Bank Lending Flatlines As Investment Prospects Dim

As we discussed in Slowing Growth is Natural Product of Debt Hangover, a weakening credit impulse globally continues to bode poorly for economic momentum for the foreseeable future.

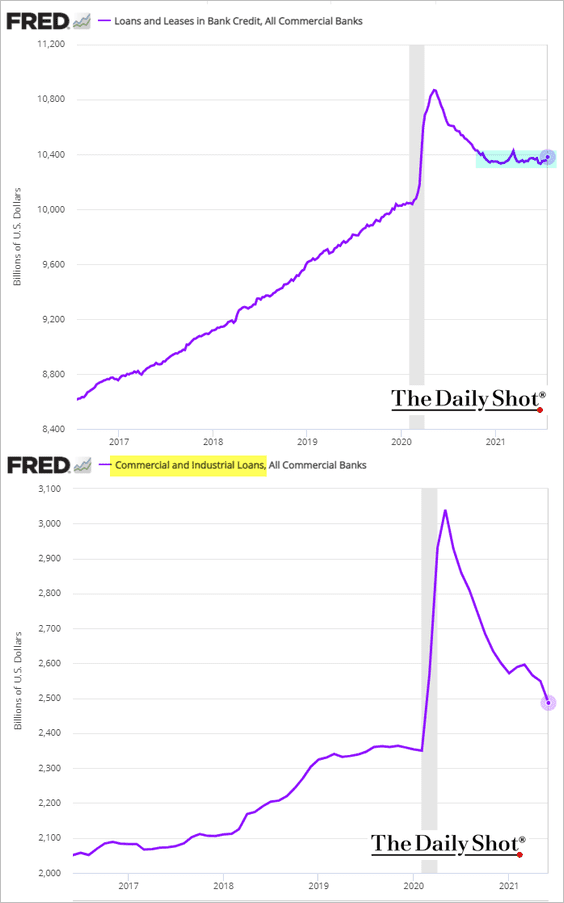

As shown below since 2016, the change in the flow of credit (commercial loans taken) has stalled over the last year notwithstanding trillions in cash injected into the lending system through central bank bond-buying. Quantitative easing can flood banks with liquid reserves but it cannot make the private sector use it.

When corporations are debt-heavy and lacking in compelling domestic investment opportunities they have little incentive to seek new bank loans.

For their part, banks are in the business of only making loans that have a high probability of being repaid in full with interest.

As Richard C. Koo, explains in The Other Half of Macroeconomics (2018):

“Once the bubble bursts and households and businesses are left facing debt overhangs, no amount of monetary easing by the central bank will persuade them to resume borrowing until their balance sheets are fully repaired. Some are badly traumatized by the years of painful deleveraging experience and may never borrow again—even after they restore their balance sheets…The fact that a number of central bank governors continue to insist that further monetary easing will enable them to meet their inflation targets suggests that they still do not understand why their models and forecasts have failed.”

Disclosure: None.