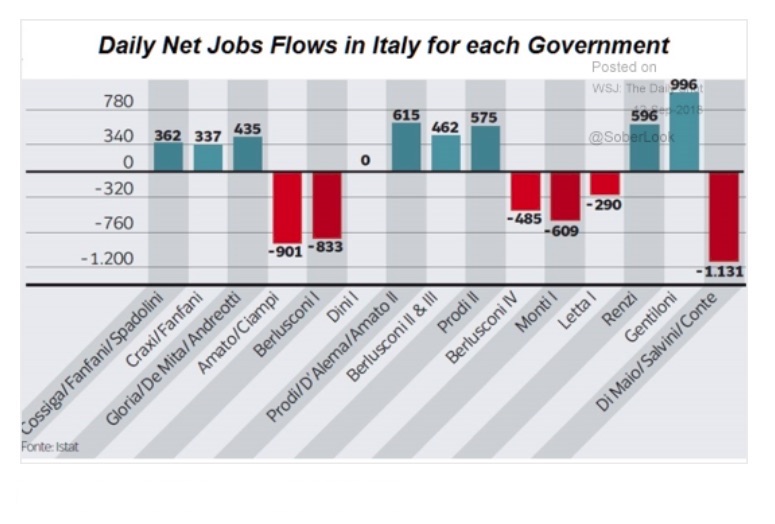

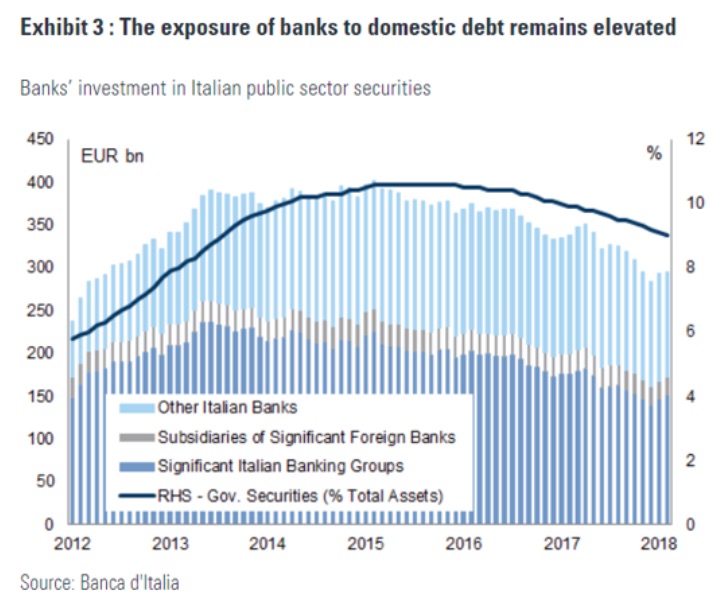

When it comes to the problems arising from Aging of the Population and the Middle Class SqueezeItaly is in even worse shape than the United States and its banks still hold an elevated level of domestic debt. The employment situation is worsening.

The banking sector is quite vulnerable.

Italy, like France and the UK, is facing voters who a frustrated with the lack of improvement in the household finances and the populist movements sweeping across them are looking for governments to spend their way into national prosperity. Neither Italy, France, Germany nor the UK have strong or stable political leadership and GDP growth is faltering. This is not good.

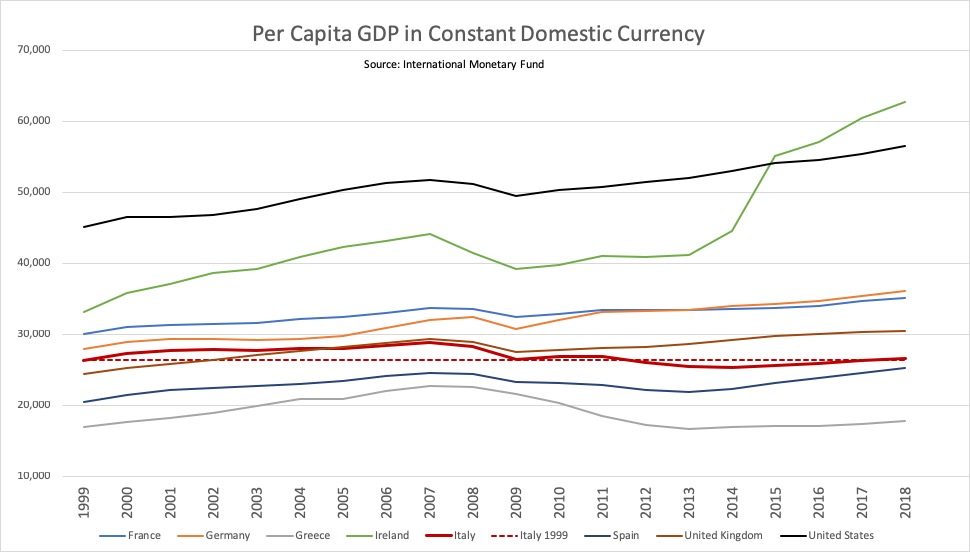

According to data from the International Monetary Fund’s October 2018 Edition of the World Economic and Financial Survey, since the inception of the unified currency, Italy has seen all of a 1% increase in its per capita GDP (as measured by chained domestic currency) while even beleaguered Greece has enjoyed a 5% increase. On the other end of the spectrum Ireland has seen its per capita GDP nearly double with an increase of 89%, Germany is in second place with a 29% improvement while the US and the UK both have seen a 25% improvement. Is it any wonder that voters in Italy are becomingly increasingly skeptical of the euro?

Putting it all together

In our last Context & Perspective piece I discussed how we are seeing a profound decline in the level of liquidity at a time when debt levels are back to record highs. In this week’s piece, I discuss the trends across major parts of the world that are likely to lead to even more debt. We look to be in the final innings of what the master investor Ray Dalio of Bridgewater Associates refers to as the debt super-cycle. These cycles tend to run 50-75 years and we are today at the far end of that range with excessive leverage across much of the world, highly concentrated lending portfolios and a mismatch between assets and liabilities and/or liabilities and asset cash generation potential.

We’ll be talking about this more in the coming months but before then, I highly recommend Mr. Dalio’s free book on how to navigate a debt crisis, which you can get a copy of here. The impact of all this debt on the economies of the world will have a profound impact on tomorrow’s investable markets.

Disclosure: None.