US Dollar Treading Water As Central Banks Follow Fed In Race To Bottom - Central Bank Weekly

Volatility is back in FX markets, and that’s largely due to the machinations and meddling of central banks. As the US-China trade war of attrition drags on, global growth has started to cool in all parts of the world, not just among developed economies or the world’s largest nations. That three central banks not considered part of the ‘top tier’ of central banks moved forth with aggressive, surprising interest rate cuts is a veritable ‘canary in the coal mine’: the negative impact of the US-China trade war is spreading beyond the borders of the world’s two largest economies.

For some central banks, the mere act of lowering interest rates will also increase the appeal of their local currency; in doing so, the country’s exports become more attractive to foreigners who now have more purchasing power.

But what has begun, in a sense, is a “race to the bottom,” akin to what was seen during and after the Global Financial Crisis: to stimulate their economies, central banks loosen up credit availability by reducing interest rates in tandem. Because all central banks are cutting rates at the same time, interest rate differentials do not change; no competitive trade advantage is gained via exchange rates.

The Fed Rate Cut Cycle Will Be Aggressive

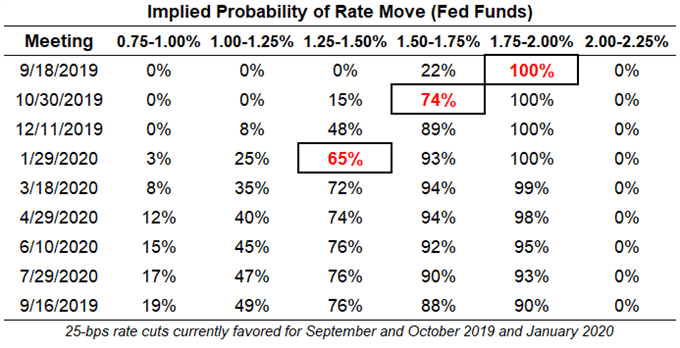

Rate cut odds remain frontloaded, even after the Fed cut rates. Prior to the July Fed meeting, Fed funds futures were discounting a 76% chance of another 25-bps rate cut in September and a 56% chance of a third and final 25-bps rate cut in December 2019.

Federal Reserve Interest Rate Expectations (August 8, 2019) (Table 1)

(Click on image to enlarge)

Now, according to Fed funds futures, after the Trump tariff announcement on August 1 and the ensuing USDCNH devaluation, there is now a 100% chance of a 25-bps rate cut in September, a 74% chance of another 25-bps rate cut in October, and a 48% chance of a fourth 25-bps rate cut in the cycle coming in December. There is a 65% chance of the fourth 25-bps rate cut at the January 2020 meeting; or, 100-bps in total in just six months.

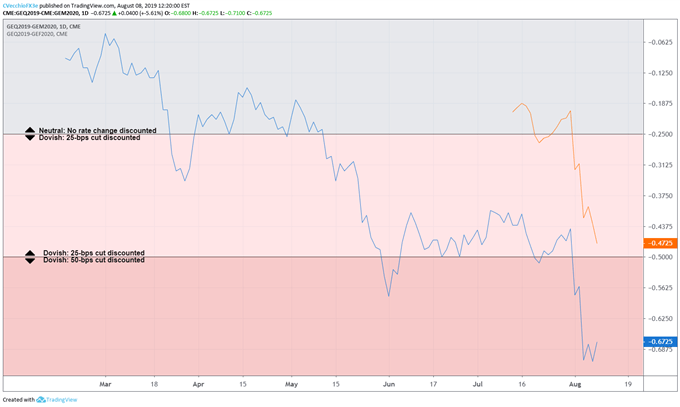

Eurodollar contracts are now as aggressive in their dovish pricing as the Fed rate cut cycle has begun. We can measure whether a rate cut is being priced-in by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. The chart below showcases the difference in borrowing costs – the spreads – for August 19/January20 (orange) and the August 19/June20 (blue), in order to gauge where interest rates are headed in the December 2019 Fed meeting and the June 2020 Fed meeting.

Eurodollar Contract Spreads –August 19/January 20 (Orange), August 19/June 20 (Blue) (FEBRUARY 2019 to AUGUST 2019) (Chart 1)

(Click on image to enlarge)

Based on the Eurodollar contract spreads, a 25-bps rate cut is fully discounted at the September Fed meeting. There is an 89% chance of seeing two 25-bps rate through the end of 2019 and a 71% chance of three more 25-bps rate cuts coming by June 2020.

Fed Rate Cut Odds are Frontloaded Due to US-China Trade War

This point bears repeating time and again. Traders must appreciate the way interest rate markets are currently discounting Fed rate cuts. Markets feel that if Fed rate cuts are coming, they’re going to come over the next several months, a direct response to the growing threat of the US-China trade war. It thus stands to reason that if a US-China trade deal materializes at any point in time – low odds at present time, given the rhetoric from both China and the US – there will be a violent repricing of Fed rate cut odds.

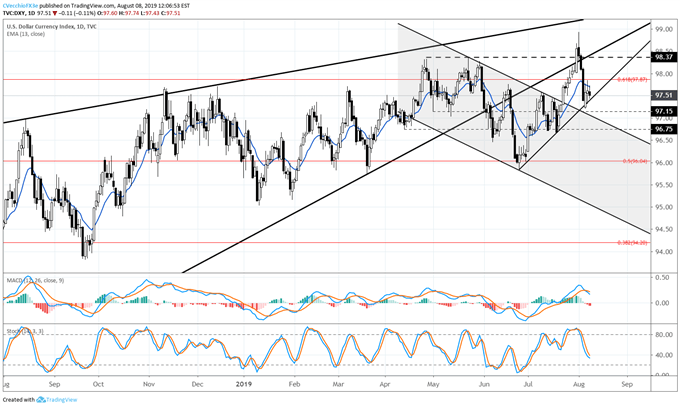

DXY INDEX TECHNICAL ANALYSIS: DAILY PRICE CHART (AUGUST 2018 TO AUGUST 2019) (CHART 2)

(Click on image to enlarge)

It’s very possible that the jump in Fed rate cut odds have spurred the conditions for a false breakout in the US Dollar (via the DXY Index). A false breakout here would occur at critical resistance in the form of (1) former trendline support from the February 2018 and March 2019 lows and (2) the bearish daily key reversal bar set at the former yearly high at 98.37.

However, the uptrend from the June and July swing lows has been maintained on the selloff this week, effectively neutralizing immediate bearish momentum. As a result of the DXY Index being intermeshed with its daily 8-, 13-, and 21-EMA envelope, daily MACD trending lower albeit in bullish territory, and Slow Stochastics now dipping below its median line, the US Dollar’s near-term outlook is decidedly neutral.

Accordingly, the outlook would only intensify in its bearishness if the DXY Index were to break the August low at 97.21.